BE (Bloom Energy) Stock Analysis: Hold at $155

Table of Contents

Executive Summary

This Bloom Energy stock analysis concludes that BE is a legitimate AI infrastructure play with a real business — but the stock has already priced in 3–5 years of flawless execution. At $154.51, BE trades at 21x FY25 revenue, 272x EV/EBITDA, and 100–165x forward P/E. Every Wall Street analyst target ($68–$162) clusters near or below the current price. The market has run ahead of the fundamentals by a wide margin, and the risk/reward from here is asymmetrically skewed to the downside.

- The business thesis is real. Solid oxide fuel cell (SOFC) servers deploy in ~55 days vs. years for grid interconnection. AI data centers need power now, and Bloom delivers it. FY25 revenue hit $2.02B (+37% YoY), backlog is $20B, and FY26 guidance is $3.1–3.3B (+58%).

- The valuation is extreme. P/S of 21.4x vs. industry average of 2.35x. The company has never been GAAP profitable on an annual basis in 23 years. Net loss widened to -$88M in FY25 despite 37% revenue growth.

- Insider selling is the most lopsided I have ever documented. CEO KR Sridhar sold $34M discretionary (no 10b5-1 plan) at $170 near the all-time high. SK ecoplant dumped $276M. Out of ~120 insider trades over 5 years, there is exactly 1 purchase ($753K by a director in 2021). Everyone else is selling.

- Probability-weighted 12-month target: $155 — essentially flat. Bear case $66 (-57%), base case $135 (-13%), bull case $242 (+57%).

Investment Thesis

After 23 years operating as a niche SOFC company — primarily selling to commercial customers like Walmart, Equinix, and Apple — the AI data center boom has catapulted Bloom Energy into the most compelling demand environment in its history. The core value proposition is simple and powerful: Bloom's fuel cell servers can be deployed in approximately 55 days, providing reliable, behind-the-meter power to data centers that would otherwise wait 3–5 years for grid interconnection.

In a world where hyperscalers are spending $600B on AI infrastructure and power is the binding constraint, Bloom's speed-to-deployment advantage is genuinely differentiated. The numbers reflect this: FY25 revenue of $2.02B (+37% YoY), a $20B total backlog (up 2.5x), a $6B product backlog (up 140%), and FY26 guidance of $3.1–3.3B revenue (+58%). Major deals include a $5B five-year partnership with Brookfield and a $2.65B order from AEP.

Bloom achieved its first-ever GAAP operating profit ($72.8M) in FY25 and generated positive free cash flow ($57M) for the first time. Among fuel cell peers, Bloom is the clear winner — Plug Power (PLUG at $2.15) has lost 98% of its value, while FuelCell Energy (FCEL at $6.63) is also struggling.

The bull case requires belief in a very specific sequence: (1) revenue grows 58% in FY26, (2) margins expand from compressed levels, (3) customer concentration risk doesn't materialize, (4) convertible dilution is offset by earnings growth, and (5) no hyperscaler capex slowdown occurs. Each individually has reasonable odds. All five together? That is pricing in perfection — which is exactly what Bank of America flagged.

Fundamental Analysis

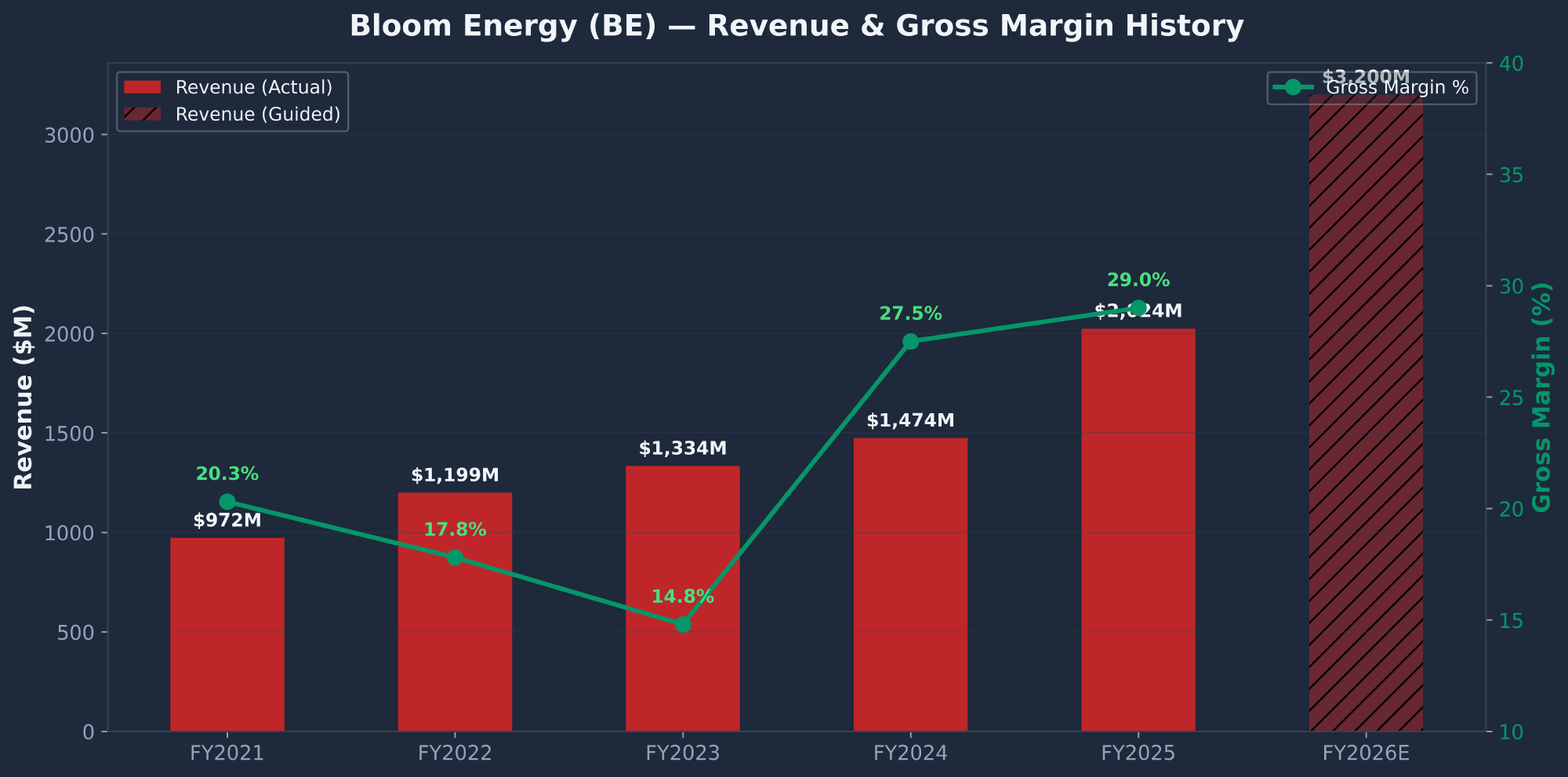

BE Revenue & Profitability

| Metric | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Revenue ($M) | $972 | $1,199 | $1,334 | $1,474 | $2,024 |

| YoY Growth | +22.4% | +23.3% | +11.2% | +10.5% | +37.3% |

| Gross Margin | 20.3% | 17.8% | 14.8% | 27.5% | 29.0% |

| Operating Income ($M) | ($115) | ($80) | ($209) | $23 | $73 |

| GAAP Net Income ($M) | ($193) | ($301) | ($302) | ($29) | ($88) |

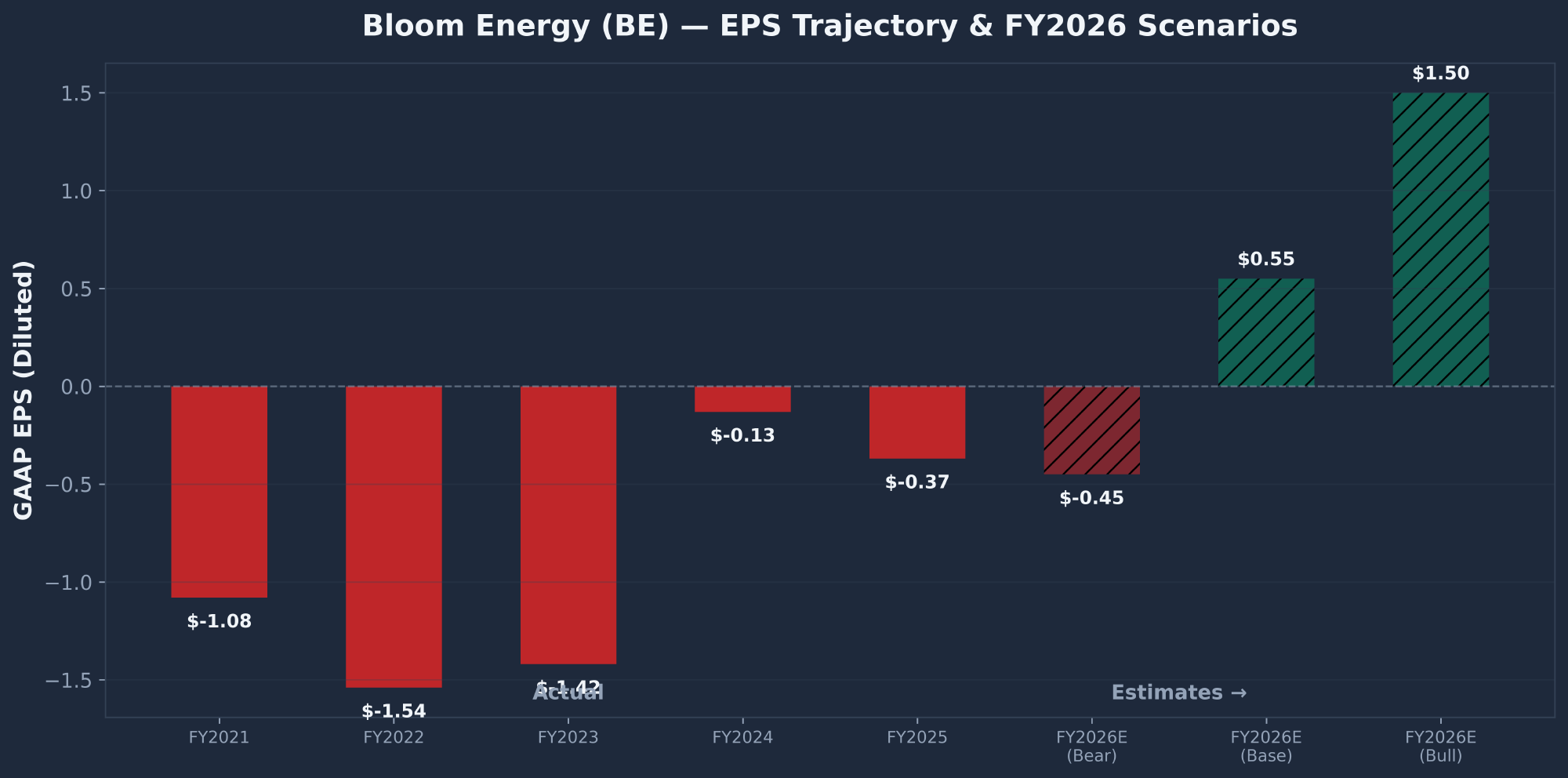

| GAAP EPS (Diluted) | ($1.08) | ($1.54) | ($1.42) | ($0.13) | ($0.37) |

| SBC ($M) | $76 | $114 | $87 | $80 | $140 |

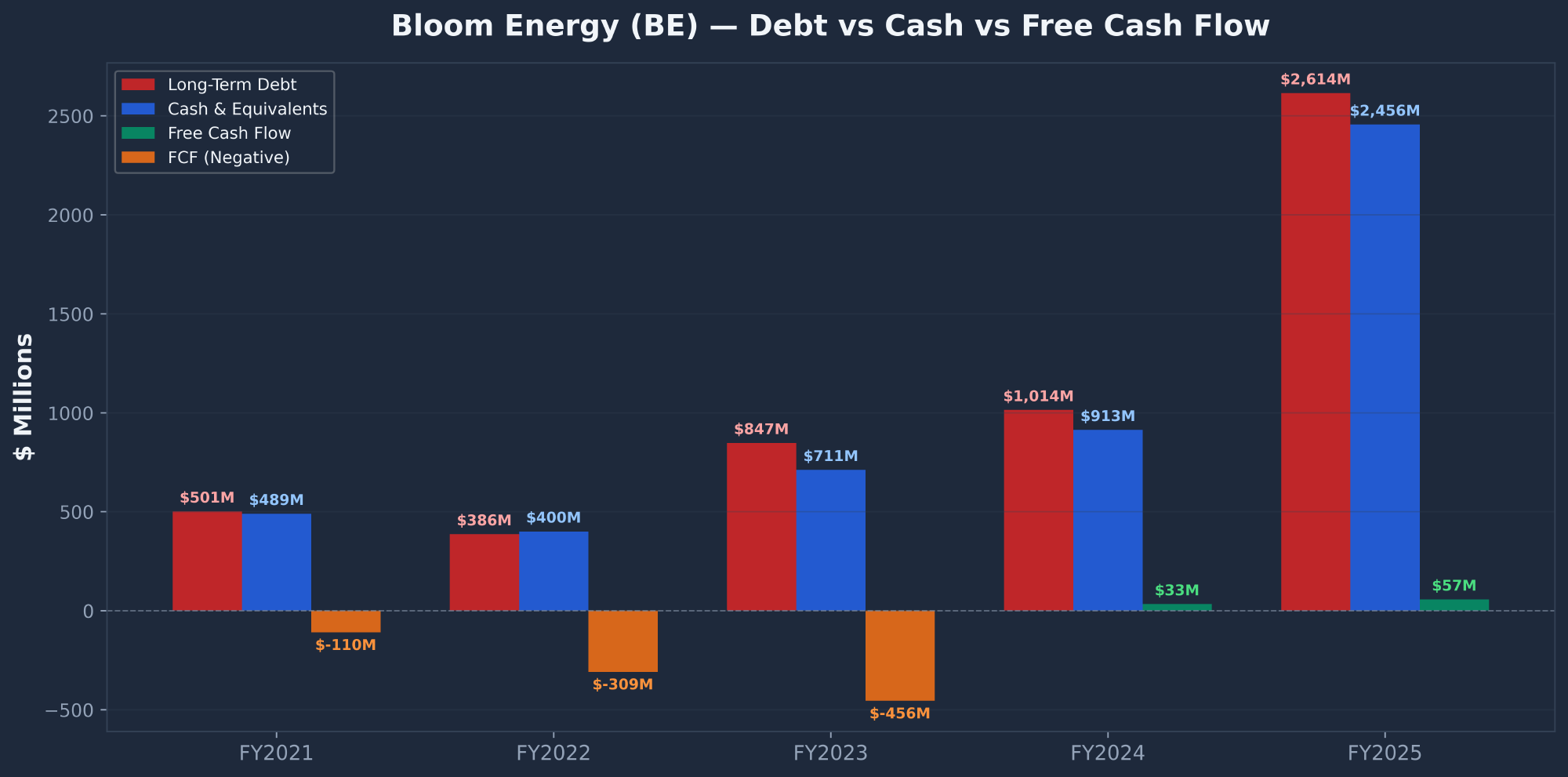

| Free Cash Flow ($M) | ($110) | ($309) | ($456) | $33 | $57 |

The margin trajectory is genuinely improving — gross margin recovered from a trough of 12.4% (FY22) to 29.0% (FY25), a 1,660 bps expansion over three years. Operating margin flipped positive for the first time in FY24. However, net loss widened from ($29M) in FY24 to ($88M) in FY25, even as revenue grew 37%. The culprits: SBC jumped 75% to $140M, and a $98.6M debt conversion/extinguishment charge plus $40.4M in equity losses from Brookfield Fund JVs overwhelmed operating gains.

Balance Sheet & Cash Flow

Bloom executed a massive capital structure transformation in FY25: $2.5B in 0% convertible notes issued in November 2025. Zero percent coupon — meaning the bond market prices the equity conversion option as so valuable that bondholders accept zero yield. Cash jumped 3x to $2.46B, but long-term debt also surged 158% to $2.61B. Debt-to-equity spiked to 3.9x. The dilution risk is real — shares outstanding grew 22% in FY25, and the Oracle warrant adds another potential 5% dilution.

FCF turned positive for the first time ($57M in FY25), but this is tiny relative to the $43.35B market cap — implying a P/FCF of 758x. SBC of $140M dwarfs FCF of $57M, meaning the company pays employees in stock worth 2.4x the cash the business generates.

Valuation Reality Check

| Metric | BE | PLUG | FCEL | ENPH |

|---|---|---|---|---|

| Price | $154.51 | $2.15 | $6.63 | $44.07 |

| Market Cap | $43.4B | $2.1B | $0.3B | $5.8B |

| P/S (TTM) | 21.4x | 3.3x | 4.3x | 4.4x |

| Revenue Growth YoY | +37% | -21% | -44% | -3% |

| GAAP Profitable? | Barely (op profit) | No | No | Yes |

BE commands a 5–6x P/S premium to every fuel cell peer. The premium is justified by 37% revenue growth and first-mover advantage in AI data center power — but Enphase (ENPH), a proven, GAAP-profitable clean energy company, trades at just 4.4x P/S. For more context on how I evaluate options trading opportunities around stocks like these, see my guide to the wheel strategy.

Technical Analysis

BE Stock Price Structure

BE has gone from $15.15 to $180.90 in roughly 12 months — a 10x parabolic move. The stock currently trades at $154.51, down 14.6% from the all-time high. The rally was fueled by three converging forces: AI data center demand narrative, massive short covering (53M shares → 22M), and institutional accumulation.

| Phase | Period | Price Range | Key Events |

|---|---|---|---|

| Base Formation | Aug 2023–Oct 2024 | $8.42–$15.89 | 14-month base. Heavy short interest built (~53M shares). |

| Initial Breakout | Nov–Dec 2024 | $10–$29.81 | Short squeeze ignition. Stock tripled in 12 weeks. |

| Parabolic Rally | Jun–Oct 2025 | $17–$134 | 8x in 5 months. Data center deals + short covering. |

| ATH Push | Jan–Feb 2026 | $134–$180.90 | New ATH. AEP $2.65B deal + earnings beat. |

| Current Pullback | Feb–Mar 2026 | $131–$180.90 | Pulling back from ATH. Oracle/OpenAI cancellation -15.5%. |

Key Technical Indicators

| Indicator | Value | Signal |

|---|---|---|

| SMA 50 | $145.86 | Bullish (+5.9% above) |

| SMA 200 | $86.97 | Extremely Extended (+78% above) |

| RSI (14) | 50.84 | Neutral — reset from overbought |

| MACD | 2.49 (Signal: 3.87) | Bearish crossover — momentum deteriorating |

| Beta | 3.16 | 3x S&P 500 volatility. Expect 30%+ swings. |

| ATR (14) | $15.13 (~10%) | Average $15/day range. Extremely volatile. |

Support & Resistance

Key support levels: $145–147 (SMA 50 confluence, strong), $131–135 (multi-week swing lows, strong), $108–112 (Oct 2025 correction lows), $86–90 (SMA 200, would be a -44% decline). Resistance: $160–167 (sellers have defended repeatedly), $175–180.90 (all-time high zone), $200 (psychological level).

The stock is trading at the 50% Fibonacci retracement ($155.95) of the Jan–Feb rally — right at the line in the sand. RSI at 50.8 is dead-center neutral, having reset from overbought without reaching oversold, which is consistent with a pullback within a bullish trend rather than a reversal. The MACD bearish crossover histogram is improving (-2.53 → -1.39), suggesting the worst of the momentum decline may be behind us.

SEC Filings Deep Dive

I analyzed 86 SEC filings across 5 years: 5x 10-K, 15x 10-Q, 61x 8-K, and 5x DEF 14A. No amendments (10-K/A or 10-Q/A) were filed — a positive indicator of clean financial reporting.

Revenue Breakdown & Customer Concentration

| Revenue Segment | FY2023 | FY2024 | FY2025 |

|---|---|---|---|

| Product (Energy Server) | $975M | $1,085M | $1,531M |

| Installation | $93M | $122M | $204M |

| Service | $183M | $214M | $228M |

| Electricity | $82M | $53M | $60M |

| Related Party Revenue | $487M (37%) | $339M (23%) | $892M (44%) |

Management Credibility Scorecard

| Promise | Outcome | Verdict |

|---|---|---|

| Expand into data centers | AEP 1 GW deal + Oracle/hyperscaler contracts | Delivered |

| Achieve operating profitability | FY24 op income $23M, FY25 $73M | Delivered |

| Generate positive cash flow | FY24 OCF $92M, FY25 OCF $114M | Delivered |

| Electrolyzer as major product line | Shelved. $21.8M write-down in FY25. | Missed |

| Hydrogen market to drive revenue | Premature. Revenue negligible. | Missed |

Rating: Moderate Credibility. Management delivered on the core business thesis (profitability, data center pivot, cash flow) but missed on hydrogen/electrolyzer. The data center strategy pivot proved exceptionally well-timed. KR Sridhar has been CEO since founding — providing continuity but raising governance independence questions as he also serves as Chairman.

Debt Schedule

| Instrument | Rate | Maturity | Principal |

|---|---|---|---|

| 0% Convertible Senior Notes | 0.0% | Nov 2030 | $2,500M |

| 3.0% Green Notes | 3.0% | Jun 2029 | $75M |

| 3.0% Green Notes | 3.0% | Jun 2028 | $100M |

| $600M Revolving Credit Facility | Variable | Dec 2030 | $0 drawn |

No near-term maturities until June 2028. The 0% coupon on $2.5B means zero cash interest on the dominant tranche, creating a powerful interest income arbitrage ($34M interest income in FY25 from the cash). The $600M undrawn revolver provides additional liquidity. Accumulated deficit stands at ($3.99B). Bloom holds 380 U.S. patents + 183 pending, providing a genuine IP moat in solid oxide technology.

News & Catalysts

I analyzed 77 articles covering BE from December 2025 through March 2026. The breakdown: ~46 bullish, ~21 neutral, ~10 cautious/bearish. The dominant narrative: Bloom Energy is the consensus pick for AI data center power infrastructure.

Major Deal Flow

| Partner | Deal Size | Details |

|---|---|---|

| Brookfield | $5B (5 years) | Preferred on-site power provider for AI factories. 55 MW complete, 230 MW contracted. |

| AEP | $2.65B | Exercised bulk of 900 MW purchase option. Largest single deal in company history. |

| Oracle | — | 55-day fuel cell deployment for AI factory. Bloom issued Oracle warrant for up to 5% of shares. |

| Wells Fargo | $600M | Credit facility (undrawn). Announced Jan 2026. |

Analyst Ratings

| Firm | Rating | Target | vs. $154.51 |

|---|---|---|---|

| China Renaissance | Buy | $207 | +34% |

| Citigroup | Neutral | $162 | +5% |

| TD Cowen | Hold | $160 | +4% |

| Barclays | Equal Weight | $153 | -1% |

| Mizuho | — | $110 | -29% |

| Trefis | Bearish | $95 | -38% |

| Jefferies | Underperform | $31 | -80% |

Consensus target is ~$150 — slightly below current price. The stock has outrun every traditional analyst model. The $207 vs. $31 spread reflects extreme uncertainty about the business trajectory.

Upcoming Catalysts

- Q1 2026 earnings (May 2026) — First quarter toward $3.1B annual target. Margins will be under a microscope.

- Brookfield deployment milestones — 230 MW contracted through mid-2027. Each milestone de-risks execution.

- Additional hyperscaler deals — Oracle, Walmart, Amazon, Equinix already customers. New wins would expand TAM.

- Oracle/OpenAI fallout — Further project cancellations or reallocations would hit sentiment.

- AI capex sustainability — Any pullback in $600B hyperscaler spending would be bearish.

Market Sentiment

Bloom Energy is the undisputed media darling of the AI-energy infrastructure trade. Internet sentiment score: 6.5/10 — strong business conviction, weakening momentum signals, rising valuation concern, absent retail base.

Reddit — A Ghost Town

Despite being one of the best-performing stocks of the past year (600%+ gain), BE has essentially zero retail Reddit engagement. This is extremely unusual — most 600% runners generate massive WSB/retail attention.

- r/wallstreetbets: Not in top picks. Zero traction.

- r/stocks: Not in top 30 discussed tickers.

- ApeWisdom: ~2 mentions/day across all of Reddit.

- AltIndex: 0–1 mentions/month. Effectively invisible.

This means the 10x move was driven almost entirely by institutional flows (Druckenmiller $64M, BlackRock endorsement, Brookfield partnership) and financial media — not retail FOMO. Implication: there is no retail base to provide a floor if institutions sell.

StockTwits — Fading Volume

StockTwits sentiment remains bullish in tone, but daily mentions dropped 59% — from ~449/day (Oct 2025) to ~186/day (Mar 2026). Bullish sentiment with declining volume is a classic "believers holding, but no new converts" pattern.

Financial Media Sentiment Shift

The media tone has shifted from "buy the dip" (Jan 2026) to "proceed with caution" (Mar 2026). Motley Fool, the highest-volume publisher, has moved from pure bullish to questioning: "Is It Too Late?", "Buy, Sell, or Hold?", "Is This a Millionaire Maker?" — the framing itself signals narrative fatigue.

Insider & Institutional Activity

CEO KR Sridhar — The $51M Sell Program

| Date | Shares Sold | Price | Value | 10b5-1? |

|---|---|---|---|---|

| Feb 2026 | 200,000 | ~$170 | $34M | NO |

| Aug 2025 | 257,000 | ~$51 | $13M | Expiring options |

| Nov 2024 | 120,000 | ~$25 | $3M | — |

| Mar 2025 | 35,600 | ~$23 | $820K | — |

The Feb 2026 discretionary sale at $170 is the most concerning data point. When the founder/CEO of a company that has never been consistently profitable makes a discretionary sale near all-time highs — not under a pre-arranged 10b5-1 plan — he is telling you with his wallet that the stock is fully valued. He still holds ~6.2M shares, so he retains significant skin in the game, but the pattern is clear: take money off the table at every opportunity.

Other Named Insiders — All Sellers

| Insider | Title | Total Sales | Notes |

|---|---|---|---|

| Soderberg | Chief Legal Officer | $8M+ | 10b5-1 plan. Systematic selling. |

| Bush | Director | $5.1M | Significant director-level selling. |

| Snabe | Director | $2.9M | Sold to ZERO shares. Complete exit. |

| Zervigon | Director | $2.8M | Selling into strength. |

| Joshi | Chief Commercial Officer | $1.8M+ | Selling into the rally (Nov 2025–Feb 2026). |

Convertible Bond Holder Warning

A significant portion of BE's "institutional ownership" comes from convertible bond funds — not long-only equity buyers. Columbia Convertible Securities Fund holds 16.91% of its fund in BE (their largest position). SPDR Bloomberg Convertible Securities ETF holds 14.58%. These holders are likely delta-hedging with short equity positions, meaning the reported 85.90% institutional ownership dramatically overstates genuine long-only equity demand. For investors looking to trade around volatile positions like this, understanding cash-secured puts can be a valuable approach.

Risk Factors

| Risk | Probability | Impact | Details |

|---|---|---|---|

| Customer Concentration | HIGH | SEVERE | Top 3 = 68% of revenue. Brookfield = 43%. One deal cancellation caused a 15.5% single-day drop. |

| Valuation Compression | HIGH | SEVERE | 21x P/S vs. 2.35x industry. Any earnings miss triggers sharp multiple compression. |

| Execution / Scaling Risk | MODERATE | HIGH | Must grow revenue 58% in one year ($2B → $3.2B) while managing margin compression. |

| Convertible Dilution | HIGH | MODERATE | $2.5B 0% convertible notes + Oracle warrant (5% of Class A). Shares grew 22% in FY25. $277M unrecognized SBC to vest. |

| AI Capex Slowdown | MODERATE | SEVERE | Entire thesis rests on $600B hyperscaler spend. Any pullback undermines demand. |

| Insider Selling Signal | CONFIRMED | MODERATE | Every insider with material non-public information is selling. Nobody is buying. |

| Natural Gas Dependency | LOW-MOD | MODERATE | Fuel cells run on natural gas. May not qualify as "clean energy" in ESG-mandated markets. Regulatory risk. |

| Tariff / Trade Risk | MODERATE | MODERATE | Recent SEC filings escalated tariff risk language. Supply chain has international exposure. |

Conclusion & Price Targets

Three-Scenario Earnings Model

| Scenario | FY27 Revenue | FY27 GAAP EPS | Target P/S | 12-Mo Target | vs. $154.51 |

|---|---|---|---|---|---|

| Bear (25%) | $3,400M | -$0.30 | 6x | $66 | -57% |

| Base (50%) | $4,200M | $1.35 | 10x | $135 | -13% |

| Bull (25%) | $5,000M | $3.25 | 15x | $242 | +57% |

| Probability-Weighted Target | $155 | ~0% | |||

Bull Case ($242)

- Revenue exceeds $3.3B guidance in FY26

- Gross margins expand to 35%+ with service revenue and scale

- New hyperscaler deals beyond Oracle/AEP/Brookfield

- First meaningful GAAP profit in FY27

- Hydrogen optionality emerges as long-dated call option

Bear Case ($66)

- Manufacturing bottlenecks prevent hitting guidance

- Margin compression continues — Brookfield deals at low margins

- Customer cancellation or delay (Oracle/OpenAI was a preview)

- AI capex cycle decelerates — hyperscalers cut spend

- Convertible dilution overwhelms any EPS improvement

Action Plan

| If You... | Action | Rationale |

|---|---|---|

| Own BE | Trim into strength above $170. Hold core position if cost basis is below $100. | Risk/reward is unfavorable at 0.6:1. Protect profits while maintaining exposure to bull case. |

| Don't Own BE | Wait for $115–125 entry or a material catalyst miss that resets expectations. | At $120, P/S compresses to ~14x and risk/reward improves to ~1.5:1. Patience is the edge. |

| Want Options Exposure | Consider selling cash-secured puts at $120–130 strikes for premium collection. | With beta of 3.16, options premiums are elevated. Get paid to wait for a better entry. See my guide to lowering stock basis with options. |

A note on Druckenmiller: His $64M position is 1–2% of his portfolio at most — a call option on the AI energy thesis, not a conviction bet. He also sold $170M of NVIDIA at a similar inflection. Hedge fund legends allocate small to high-risk/high-reward plays. Retail investors who size this as a core holding are taking a fundamentally different risk.

As this BE stock analysis highlights, the short squeeze from 53M to 22M shares — which was likely a primary driver of the $15 → $155 move — is largely played out. With mechanical covering mostly complete and insiders aggressively selling into the rally, the question is whether fundamental demand can sustain a $43B market cap for a company where every person with material non-public information is selling, and nobody is buying. I explore more ideas for income strategies on this website.

Frequently Asked Questions

Is BE a good stock to buy?

At the current price of $154.51, BE presents an unfavorable risk/reward. The AI data center power thesis is real and Bloom Energy is the clear leader in fuel cell deployment — but the stock already prices in 3–5 years of flawless execution at 21x P/S and 100–165x forward P/E. Every Wall Street analyst target ($68–$162) is at or below the current price. My probability-weighted 12-month target is $155, essentially flat. A better entry point would be $115–125 following a catalyst miss or broader market correction.

What is the BE price target for 2026?

My base case 12-month price target is $135 (10x FY27 P/S), with a probability-weighted target of $155 accounting for bull and bear scenarios. Bull case is $242 (if revenue exceeds guidance and margins expand). Bear case is $66 (if execution falters or AI capex slows). The consensus analyst target is ~$150, confirming the stock has largely outrun fundamental models.

Should I buy or sell BE?

HOLD. If you own it with a low cost basis, trim into strength above $170 but maintain a core position for the bull case. If you don't own it, wait for a pullback to $115–125 or a material catalyst miss. The insider selling pattern — CEO sold $34M discretionary at $170, SK ecoplant dumped $276M, 119 out of 120 insider trades are sales — is the most one-sided I have documented in any stock analysis on this website.

What is the BE stock forecast for 2026 and beyond?

The near-term trajectory depends on Q1 2026 earnings (May 2026) and whether Bloom can demonstrate progress toward $3.1–3.3B in annual revenue without further margin compression. If the company hits guidance and margins stabilize, the stock could retest the $180 all-time high. Longer-term, the fuel cell market is projected to reach $18.16B by 2030 (26.3% CAGR), and Bloom is the dominant SOFC player. The hydrogen economy represents additional optionality, though the electrolyzer write-down suggests this catalyst is further out than initially hoped. The biggest long-term risk is that the 0% convertible notes create significant dilution as they convert, limiting per-share earnings growth even if the business scales.

Sources: SEC Filings (10-K, 10-Q, 8-K, DEF 14A), Finviz, Polygon.io, Google News, Reddit, StockTwits, Motley Fool, Benzinga, Investing.com, GlobeNewswire. Report compiled March 15, 2026.