BYND (Beyond Meat) Stock Analysis: Sell | $0.40 Target

Table of Contents

Executive Summary

This BYND stock analysis covers Beyond Meat's fundamentals, technicals, SEC filings, market sentiment, and insider activity as of April 21, 2026, with the stock trading at $1.16 after a 65% intraday rally on April 20. Here is my bottom line on this Beyond Meat stock analysis:

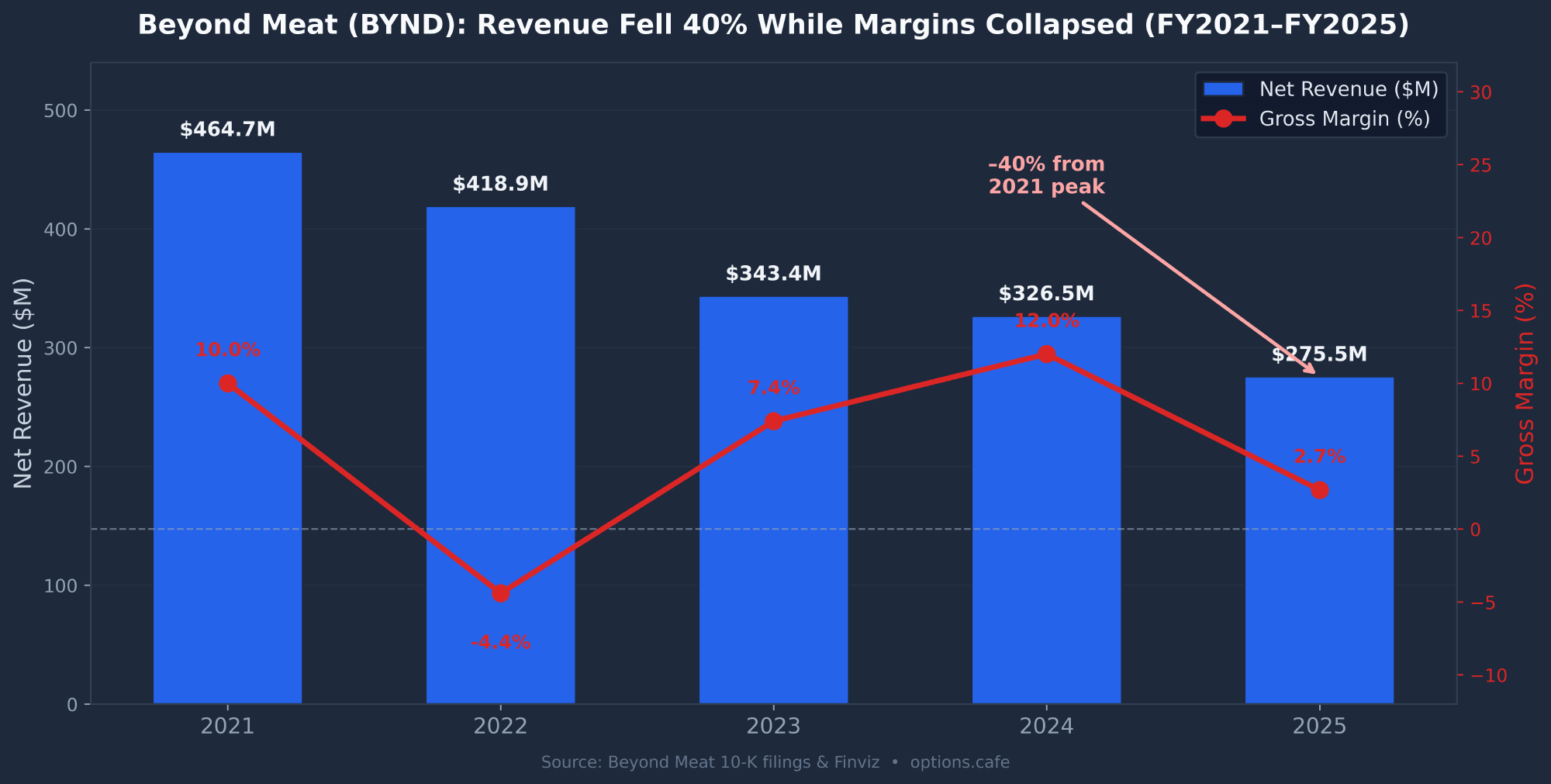

- The operating business is in terminal decline. Revenue has fallen every year for five straight years, from a $464.7M peak in 2021 to $275.5M in 2025 (−40%). Management has already pre-guided Q1 2026 down again.

- Q4 2025 gross margin turned negative (−0.77%). Beyond Meat is selling product for less than it costs to make. Even with zero overhead, the company would lose money on every unit.

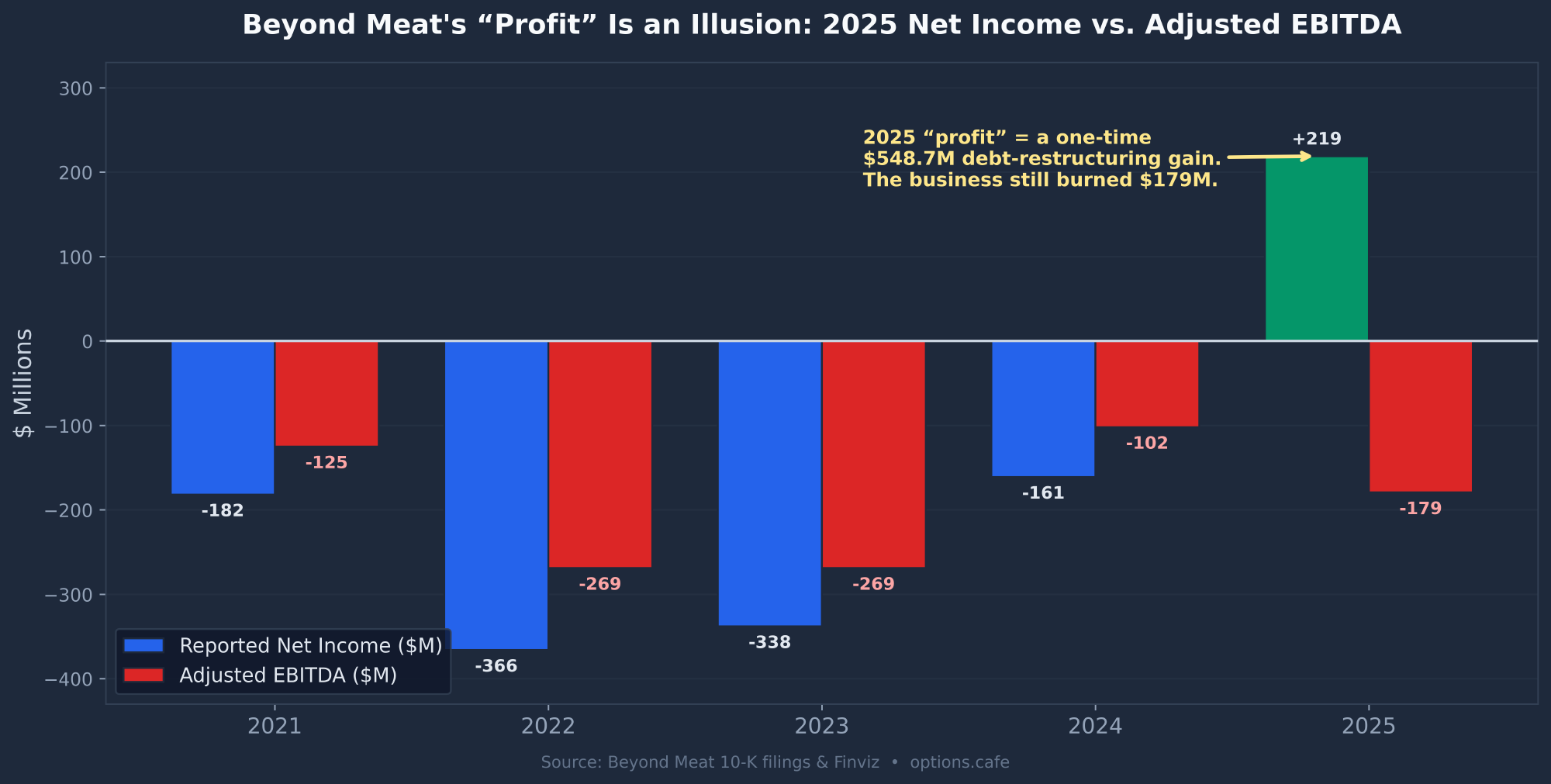

- The 2025 "profit" is an accounting illusion. The headline $219M net income is a $548.7M non-cash gain on debt restructuring masking a roughly $330M operating loss. Adjusted EBITDA was −$179M — and it got worse year-over-year despite the bailout.

- Management credibility is shattered. The FY2025 10-K admits "material weaknesses in internal control over financial reporting" and a "potential need to restate." It was filed four days late. Ten-plus law firms have filed securities class actions.

- The insider signal is maximally bearish. Zero open-market insider purchases in five-plus years through a 99% decline. The CFO — who is also the principal accounting officer — sold $253K of stock at $0.60 one week before the rally.

The 4/20 rally is a short squeeze on a broken business, not the start of a turnaround. I rate Beyond Meat a SELL with a 12-month price target of $0.40–$0.55.

| Report | Signal | Key Finding | Weight |

|---|---|---|---|

| Fundamentals | BEARISH | 5-year revenue decline, Q4 2025 gross margin negative, EV/Sales 3.0x for a shrinking business | 25% |

| SEC Filings | BEARISH | Material weaknesses admitted, restatement risk, $38.9M litigation accrual, PIK debt compounding | 20% |

| Technical | MIXED | RSI 79 (overbought), price below SMA 200 ($1.64). Prior squeezes reverted within 2 weeks. | 15% |

| News & Events | BEARISH | 45 of 50 recent articles negative; WSJ/MarketWatch framing as a cautionary tale; 10+ class actions | 15% |

| Insider/Institutional | BEARISH | Zero insider buys in 5 years; CFO sold at the $0.60 low; institutions are arbitrageurs, not longs | 15% |

| Sentiment | MIXED | Retail squeeze fever short-term; long-term press and analysts unanimously bearish | 10% |

| COMPOSITE | BEARISH (HIGH CONVICTION) | 4 of 6 reports clearly bearish; the other 2 are mixed with no clean bullish signal anywhere. | 100% |

Investment Thesis

Beyond Meat is a classic terminal-decline consumer-staples fade, complicated by an October 2025 debt-for-equity restructuring that produced cosmetic balance-sheet improvement at the cost of roughly 6x equity dilution. The underlying business — plant-based meat analogs — is in a sustained secular demand decline. This is not just BYND's problem: in 2025, Unilever sold The Vegetarian Butcher to JBS (a conventional meat company), Daring Foods was acquired by V2 Food, and Vital Meat was bought by Gourmey. The largest consumer-packaged-goods company in the world concluded the category destroys value and exited. Beyond Meat is the last public pure-play standing — which is not a strength, it's a lack of acquirers.

The October 2025 Exchange Offer and the $100M delayed-draw term loan from Unprocessed Foods (an affiliate of the Ahimsa Foundation) bought BYND roughly 12–18 months of runway. But the new 2030 Notes are PIK-toggle (7% interest that can be paid in more debt) and second-lien — meaning the debt compounds while the company keeps burning cash. Absent a dramatic and unprecedented operational reversal, the mathematical endpoint is a second debt-for-equity restructuring by 2028–2030 that wipes out existing common equity.

The April 20, 2026 rally (+65% intraday on 220M shares) is a short-squeeze ignition layered on a genuine but tiny catalyst (the Big Geyser beverage distribution deal). Short float is 31.61% with rising borrow rates — a similar setup to the October 2025 squeeze that ran from $0.50 to $7.69 and then collapsed within ten days. History strongly suggests this squeeze exhausts within two to four weeks, after which the stock gravitates back toward its fundamentally-anchored range of $0.40–$0.80. The August 31, 2026 Nasdaq compliance deadline then forces a binary resolution.

The strongest counterargument is that this is a meme stock with a retail cult following where fundamentals don't matter. That is partially true over days and weeks — but it loses its force over six to twelve months. BYND has two prior failed squeezes in 2025 (July and October), and both fully retraced. That is exactly why my recommendation is SELL over a 6–12 month window, not "never touch it." Short-term traders can play the volatility; long-biased investors should own none of it.

Fundamental Analysis

Company Overview

Beyond Meat, Inc. (NASDAQ: BYND) makes plant-based meat analogs — burgers, sausage, chicken strips, and beef crumbles — and is expanding into protein beverages via its Beyond Immerse line. Founded in 2009 by Ethan Brown and Brent Taylor, the company IPO'd on May 2, 2019 at $25 per share and briefly traded above $234. It rebranded from "Beyond Meat" to "Beyond" in March 2026 (the legal name is unchanged), telegraphing a pivot away from the collapsing plant-based meat category. The company employs roughly 589 people and is headquartered in El Segundo, California.

Price History — A Five-Year Collapse

The five-year total return is −99.1%. A $10,000 position bought near the 2020 lows would be worth roughly $88 today. This is a textbook illustration of a thematic IPO bubble deflating as the underlying category failed to materialize.

| Period | Price Range | Event |

|---|---|---|

| Jul 2019 | $234 peak | All-time high. McDonald's / Dunkin' / KFC partnership hype. |

| 2021 | $50 – $140 | Peak revenue year ($464.7M). Consumer interest beginning to wane. |

| 2022–2024 | $5 – $50 | Margins collapse, mass layoffs, category-wide decline becomes visible. |

| Oct 2025 | $0.60 → $7.69 → $1.50 | 52-week high $7.69 on a WSB squeeze. Exchange Offer closes Oct 30 (massive dilution), then collapse. |

| Mar 2026 | $0.50 – $1.10 | 52-week low $0.50. Nasdaq deficiency, 10-K delay, rebrand, Q4 earnings miss. |

| Apr 2026 | $0.66 – $1.16+ | +65% intraday Apr 20 on 220M shares — squeeze re-ignition plus the Big Geyser deal. |

Income Statement — Five Years of Decline

| Metric ($M) | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Revenue | 464.7 | 418.9 | 343.4 | 326.5 | 275.5 |

| YoY Growth | +14.2% | −9.9% | −18.0% | −4.9% | −15.6% |

| Gross Margin | ~10% | −4.4% | 7.4% | 12.0% | 2.68% |

| Operating Loss | (182) | (337) | (203) | (163) | (211) |

| Net Income | (182) | (366) | (338) | (161) | +219* |

| Adjusted EBITDA | (125) | (269) | (269) | (102) | (179) |

*2025 net income of +$219M is an accounting artifact: a $548.7M non-cash gain on the debt restructuring. The underlying operation lost roughly $330M.

The "Profit" That Isn't

The single most important chart in this Beyond Meat stock analysis is the gap between reported net income and Adjusted EBITDA. In 2025, the headline net income flipped positive to +$219M — but cash-based Adjusted EBITDA stayed deeply negative at −$179M. The entire "profit" is a one-time, non-cash debt-restructuring gain.

Valuation — A Premium for a Shrinking, Cash-Burning Business

| Metric | Value | Metric | Value |

|---|---|---|---|

| Market Cap | $537.7M | Enterprise Value | $837.5M |

| P/S (TTM) | 1.95x | EV/Sales | 3.04x |

| P/E | N/A (no real earnings) | EV/EBITDA | N/A (EBITDA −$179M) |

| Book Value / Share | −$0.002 | Forward EPS (est.) | −$0.40 |

| Analyst Target (mean) | $0.66 (−43%) | Recommendation | 4.14 (Sell) |

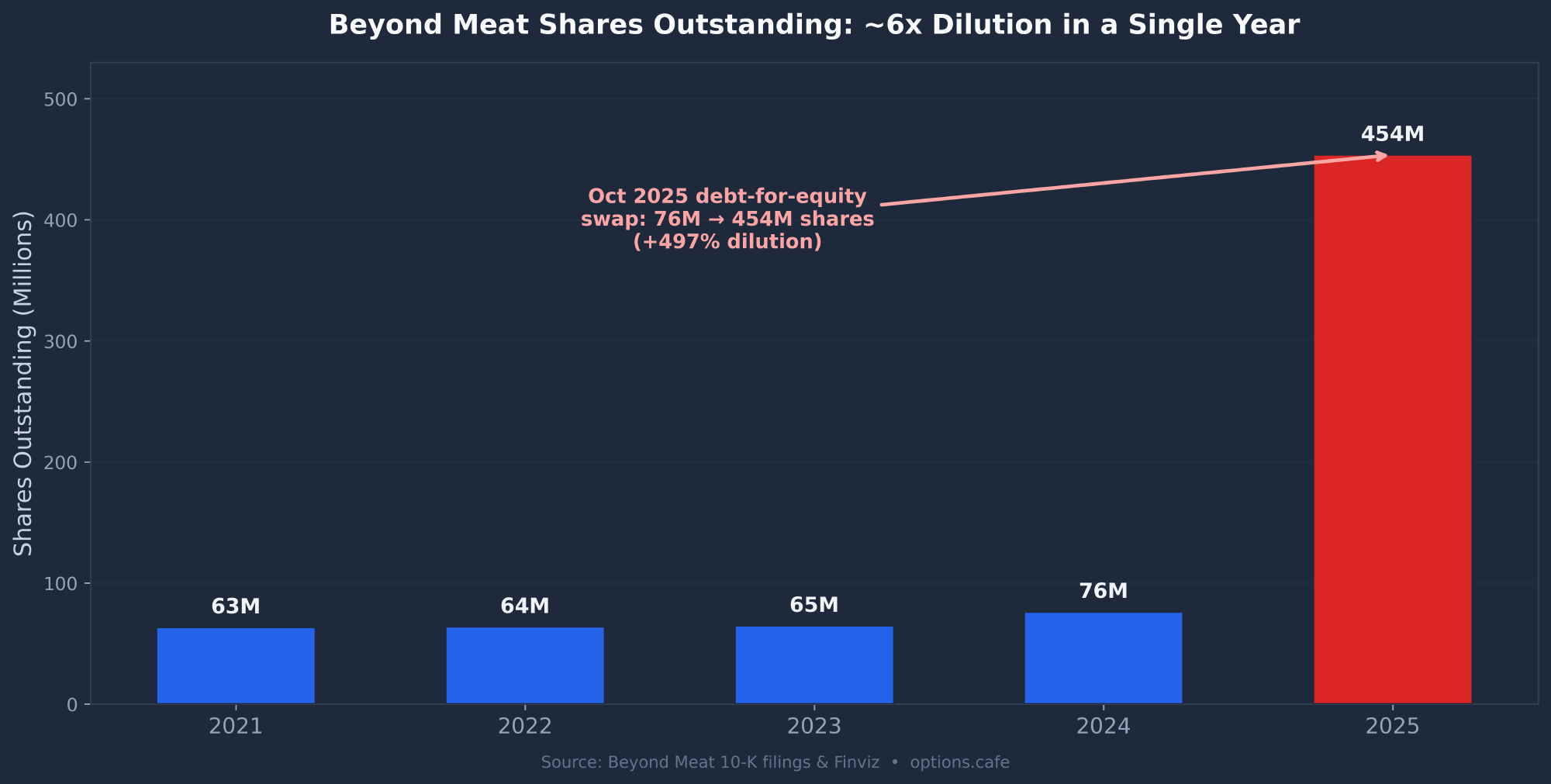

Balance Sheet & Dilution

| Balance Sheet ($M) | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| Cash & Equivalents | 309.9 | 190.5 | 131.9 | 203.9 |

| Total Debt | 1,133.6 | 1,137.5 | 1,141.5 | 415.8 |

| Total Stockholders' Equity | (203.5) | (513.4) | (601.2) | (1.0) |

| Shares Outstanding (M) | 63.8 | 64.6 | 76.1 | 453.7 |

The debt reduction from $1.13B to $416M looks like progress, but it's cosmetic. The 2030 Notes carry a PIK toggle, so interest compounds into principal; there is a $39.2M embedded derivative liability and $5.1M of warrant liabilities attached to the term loans. Meanwhile, share count exploded from 76M to 453.7M — a roughly 6x dilution in a single year. With the business still burning cash, the only path to liquidity is more equity issuance at prices at or below today's.

Peer Comparison

| Metric | BYND | TSN (Tyson) | HRL (Hormel) | GIS (Gen. Mills) |

|---|---|---|---|---|

| P/S (TTM) | 1.95x | ~0.6x | ~1.5x | ~1.8x |

| EV/Sales | 3.04x | ~0.8x | ~1.7x | ~2.4x |

| Gross Margin | 2.68% | ~12% | ~17% | ~35% |

| EBITDA | Deeply negative | Positive | Positive | Positive |

| Revenue Trend | 5 yrs declining | Stable | Stable | Stable |

Technical Analysis

Technical Summary

BYND has two completely different charts. The long-term weekly is a brutal, unbroken downtrend from $22.87 (early 2023) to $0.50 (October 2025) — a 98% decline with repeated failed recoveries. The short-term daily shows "distressed volatility" with two prior squeeze attempts: July 2025 ($3.50 → $4.82 → $0.50) and the October 2025 monster ($0.50 → $7.69 → $0.80 in ten days). The April 20 spike is squeeze attempt number three. RSI(14) at 79.4 is deeply overbought, and price is +68% above its SMA 20 yet still −29% below its SMA 200 ($1.64). That is a textbook mean-reversion-down setup — and also a launchpad if the squeeze gains momentum.

| Indicator | Value | Signal |

|---|---|---|

| Price | $1.16 | NEUTRAL |

| SMA 50 | $0.73 | Price +59% (extended) |

| SMA 200 | $1.64 | BEARISH (price −29%) |

| RSI (14) | 79.41 | OVERBOUGHT |

| MACD | +0.040 / Signal −0.011 | Fresh bull crossover |

| Beta | 2.70 | EXTREME VOLATILITY |

| ATR (14) | $0.09 (~8% of price) | VERY HIGH |

| Relative Volume | 6.19x | SQUEEZE SIGNATURE |

Support & Resistance Levels

| Support | Price | Significance |

|---|---|---|

| S1 | $0.95–$1.00 | Round-number + Nasdaq minimum-bid compliance target. |

| S2 | $0.72–$0.73 | SMA 10 + SMA 50 confluence. Strong. |

| S3 | $0.60–$0.65 | Where the CFO sold on Apr 13; multiple March–April bounces. |

| S4 | $0.50–$0.52 | 52-week low. Critical floor. |

| Resistance | Price | Significance |

|---|---|---|

| R1 | $1.17–$1.20 | April 20 intraday high. Immediate breakout level. |

| R2 | $1.64–$1.65 | SMA 200 — the major pivot. A close above breaks the 3-year downtrend. |

| R3 | $2.00 | Psychological + October 2025 post-squeeze retest. My thesis-broken level. |

| R4 | $7.69 | 52-week high (Oct 21, 2025). The squeeze ceiling. |

SEC Filings Deep Dive

I reviewed 21 SEC filings spanning 2021 to April 2026 — five 10-Ks, three recent 10-Qs, ten 8-Ks, and two proxy statements. The filings tell a far more alarming story than the headline numbers. Critically, the FY2025 10-K was filed four days late and explicitly acknowledges "material weaknesses in internal control over financial reporting" and a "potential need to restate financial statements."

Management Credibility Scorecard — Promise vs. Delivery

| Promise / Guidance | Outcome |

|---|---|

| "Continued revenue growth as the plant-based category expands" (FY2021) | MISSED (−40%) |

| "Restoring gross margin to historical levels (25%+)" (FY2023) | MISSED (2.68%) |

| "EBITDA breakeven expected in 2025" (FY2023) | MISSED (−$179M) |

| "Refinancing strategy positions the company for the future" (FY2024) | PYRRHIC (6x dilution) |

| "Internal controls over financial reporting are effective" | MATERIAL WEAKNESS |

| "Beyond Immerse launches, expanding into beverages" (Jan 2026) | DELIVERED |

In five years of filings, management has not delivered a single multi-quarter revenue inflection upward. The one promise kept — the Beyond Immerse beverage launch — contributes a tiny fraction of the $275M core business. The presence of John R. Boken as Interim Chief Transformation Officer, a veteran restructuring advisor, signals the company is positioning for a corporate restructuring rather than a growth turnaround.

Debt Structure (as of Dec 31, 2025)

| Instrument | Amount | Terms |

|---|---|---|

| 2027 Notes (residual) | $29.5M | 0% coupon, unsecured, due Mar 2027 |

| 2030 Notes | $308.4M | 7% PIK toggle, second-lien secured, convertible |

| Delayed-Draw Term Loans | $77.9M | Secured (Unprocessed Foods / Ahimsa Foundation), warrants attached |

| Litigation Accrual | $38.9M | Up from $7.25M a year earlier — class actions escalating |

Key Red Flags Summary

- Material weaknesses in ICFR admitted in the FY2025 10-K, with a stated "potential need to restate."

- 10-K filed four days late after disclosing accounting errors tied to an inventory review.

- Two Nasdaq non-compliance notices in five weeks (minimum bid price + late filing).

- $38.9M litigation accrual, up 5x year-over-year, with 10+ securities class actions pending.

- Category exits: the 10-K itself discloses Unilever selling The Vegetarian Butcher to JBS, Daring Foods to V2 Food, and Vital Meat to Gourmey — all distressed exits in 2025.

News & Catalysts

Media coverage is extraordinarily high for a $537M-cap stock. Of roughly 50 articles tracked over the past 90 days, 45 are negative. The dominant narrative is "from a $14 billion powerhouse to a penny stock." The five positive articles are all about the Big Geyser deal, the Beyond Immerse drinks launch, or a climate certification.

Key Headlines

| Date | Headline | Sentiment |

|---|---|---|

| Apr 16 | Beyond Meat partners with Big Geyser — Beyond Immerse drinks reach 26,000+ NYC outlets (+18.5%) | Bullish |

| Apr 15 | Moneywise: "The CEO got a raise and blames Americans for the collapse" | Bearish |

| Apr 12 | MarketWatch: "How Beyond Meat sank from a $14 billion powerhouse to a penny stock" | Bearish |

| Apr 09 | Second Nasdaq non-compliance notice — 10-K filed four days late | Bearish |

| Apr 02 | Just Food: "Beyond Meat expects Q1 sales to be down again" | Bearish |

| Mar 25 | WSJ: "Beyond Meat delays financial report after identifying accounting errors" | Bearish |

Analyst Ratings

| Firm | Rating | Target |

|---|---|---|

| Mizuho | Underperform | $1.50 |

| Argus | Sell | — |

| JP Morgan | Underweight | — |

| TD Cowen | Underperform | — |

| Consensus | Sell (4.14) | $0.66 (−43%) |

There has not been a single analyst upgrade to "Buy" or equivalent in more than four years. The only recent "upgrade" was Argus moving from Sell to Hold in February 2024 — promptly reversed back to Sell in September 2025.

Upcoming Catalysts

| Catalyst | Timing | Direction |

|---|---|---|

| Q1 2026 earnings (pre-guided down) | ~May 2026 | Bearish |

| Big Geyser initial revenue data point | ~Jun 2026 | Uncertain |

| Nasdaq compliance deadline (10 closes ≥ $1.00) | Aug 31, 2026 | BINARY |

| Possible reverse stock split execution | H2 2026 | Bearish |

Market Sentiment & the Squeeze

Overall sentiment is bifurcated by time horizon. Over days and weeks, retail is extremely bullish on the squeeze setup. Over quarters and years, the financial press, the analyst community, and informed observers are nearly unanimously bearish. When the meme cohort and the financial press disagree this strongly, the meme side historically wins for days to weeks and the financial side wins for months to years.

I want to address the squeeze directly, because it is the single strongest argument against my SELL thesis — and it deserves an honest answer.

The Bull (Squeeze) Case

- Short float 31.61%, 141.7M shares short, short ratio 3.98 days

- 6.19x relative volume on Apr 20 (220M shares) — squeeze ignition signature

- Precedent: Oct 2025 ran $0.50 → $7.69 in six trading days

- Big Geyser deal is the first credible growth initiative in years

- Rising borrow rates can force a gamma + short squeeze

Why the Squeeze Fades

- Both 2025 squeezes (July and October) gave back 70%+ within two weeks

- The Oct 2025 squeeze ended in a debt-for-equity dilution event

- RSI 79 + price below SMA 200 = classic mean-reversion-down

- Shorts keep reloading because the bankruptcy/restructuring payoff outweighs squeeze risk

- Nothing about the squeeze changes negative gross margins or the Aug 31 deadline

The most-upvoted Reddit posts capture the mood perfectly: a thread titled "$BYND baggies right now" drew 34,000 upvotes mocking the people who bought the last squeeze at $7+, while another user posted "FULL PORTED MY LIFE SAVINGS INTO BYND." This is gambling behavior, not investing. The squeeze is real and tradable for nimble short-term traders — but it is a reason to take volatility seriously, not a reason to own the business.

Insider & Institutional Activity

Insider Trading: Maximally Bearish

Over five-plus years and 25+ tracked transactions, there have been zero open-market insider purchases. Every transaction has been a sale. No executive has bought a single share with their own money through the entire 99% decline.

Institutional Ownership: A Hollow 46%

The top 10 institutional holders look substantial at ~46% cumulative, but the composition is the story. Context Capital, Point72, Wolverine, D.E. Shaw, CSS, LMR, and Two Sigma are multi-strategy, quant, and convertible-arbitrage funds — they almost certainly hold BYND common as a hedge against the 2027/2030 convertible notes or for options market-making, not as a conviction long. Their stock positions are offset by short positions elsewhere. The only genuine "long" holders are BlackRock and Vanguard, who buy mechanically because BYND is in the Russell 2000 — and who would be forced sellers if a delisting removed it from the index.

The real controlling holder is Unprocessed Foods, LLC (an affiliate of the Ahimsa Foundation, a vegan-focused nonprofit). They are a mission-aligned distressed lender: unlikely to push for liquidation, but holding PIK-toggle second-lien debt that lets them take the company in a future swap — at the expense of common shareholders.

Risk Factors

Because this is a bearish call, the "risks" here are largely the things that could go right for the company (and wrong for a short), plus the structural dangers to any holder.

| Risk / Scenario | Probability | Impact |

|---|---|---|

| Nasdaq reverse split triggered. Sub-$1 reverse splits decline further ~70% of the time within six months post-split. | ~60% | HIGH |

| Accounting restatement. Material weaknesses already admitted. Would trigger an SEC inquiry and more class actions. | ~45% | CATASTROPHIC |

| Major retailer delists products. A Walmart, Kroger, or Costco shelf-space cut would be devastating given customer concentration. | ~35% | HIGH |

| Second debt-for-equity restructuring by 2028. PIK debt math points here; common equity gets wiped out. | ~25% | CATASTROPHIC |

| Short squeeze sustains (risk to the short). Beta 2.70 means a violent multi-hundred-percent move is possible in days. | ~15% | HIGH (to shorts) |

Conclusion & Price Targets

Earnings Model — Three Scenarios

| Metric | Bear Case | Base Case | Bull Case | |||

|---|---|---|---|---|---|---|

| FY26E | FY27E | FY26E | FY27E | FY26E | FY27E | |

| Revenue ($M) | $225 | $185 | $245 | $220 | $275 | $290 |

| Gross Margin | ~2% | 0% | 5% | 8% | 8% | 12% |

| Adj. EBITDA ($M) | −180 | −170 | −140 | −115 | −110 | −70 |

| Implied Price | $0.20–$0.30 | $0.40–$0.55 | $1.64–$2.50 | |||

Base/Bear Target: $0.40–$0.55 (−53% to −66%)

- Squeeze unwinds within days to weeks (probability ~55–60%)

- Q1 2026 confirms revenue −15% or worse

- Nasdaq compliance fails → reverse split signals desperation

- 2030 PIK interest compounds into more debt

- Three valuation methods cluster at $0.20–$0.43

Bull Target: $1.64–$2.50 (squeeze)

- Short float stays above 25% and borrow stays tight

- Big Geyser shows early revenue momentum by Q3 2026

- No further accounting surprises

- Price clears the SMA 200 at $1.64 (probability ~25–30%)

- This is a trade, not an investment thesis

Action Plan

| Parameter | Recommendation |

|---|---|

| Direction | Short / avoid. Long-biased investors should own zero shares. |

| Preferred Vehicle | Put options (3–6 months out) to cap risk. Direct short borrow is expensive; defined-risk puts beat unlimited-loss short selling on a Beta-2.70 name. |

| Position Size | 0.5–1.5% of risk capital, maximum. Beta 2.70 and 8% daily ATR demand tiny sizing. |

| Entry | Wait for the squeeze to exhaust. Short a break of $1.00, or a pullback to RSI < 50. Do NOT short into a vertical rally at RSI 79. |

| Stop-Loss | $2.00 (thesis-broken). A 5-day close above $2.00 on sustained volume means exit the bearish view and reassess. |

| Profit Targets | Cover 50% at $0.66 (analyst target), 25% at $0.50 (prior low), hold 25% for $0.30–$0.40. |

The Bottom Line

This Beyond Meat stock analysis rates BYND a high-conviction SELL at $1.16 with a 12-month target of $0.40–$0.55. Beyond Meat is not a turnaround story — it is a secular decline story with a debt-for-equity swap that bought time but fixed nothing. Revenue has fallen for five straight years, Q4 2025 gross margin went negative, the 2025 "profit" is a one-time accounting gain, management has admitted material weaknesses in its financial controls, and the insider with the deepest visibility sold at the lows.

The 65% rally on April 20 is a tradable short squeeze in a terminally ill business. Sophisticated capital is signaling one thing unanimously: the stock is going lower. The only open question is how long the meme squeeze extends the exit opportunity. Use the rally to initiate short positions, not long positions — and respect the volatility with tiny position sizes and a hard stop at $2.00.

If you are looking for healthier setups, BYND is a useful counter-example: it fails every screen for the best stocks for the wheel strategy — negative margins, no earnings, and a balance sheet near zero equity. For traders who want to express a defined-risk bearish view, long puts are the cleaner vehicle than short stock. And if you would rather generate income on quality names instead, see my guide to the options wheel strategy and selling cash-secured puts.

For comparison, I've reached very different conclusions on other widely-debated names — a Buy on DraftKings (DKNG), and Hold ratings on Rivian (RIVN) and IonQ (IONQ). You can browse all my stock analysis reports for the full list.

Sources: SEC Filings, Finviz, Polygon.io, Google News, Reddit, Twitter/X. Report compiled April 21, 2026.

Frequently Asked Questions

Is BYND a good stock to buy right now?

No. Based on this analysis, Beyond Meat (BYND) is rated a SELL at $1.16 with a 12-month price target of $0.40–$0.55 (−53% to −66%). The business has declined for five straight years, Q4 2025 gross margin was negative (−0.77%), and the 2025 "profit" was a one-time debt-restructuring gain masking a roughly $330M operating loss. The April 2026 rally is a short squeeze, not a turnaround.

What is the BYND stock price target for 2026?

The Wall Street consensus price target for BYND is $0.66 — about 43% below the current $1.16. My base-case 12-month target is $0.40–$0.55, derived from peer EV/Sales, price-to-sales, and DCF methods that cluster around $0.20–$0.43. A bull-case squeeze scenario could reach the SMA 200 at $1.64 or the $2.00 psychological level, but that is a trade, not a fundamental valuation.

Should I buy or sell Beyond Meat stock?

The recommendation is to sell or avoid Beyond Meat, and for traders, to consider a defined-risk short via put options after the squeeze exhausts. Short-term traders can play the squeeze volatility with tiny position sizes, but long-biased investors should hold no position. The thesis-broken level is a sustained close above $2.00.

Will Beyond Meat get delisted from the Nasdaq?

It's a real and binary risk. Beyond Meat received a Nasdaq minimum-bid-price deficiency notice and must close at $1.00 or above for 10 consecutive trading days before August 31, 2026. If it cannot, the likely path is a transfer to the Nasdaq Capital Market and a reverse stock split — stockholders already pre-approved 30 alternative split ratios (1-for-2 through 1-for-50) in November 2025. Distressed reverse splits historically continue to decline post-split.

Why did Beyond Meat stock crash?

Beyond Meat (BYND) has fallen roughly 99% from its 2019 peak of $234 to about $1.16. The collapse reflects a broad decline in the plant-based meat category — U.S. meat-alternative sales have dropped sharply since 2021 on high prices, taste complaints, and "ultra-processed" concerns. Beyond Meat's revenue has now fallen for five straight years (from $464.7M in 2021 to $275.5M in 2025), Q4 2025 gross margin turned negative, and an October 2025 debt-for-equity swap diluted shareholders roughly 6x in a single year. A company once worth $14 billion now trades as a penny stock.

Is Beyond Meat going bankrupt?

Beyond Meat has not filed for bankruptcy, and the October 2025 debt-for-equity swap bought roughly 12–18 months of runway while cutting debt from $1.13B to $416M. But the company is still burning cash on negative gross margins, and the new 2030 Notes carry a 7% PIK toggle that compounds debt over time. The more probable path than a Chapter 11 liquidation is a second debt-for-equity restructuring by 2028–2030 that wipes out existing common shareholders — economically similar to bankruptcy for equity holders even if the company never formally files.

Will Beyond Meat stock recover?

My Beyond Meat stock forecast is bearish over a 6–12 month horizon, with a $0.40–$0.55 target. A durable recovery would require the plant-based meat category to inflect (no evidence of that yet), the Beyond Immerse beverage line to scale to $50M+, and the company to clear its August 2026 Nasdaq deadline without a reverse split. Short-squeeze rallies like the one in April 2026 can produce sharp temporary spikes, but both 2025 squeezes fully retraced. Until the fundamentals turn, rallies are exit opportunities, not recoveries.