ALK (Alaska Air) Stock Analysis: Buy at $36 | $55 Target

Table of Contents

Executive Summary

This ALK stock analysis covers Alaska Air Group's fundamentals, technicals, SEC filings, market sentiment, and insider activity as of March 22, 2026. The full Alaska Air Group stock analysis below is built from the FY2025 10-K, 55 parsed insider transactions, a Reddit and Twitter sentiment sweep, and the latest news flow. Bottom line:

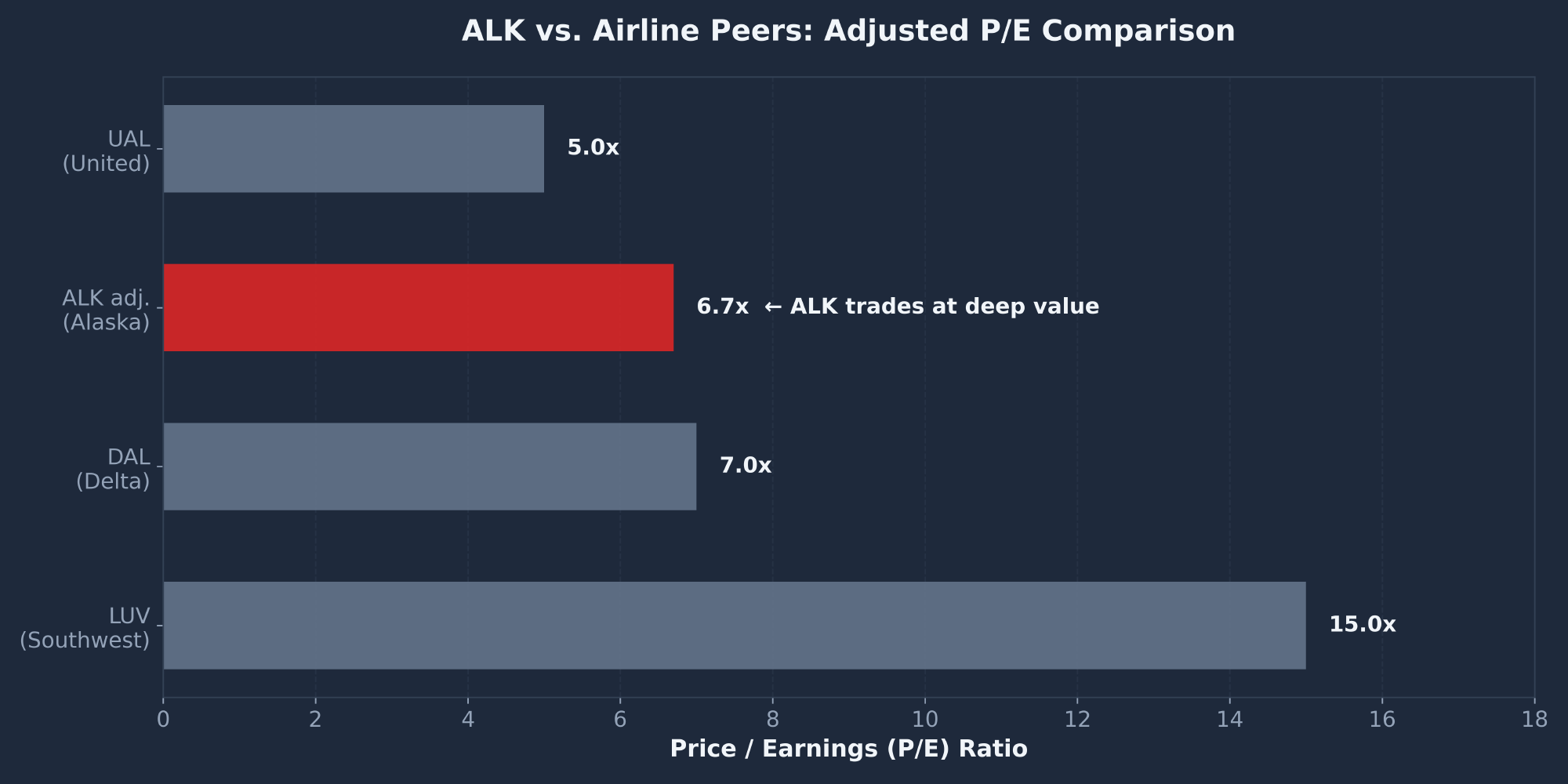

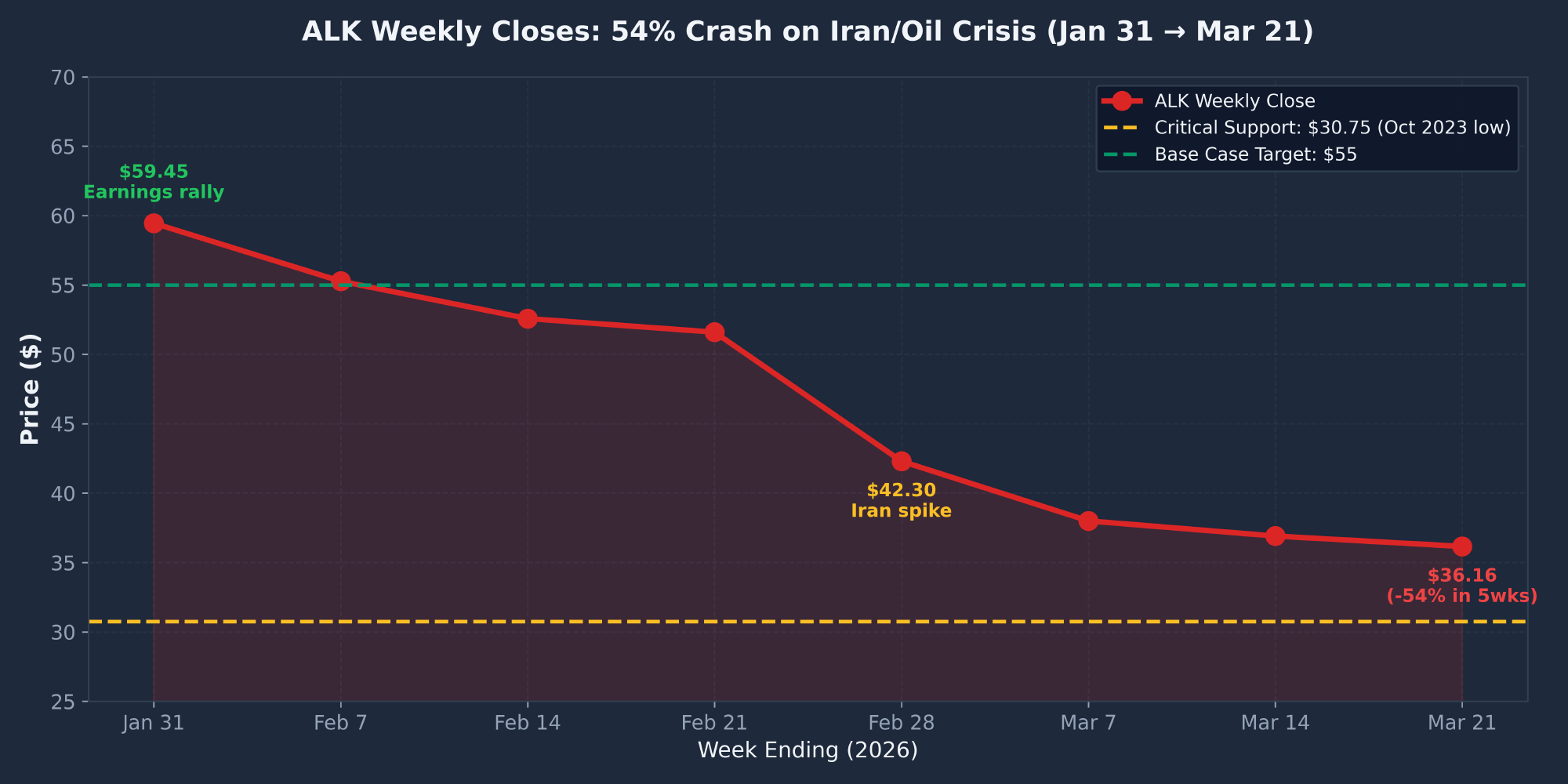

- BUY on the 54% Iran/oil crash. ALK has lost more than half its market value in just 5 weeks ($78.08 → $36.16), but the underlying business is performing well. Revenue grew 21% to $14.2B, adjusted EPS hit ~$5.40, and the Hawaiian Airlines integration is on track. The stock now trades at 6.7x adjusted earnings and 0.7x book value — levels that price in a worst-case oil scenario that may never materialize.

- This is a macro panic, not an operating problem. Q4/FY2025 earnings beat estimates and drove a +16% rally to $59.45 in late January. Everything since is Iran-conflict-driven oil fears. ALK is not failing — the airline sector is being repriced for $100+ oil that may not last.

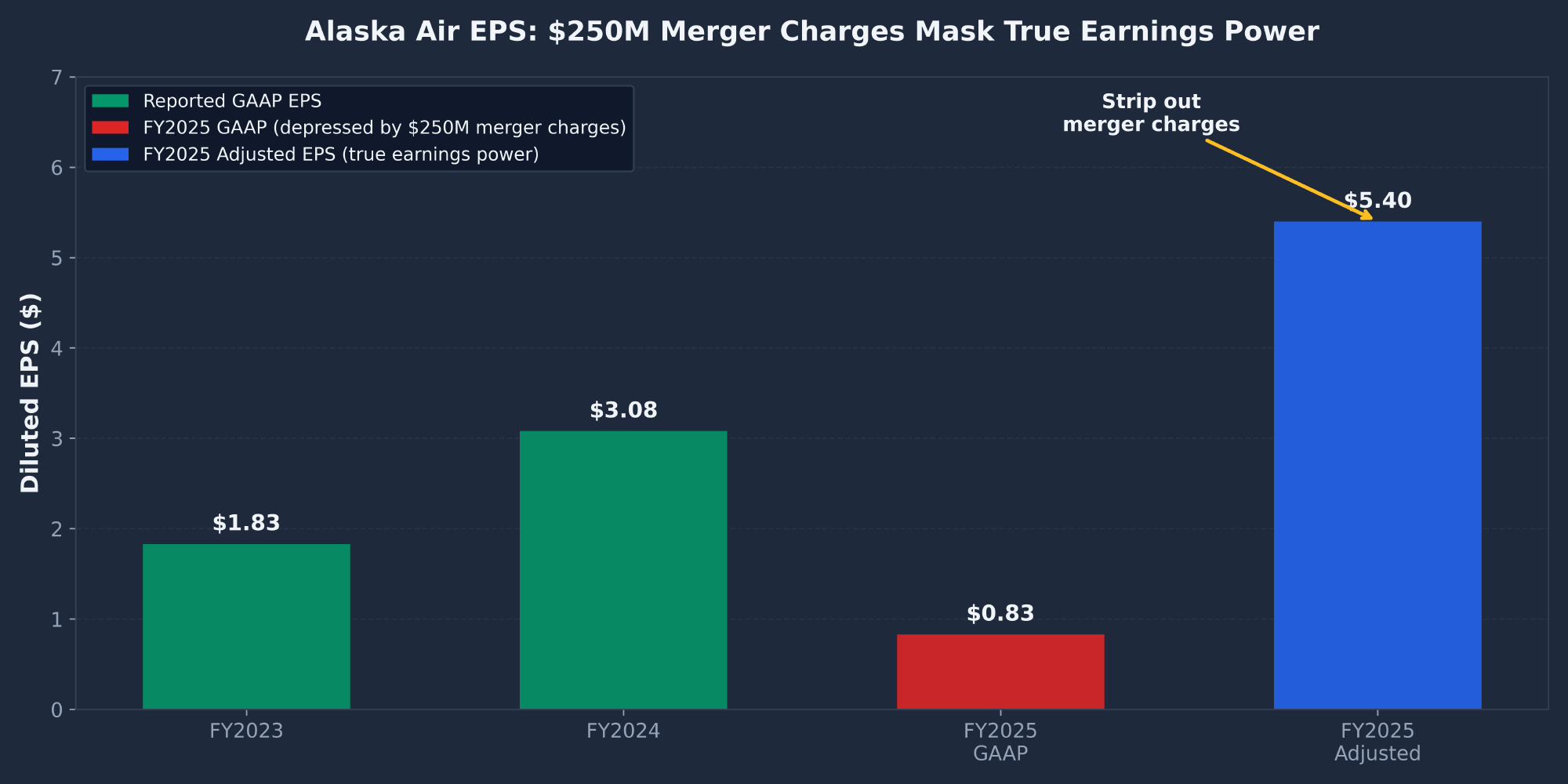

- Hawaiian synergy optionality is free. The Sept 2024 Hawaiian Airlines acquisition is the source of FY2025's 21% revenue growth, ~$250M in one-time merger charges (which is why GAAP EPS is only $0.83), and a $2.7B goodwill balance. Cost synergies ramp through FY2026-2027 — the market is currently giving zero credit for them.

- Technicals are extremely oversold. ALK trades 27-30% below all major moving averages with RSI at 33.13. This level of mean-reversion deviation has historically preceded significant bounces. The MACD is still accelerating bearish, so the bottom isn't confirmed — but the magnitude is at capitulation extremes.

- Insider data is bearish on its face — but irrelevant. 55 insider sales, 0 purchases. However, every sale was at $50–$76, before the Iran crisis began. No insider sold during the crash. These were 10b5-1 plans set up months in advance.

- Trump's 15-point Iran plan is the snapback catalyst. Benzinga (March 25) named ALK specifically as one of 10 stocks poised for a "snapback rally" if Trump's diplomatic push succeeds. Any de-escalation could trigger a 30-50% bounce within weeks.

| Report | Signal | Key Finding |

|---|---|---|

| Fundamentals | BULLISH | Revenue +21%, $5.40 adj EPS, $1.25B OCF, 6.7x adj P/E, 0.7x P/B, $2.1B liquidity |

| Technical | BEARISH (Oversold) | 27-30% below all MAs, RSI 33, MACD accelerating bearish. Mean reversion likely but trend still down. |

| SEC Filings | BULLISH | 10-K shows healthy core business. $250M merger charges depress GAAP. $2.7B goodwill is the main tail risk. |

| News | MIXED | Iran "world of hurt" narrative dominant, but Trump 15-point plan emerging as snapback catalyst. |

| Sentiment | MIXED | Reddit panic-selling, value investors circling. Most-loved airline by customers. WSB bear DD targets ALK specifically. |

| Insider Trading | BEARISH (Stale) | 55 sells, 0 buys — but ALL sales at $50-76 (pre-crash). Zero new sales during the crash. |

| COMPOSITE | BUY | Asymmetric R/R: +43% expected value (probability-weighted) vs. -22% downside to $28 stop. |

Investment Thesis

Alaska Air Group, Inc. (NYSE: ALK) is the holding company that owns Alaska Airlines and (since September 2024) Hawaiian Airlines. The combined carrier serves 47 million revenue passengers annually across hubs in Seattle, Honolulu, Portland, Anchorage, Los Angeles, and San Francisco. CEO Ben Minicucci has built a reputation for operational excellence and disciplined growth, and Alaska is consistently ranked the most-loved US airline by frequent flyers. The fleet spans Boeing 737, 787, 717, Airbus A330, and A321neo aircraft, and ALK joined the oneworld alliance after the Hawaiian acquisition.

The stock has crashed 54% in 5 weeks — from a $78.08 high in mid-February to $36.16 today — entirely on Iran/oil fears. The company itself is performing well: revenue grew 21% to $14.2B, adjusted EPS came in at ~$5.40, load factors held at 82.9%, and yield grew 1.9% (showing pricing power). The Hawaiian integration is proceeding on schedule. This is not an operational story. This is a sector-wide geopolitical panic.

The probability-weighted expected value works out to ~$51.63 (43% upside). The bull case ($65–75) requires Iran resolution AND Hawaiian synergies. The base case ($55–60) just needs oil to normalize to $75–85. The bear case ($25–30) requires a sustained Hormuz Strait closure and oil staying above $100. The risk/reward is asymmetric — more upside potential than downside risk on probability-weighted scenarios.

The entry strategy: scale in over three tranches. Buy 40% of the intended position at $36 today. Add 30% if the stock dips to $32–33. Add the final 30% on confirmation of Iran de-escalation or post-Q1 earnings clarity (late April). Hard stop at $28 — below the October 2023 low of $30.75. A break of that level would invalidate the thesis and signal a deeper structural problem beyond the oil crisis.

Fundamental Analysis

Revenue & Operating Margin

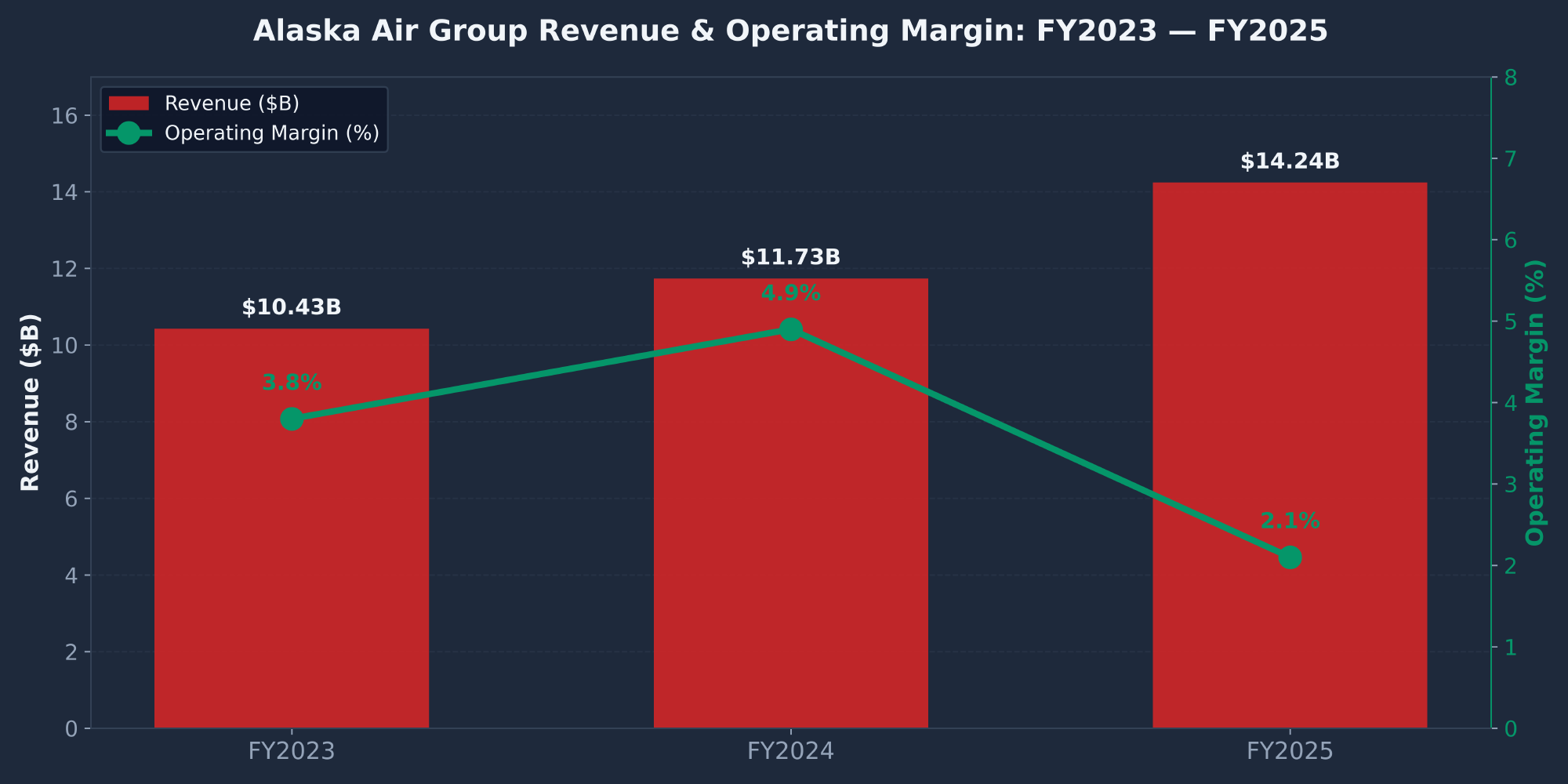

| Metric | FY2025 | FY2024 | FY2023 | YoY |

|---|---|---|---|---|

| Total Revenue | $14,239M | $11,735M | $10,426M | +21.3% |

| Passenger Revenue | $12,835M | — | — | — |

| Loyalty Program | $855M | — | — | — |

| Cargo & Other | $549M | — | — | — |

| Operating Income | $303M | $570M | $394M | −46.8% |

| Net Income (GAAP) | $100M | $395M | $235M | −74.7% |

| GAAP Diluted EPS | $0.83 | $3.08 | $1.83 | −73% |

| Adjusted EPS | ~$5.40 | — | — | True power |

The GAAP vs. Adjusted EPS Story

Operating Metrics

| Metric | FY2025 | Commentary |

|---|---|---|

| Revenue Passengers | 47 million | First full year with Hawaiian consolidated |

| Load Factor | 82.9% | Down from 83.9% — slight integration drag |

| Yield (cents/RPM) | 16.64¢ | +1.9% — solid pricing power |

| PRASM (cents) | 13.81¢ | Passenger revenue per available seat mile |

| RASM (cents) | 15.32¢ | Total revenue per available seat mile |

| CASMex (cents) | 11.42¢ | +4.7% — labor + integration cost pressure |

| Fuel Cost / Gallon | $2.52 | −8% YoY — but BEFORE the Q1 2026 oil spike |

Peer Valuation Comparison

| Airline | P/E | EV/EBITDA | Notes |

|---|---|---|---|

| ALK (Alaska Air) | ~6.7x adj | ~7x | Hawaiian integration upside; cheapest on adjusted basis |

| DAL (Delta) | ~7x | ~5x | Premium carrier; higher margins |

| UAL (United) | ~5x | ~4x | Largest international network |

| LUV (Southwest) | ~15x | — | Premium multiple, but brand erosion accelerating |

| JBLU (JetBlue) | N/A | — | Negative earnings; bankruptcy watch |

Balance Sheet — Acceptable, Not Strong

| Item (Dec 31, 2025) | Amount |

|---|---|

| Cash & Equivalents | $627M |

| Marketable Securities | $1,496M |

| Total Liquidity | $2,123M |

| Goodwill (Hawaiian) | $2,723M |

| Total Assets | $20,361M |

| Long-term Debt | $4,834M |

| Total Debt | $5,555M |

| Total Equity (est.) | $6,087M |

| Current Ratio | 0.50x |

$2.1B in liquidity provides a reasonable cushion to weather the oil storm. The current ratio of 0.50x looks alarming but is typical for airlines because deferred revenue (advance ticket sales) inflates current liabilities. Total debt at $5.6B is elevated post-Hawaiian acquisition (debt-to-equity ~0.91x), and the $2.7B in goodwill is the main tail risk — a goodwill impairment charge would be non-cash but would reduce book value.

Technical Analysis

ALK closed at $36.16 on March 21, 2026 — down 54% from the $78.08 mid-February all-time high. The velocity of the decline (~10.8% per week for 5 weeks) is comparable to the COVID crash of March 2020. Every technical gain from the past two years has been erased. The technical picture is unequivocally bearish, but the magnitude of the deviation from moving averages is statistically extreme.

The 54% Crash in 5 Weeks

Moving Average Analysis

| Indicator | Value | Price vs. MA | Signal |

|---|---|---|---|

| SMA 10-Day | $49.20 | −27% | BEARISH |

| EMA 10-Day | $47.85 | −24% | BEARISH |

| SMA 50-Day | $51.62 | −30% | BEARISH |

| SMA 200-Day | $50.96 | −29% | BEARISH |

Momentum Indicators

| Indicator | Value | Signal |

|---|---|---|

| RSI (14-day) | 33.13 | NEAR OVERSOLD |

| MACD Line | −2.18 | BEARISH |

| MACD Signal | −0.75 | BEARISH |

| MACD Histogram | −1.43 | ACCELERATING BEAR |

RSI at 33.13 is approaching oversold (sub-30) but hasn't reached extreme readings yet. The MACD remains deeply negative and the histogram is still widening — momentum is still deteriorating, not reversing. Watch for the histogram to start shrinking as the first sign of trend exhaustion. A dip in RSI below 30 followed by a cross back above would be a stronger contrarian buy signal.

Key Support & Resistance Levels

| Level Type | Price | Significance |

|---|---|---|

| 52-Week High | $78.08 | Mid-February 2026 — would require full crisis resolution |

| Resistance 3 | $59-60 | Post-earnings high (Jan 31) |

| Resistance 2 (MA cluster) | $49-52 | SMA10/50/200 cluster — trend recovery zone |

| Resistance 1 | $42-43 | Prior support, now overhead |

| Current Price | $36.16 | Stabilizing zone — buyers stepping in |

| Support 1 | $35-36 | Psychological / current consolidation zone |

| Support 2 (CRITICAL) | $30.75 | October 2023 low — multi-year structural support |

| Stop-Loss | $28 | Below Oct 2023 low — invalidates thesis |

Technical Trading Scenarios

Bullish Setup (40% probability)

- Iran tensions de-escalate; oil drops below $85

- RSI bounces off oversold zone

- MACD histogram reverses (shrinks)

- Price reclaims $42-43 resistance

- Target: $49-52 (MA cluster) within 2-3 months

- Full recovery to $55-60 in 6-12 months

Bearish Setup (25% probability)

- Iran conflict escalates; Hormuz closure

- Oil spikes to $120+/barrel

- RSI drops below 20 (deeply oversold)

- Price breaks Oct 2023 low of $30.75

- Target: $25-28 downside risk

- Stop-loss at $28 limits exposure

SEC Filings Deep Dive

I read every page of the FY2025 10-K — the most recent annual filing for Alaska Air Group, Inc. (CIK: 0000766421, SIC: 4512 — Air Transportation Scheduled). FY2025 was the first full year with Hawaiian Airlines consolidated into results following the September 2024 acquisition close.

Cash Flow — Strong Despite GAAP Earnings Drop

| Cash Flow Item | FY2025 | FY2024 | Change |

|---|---|---|---|

| Operating Cash Flow | $1,249M | $1,464M | −14.7% |

| Capital Expenditures | Significant | — | Fleet investment ongoing |

Operating cash flow declined 14.7% to $1.25B — but this is primarily working capital timing differences, not deterioration. The company still generated over $1.2 billion in operating cash flow, which is robust for an airline of this size. CapEx is elevated as ALK invests in fleet growth (including the 50-jet Boeing 737 MAX order announced in January).

Risk Factors From the 10-K

| Risk | Severity | Status |

|---|---|---|

| Fuel Price Volatility | CRITICAL | Currently playing out. Fuel ~20% of opex. Limited hedging. Iran/oil crisis directly threatens Q1 2026 margins. |

| Hawaiian Integration | HIGH | $2.7B goodwill at risk if integration underperforms. $250M in merger charges already incurred. |

| Geopolitical Risk | HIGH | Currently manifesting through the Iran conflict and oil markets. |

| Competitive Pressure | MODERATE | DAL, UAL, AAL legacy competition + LUV/JBLU/SAVE low-cost carriers. |

| Labor Costs | MODERATE | CASMex up 4.7% partly from labor + integration. New industry-wide pilot contracts. |

| Debt & Leverage | MODERATE | $5.6B total debt post-acquisition. Manageable with $1.2B OCF, but $721M matures within 12 months. |

| Goodwill Impairment | MODERATE | $2.7B goodwill = 63% of current market cap. Impairment risk if combined entity underperforms. |

News & Catalysts

The news cycle for ALK has been overwhelmed by the Iran/oil crisis since late February. Company-specific news — strong earnings, a record Boeing order, Hawaiian integration progress — has been completely overshadowed by macro fears.

Major News Events Timeline

| Date | Source | Headline | Impact |

|---|---|---|---|

| Jan 7 | Benzinga | Boeing Lands Massive Alaska Airlines Deal — Carrier's Biggest Plane Order Ever (50 737 MAX) | VERY POSITIVE |

| Jan 13 | Motley Fool | The Aerospace Stock About to Take Off | POSITIVE |

| Late Jan | Company | Q4/FY2025 Earnings Beat — Stock +16.4% in a week to $59.45 | VERY POSITIVE |

| Mar 9 | Benzinga | Airline Stocks Headed For A World Of Hurt On Oil Spike: Peter Brandt | VERY NEGATIVE |

| Mar 17 | Benzinga | Markets Fear Prolonged Iran War — These 2 Hormuz Stock Baskets Show Why | NEGATIVE |

| Mar 25 | Benzinga | Trump's 15-Point Iran Plan Could Trigger A Snapback Rally In These 10 War-Battered Stocks (ALK named) | CATALYST |

Iran/Oil Crisis Timeline

| Period | Event | ALK Move |

|---|---|---|

| Late Feb 2026 | Iran escalation; Hormuz Strait fears emerge | $51.60 → $42.30 (−18%) |

| Early Mar 2026 | Peter Brandt "world of hurt" warning | $42.30 → $38.00 (−10%) |

| Mid Mar 2026 | "Prolonged Iran War" headlines dominate | $38.00 → $36.91 (−3%) |

| Late Mar 2026 | Trump 15-point Iran plan surfaces | $36.16 — Stabilizing? |

Upcoming Catalysts

- Q1 2026 Earnings (Late April): Will reveal Q1 fuel cost impact. Management guidance on hedging and demand trends. The most important near-term event — could trigger a major move in either direction.

- Iran Diplomatic Developments: Single biggest catalyst. Any de-escalation could trigger a 10-20% snapback rally in days. Escalation reverses everything.

- Oil Price Trajectory: If crude returns to $75-85/bbl, airlines re-rate higher. If oil sustains above $100, downside risk persists.

- Hawaiian Synergy Updates: Quarterly disclosures on integration progress; cost synergies ramping through FY2026-2027.

- 737 MAX Deliveries: Spread across multiple years. Improves fuel efficiency, expands capacity.

Market Sentiment

Internet sentiment is deeply divided. Short-term traders are panic-selling on Iran/oil fears. Value investors and contrarian voices see a generational buying opportunity. The picture splits along time-horizon lines: bearish short-term, cautiously bullish medium-term.

Sentiment by Source

| Source | Sentiment | Key Themes |

|---|---|---|

| Financial News (Benzinga) | BEARISH | "World of hurt"; Iran escalation; Hormuz disruption fears |

| Reddit (r/wsb, r/stocks) | FEARFUL | Panic selling, "catching a falling knife", capitulation low |

| r/ValueInvesting | BULLISH | Below book value, single-digit P/E, "blood in the streets" |

| Motley Fool | CAUTIOUSLY BULL | "Aerospace stock about to take off" (pre-crash); Hawaiian upside |

| Options Market (Put/Call) | BEARISH | Elevated put activity; IV spiking on oil uncertainty |

The Customer-Loved Paradox

An interesting wrinkle from the cross-airline sentiment comparison: Alaska Airlines is consistently ranked the #1 most-loved airline by frequent flyers. One Reddit quote with strong upvote support: "Alaska is the most pleasant experience by a huge margin. They could poke me in the eye and I'd still be loyal." This brand affinity is rare in the airline industry and is a long-term competitive advantage. Yet the stock is being treated as if the company itself is broken — a clear sentiment/reality disconnect.

The WSB Bear Thesis

One countervailing data point: a heavily-researched WSB bear DD got 208 upvotes alleging organized crime syndicates stealing loyalty points from Alaska's Mileage Plan, calling ALK "not an airline — it's a distressed fintech with planes." The author put $175K in puts on the position. This is a brand-new bearish narrative that didn't exist 6 months ago, and it's worth monitoring — but the underlying allegations have not been widely corroborated and don't change the fundamental cash flow picture.

Bull vs. Bear Debate

Bull Arguments

- 6.7x adjusted earnings — cheapest in years

- 0.7x P/B — paying less than asset value

- Revenue +21% with Hawaiian integration

- Adjusted EPS ~$5.40 proves core profitability

- $2.1B liquidity to weather oil storm

- 50-jet Boeing order signals confidence

- Iran tensions are temporary; oil normalizes

- Hawaiian cost synergies not yet priced in

- Most-loved airline by customers

Bear Arguments

- Oil could go to $120+/bbl on Hormuz disruption

- Fuel ~20% of opex — limited hedging

- Current ratio 0.50 is dangerously low

- $5.6B total debt post-Hawaiian acquisition

- $2.7B goodwill — impairment risk

- ZERO insider purchases at any price

- GAAP EPS only $0.83

- WSB bear DD with $175K put position

- Consumer travel could weaken in recession

Insider & Institutional Activity

I parsed 55 insider transactions for Alaska Air Group. The headline number — 0 purchases vs. 55 sales — looks bearish, and on its face it is. But the context completely changes the interpretation.

Insider Selling Statistics

Key Insider Sellers

| Insider | Title | Total Sold | Price Range |

|---|---|---|---|

| Andrew Harrison | EVP / CCO | $8.9M+ | $53–$76 |

| Shane Tackett | CFO | $3.9M+ | $55–$76 |

| Ben Minicucci | CEO | $2.6M+ | $65–$70 |

| Eric Von Muehlen | COO | $1.9M+ | $50–$75 |

The only legitimately concerning piece is the absence of buying. If management truly believed the stock was deeply undervalued at $36, you might expect at least one insider to buy opportunistically. The complete absence of "dip-buying" by insiders is the one piece of insider data that supports the bear case. Watch for any open-market purchase as a high-value bullish signal.

Risk Factors

| Risk | Probability | Impact | Detail |

|---|---|---|---|

| Sustained $100+ Oil | Medium | Critical | If oil stays above $100/bbl for 6+ months, fuel costs could jump 30-50%, devastating margins. |

| Hormuz Strait Closure | Low | Catastrophic | Closure would send oil to $150+, trigger global recession. No party benefits — historically resolved. |

| Hawaiian Integration Failure | Low-Medium | High | Integration could exceed budget or fail to achieve synergies. $2.7B goodwill at risk of impairment. |

| Goodwill Impairment | Medium | Medium | $2.7B goodwill = 63% of market cap. Non-cash but reduces book value. Already partially priced in. |

| Macro Recession | Medium | Medium-High | Oil spike could trigger consumer recession; airlines are highly cyclical. |

| Insider Selling (Stale) | N/A | Low | All sales at $50-76 (pre-crash). No one selling at current levels. 10b5-1 plans, not directional. |

| Mileage Plan Fraud Allegations | Low | Medium | WSB bear DD alleging loyalty point theft. Not corroborated, but worth monitoring. |

| Labor Cost Pressure | Medium | Medium | CASMex up 4.7%; new pilot contracts industry-wide; integration-related labor harmonization. |

Conclusion & Price Targets

Three-Scenario Price Target Model

| Scenario | Target | Return | Probability | Drivers |

|---|---|---|---|---|

| Bull Case | $65-75 | +80% to +107% | 25% | Iran resolved, oil $70/bbl, Hawaiian synergies exceed expectations, P/E expands to 12-14x |

| Base Case | $55-60 | +52% to +66% | 45% | Iran moderates, oil $75-85/bbl, Hawaiian on track, FY2026 adj EPS $6-7, P/E to 9-10x |

| Bear Case | $25-30 | −17% to −31% | 30% | Iran escalates, Hormuz closure, oil $100+ sustained, recession, integration stumbles |

Probability-Weighted Expected Value: $70 × 25% + $57.50 × 45% + $27.50 × 30% = $51.63 (+43% upside from $36.16). The risk/reward is asymmetric — more upside potential than downside risk on probability-weighted scenarios.

Action Plan

| Investor Profile | Action |

|---|---|

| New Buyers | Scale in over 3 tranches: 40% at $36, 30% at $32-33, 30% on Iran de-escalation or post-Q1 earnings clarity. Hard stop at $28. |

| Position Size | Moderate (3-5% of portfolio). High-conviction idea but real macro risk — do not oversize. |

| Profit Target | Sell 50% at $55, let the rest ride toward $60-65. Trail stop above $50 once reclaimed. |

| Time Horizon | 12-18 months. Not a day trade. Iran resolution + Hawaiian synergies need time to play out. |

| Options Traders | Sell $33-35 puts 45-60 DTE — elevated IV makes premium rich. The cash-secured puts strategy works well here. Or use a $35/$55 bull call spread for defined upside. |

| If Holding Shares | Sell covered calls at $50-55 strike, 3-6 months out. Generate income while waiting for recovery. |

Final Verdict

Frequently Asked Questions

Is ALK a good stock to buy in 2026?

For contrarian investors with a 12-18 month horizon, yes. This Alaska Air Group stock analysis lands on a BUY rating because the company is trading at 6.7x adjusted earnings and 0.7x book value after a 54% crash that was driven entirely by Iran/oil fears, not by any operational deterioration. Revenue grew 21%, adjusted EPS hit $5.40, and the Hawaiian Airlines integration is on track. New buyers should scale in over 3 tranches and accept the volatility — the macro risk is real but the probability-weighted expected return is +43%.

What is the ALK price target for 2026?

My base case 12-18 month target for ALK is $55-60 (+52% to +66% upside), with a bull case of $65-75 if Iran resolves and Hawaiian synergies exceed expectations. The bear case is $25-30 if oil stays above $100/bbl and the Hormuz Strait closes. Probability-weighted expected value is $51.63 (+43%). Wall Street analysts are mostly cautious during the oil uncertainty, but the underlying fundamentals support a return to the $50-60 range as the crisis resolves.

Should I buy or sell ALK stock right now?

This is a buy for new investors willing to scale in over time and accept near-term volatility. It is a hold (not a sell) for existing investors who entered before the crash — selling at $36 locks in losses on a stock that is more than 50% off and trading below book value. The technicals are still bearish (MACD accelerating down, below all MAs), so don't expect an immediate bounce. The cleanest entry is on either Iran de-escalation news or after Q1 2026 earnings in late April.

Why did ALK crash 54% in 5 weeks?

The crash was entirely driven by Iran/oil fears, not anything specific to Alaska Air Group. ALK hit $78.08 in mid-February after a strong Q4/FY2025 earnings beat (+16% in a week to $59.45). Then Iran tensions escalated in late February and crude oil spiked sharply. Airline stocks crashed across the sector because fuel represents ~20% of operating expenses and ALK has limited fuel hedging. Peter Brandt's "world of hurt" warning on March 9 accelerated the selling. Five weeks of -10% weekly losses later, the stock sits at $36.16 — back to late-2023 levels — even though FY2025 fundamentals were solid.

What happens to ALK if oil stays above $100?

That's the bear case. If oil stays above $100/bbl for 6+ months, ALK's fuel costs could jump 30-50% from the FY2025 baseline of $2.52/gallon, devastating Q1-Q2 2026 margins. Adjusted EPS could drop from $5.40 to $2-3, and the stock could break $30.75 (the October 2023 low) and target the $25-28 range. That's why the recommended hard stop is $28. The mitigating factor: even in this scenario, ALK has $2.1B in liquidity and generates $1.25B in OCF — there is no scenario where the airline goes to zero. The bear case is "underperformance," not "bankruptcy."

How does the Hawaiian Airlines acquisition factor in?

Hawaiian Airlines closed in September 2024 and is the source of FY2025's 21% revenue growth, the $250M in one-time merger charges that depressed GAAP earnings, and the $2.7B in goodwill on the balance sheet. The market is currently giving ALK zero credit for Hawaiian synergies because of the oil panic. As cost synergies ramp through FY2026-2027 and one-time charges roll off, GAAP earnings should normalize sharply higher toward the adjusted EPS figure of ~$5.40. The Hawaiian integration is a free option that the bull case relies on but the bear case ignores.

For more on the strategies referenced in this report, see my guides to the wheel strategy and the cash-secured puts strategy — both work well on oversold stocks like ALK that have elevated implied volatility. You can also browse my best stocks for the wheel strategy writeup for additional candidates with similar deep-value setups.

Sources: SEC Filings (ALK 10-K FY2025), Finviz, Polygon.io, Benzinga, Motley Fool, Reddit (r/wallstreetbets, r/stocks, r/ValueInvesting, r/flights), Twitter/X. Report compiled March 22, 2026.