CHWY (Chewy) Stock Analysis: Buy at $22.97 | $35 Target

Table of Contents

Executive Summary

This CHWY stock analysis covers Chewy Inc.'s fundamentals, technicals, SEC filings, market sentiment, and insider activity as of May 2026. Here is the bottom line on Chewy stock analysis at the current $22.97 print:

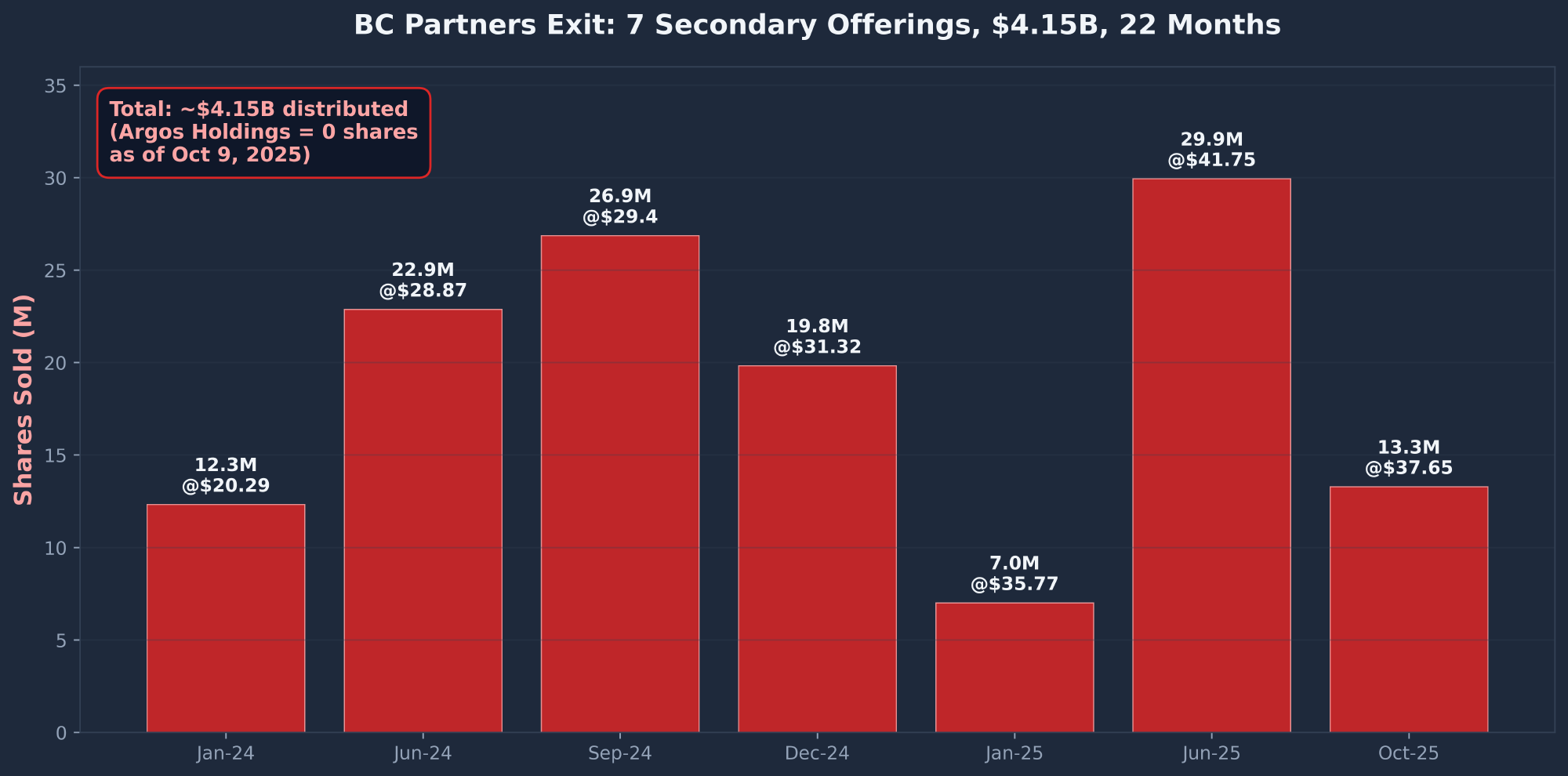

- BUY CHWY at $22.97 with a $35 price target. The thesis is structural, not earnings-driven. BC Partners just finished a $4.15B exit after 22 months and 9 secondary offerings. Smart money (Viking Global, Holocene Advisors) has begun replacing the freed-up float. The stock is at a 52-week low at the exact moment the largest structural overhang in the company's history was cleared.

- The business underneath is a debt-free free cash flow compounder. FCF grew 60x in four years — from $9M in FY2021 to $562M in FY2025 — on $0 traditional debt, $879M cash, and an undrawn $800M ABL facility. This is unusual for a low-margin retailer.

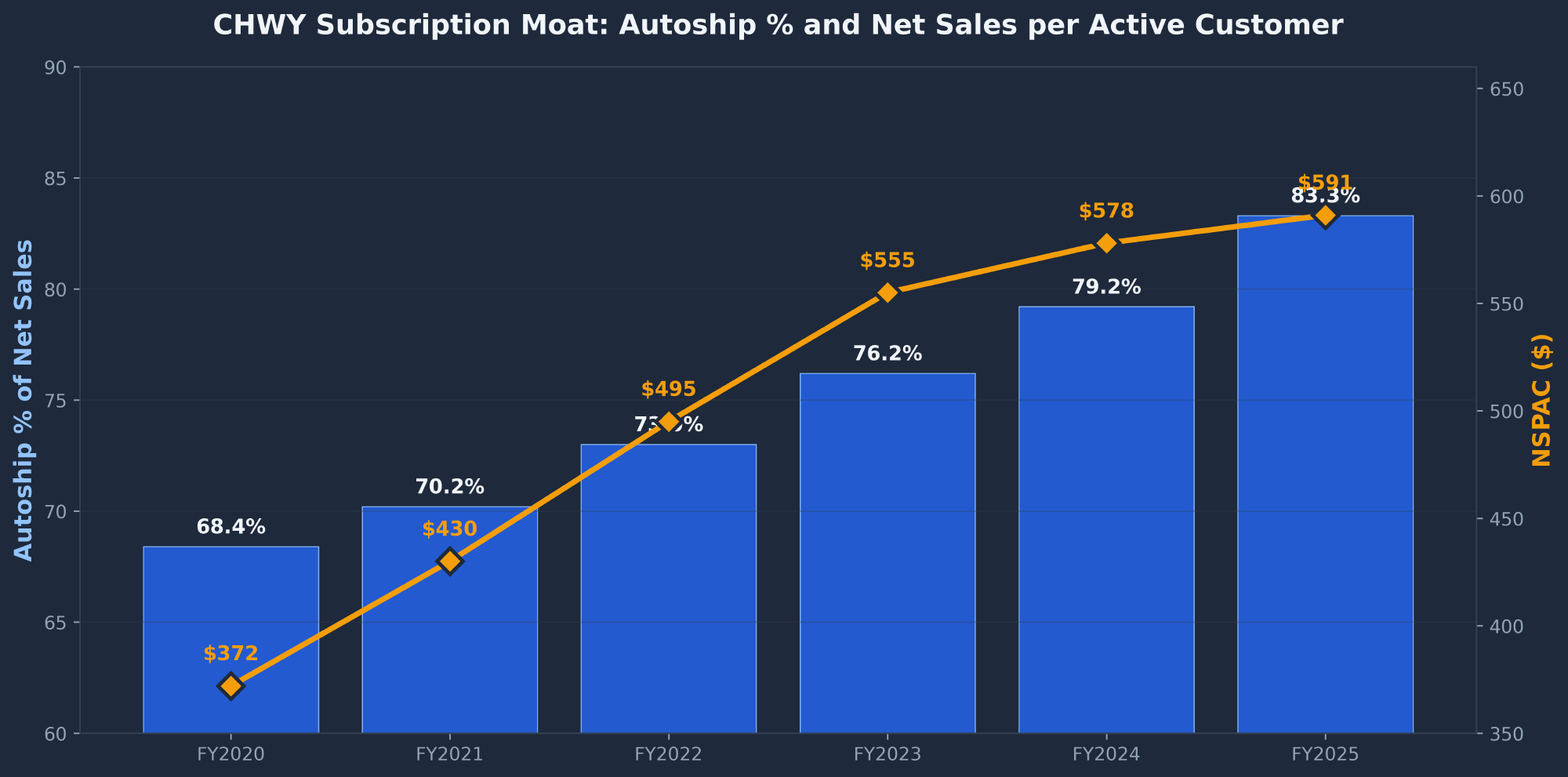

- Autoship at 83.3% of net sales is a real subscription moat. Net Sales Per Active Customer (NSPAC) compounded from $372 to $591 over five years even as gross customer count plateaued. This is consumer-staples-like recurring revenue inside a stock that the market is pricing like a struggling discretionary retailer.

- The valuation reset is real. Forward P/E 19x with consensus 38% EPS growth (PEG 0.50). P/S 0.76 below 1x revenue. Analyst consensus 1.52 Strong Buy with $41.24 target = +80% upside. Even haircut to a base case $35 target, the risk/reward is asymmetric: ~$3 of downside to firm support at $20 vs $12-18 of upside to mean reversion.

- The bear case is governance, not business. Stock-based compensation ($311M FY2025) exceeded GAAP net income ($223M). Three CFOs in three years. $950M of buybacks went directly to BC Partners' vehicle rather than open-market minority holders. CEO Sumit Singh's wife runs the highest-growth segment. These risks are real but already priced into a name trading at PEG 0.50.

| Report | Signal | Key Finding |

|---|---|---|

| Fundamentals | BULLISH | FCF compounding $9M → $562M, $0 debt, 83% Autoship, PEG 0.50 |

| SEC Filings | MIXED | Pristine balance sheet, but 3 CFOs in 3 yrs, SBC > GAAP NI, BC buyback prices flagged |

| Technical | MIXED | RSI 33.6, at 52W low, all MAs bearish — but capitulation volume 1.71x average |

| News & Events | BULLISH | 89 articles in 30 days. "Strategically right tactically painful" narrative. Zacks Strong Buy. |

| Insider/Institutional | BULLISH (Structural) | BC fully exited, Viking + Holocene smart money in, +3.09% Q/Q institutional accumulation |

| Sentiment | MIXED | Media bullish (Motley Fool, Seeking Alpha), Reddit cold, Twitter inconclusive |

| COMPOSITE | MODERATELY BULLISH | Four reports bullish or constructive; two mixed. No report bearish. |

CHWY Investment Thesis

Chewy at $22.97 is the rare case where a structural overhang has just been removed at the exact moment the stock hits a 52-week low. For 22 months, BC Partners (Argos Holdings) liquidated approximately 190M shares — 47% of the entire company — across nine secondary offerings, suppressing every rally and topping out the stock at $48.62 in late 2025. As of October 9, 2025, Argos Holdings owns zero CHWY shares. Smart money has begun replacing the displaced float: Viking Global (Ole Andreas Halvorsen, Tiger Cub) initiated a 5.70% position in December 2025, and Holocene Advisors (Brandon Haley, Citadel-pedigreed long/short) initiated 5.54% in May 2025. Net institutional transactions are +3.09% quarter-over-quarter despite the price weakness.

Underneath the supply/demand reset is a genuinely compounding business. Free cash flow grew from $9M (FY2021) to $562M (FY2025) — a 60x increase in four years on a debt-free balance sheet now sitting on $879M of cash and an undrawn $800M ABL facility. Gross margin expanded 310 basis points to 29.8%. Adjusted EBITDA margin went from 0.9% to 5.7%. Autoship penetration hit 83.3% of net sales ($10.5B), creating subscription-like revenue visibility that doesn't show up in consumer e-commerce comps. NSPAC compounded from $372 to $591 even as gross customer count plateaued during the post-COVID unwind.

The market is currently penalizing CHWY for three things: (1) the Modern Animal vet acquisition spend that dropped the stock 6.9% on announcement, (2) revenue growth decelerating from 24% to 6%, and (3) the optically bearish CEO 10b5-1 sale on May 5. All three are misjudged on time horizon. Vet expansion is the highest-margin extension of the PracticeHub platform that already serves ~50% of US vet clinics. Growth deceleration is the natural maturation of a 21M-customer subscription business that has shifted to compounding NSPAC. The CEO sale is mechanical 10b5-1 sell-to-diversify, not signal.

CHWY Fundamental Analysis

Chewy is the largest pure-play online pet retailer in the United States, founded in 2011, acquired by PetSmart (a BC Partners portfolio company) in 2017, and IPO'd in 2019. The company runs 17 fulfillment centers totaling 9.87M square feet across the US and Canada, partners with ~4,000 brands across ~190,000 SKUs, and claims the "#1 pet pharmacy in America" title. Fiscal year ends late January / early February. Market cap is $9.57B at $22.97, with enterprise value of $9.25B.

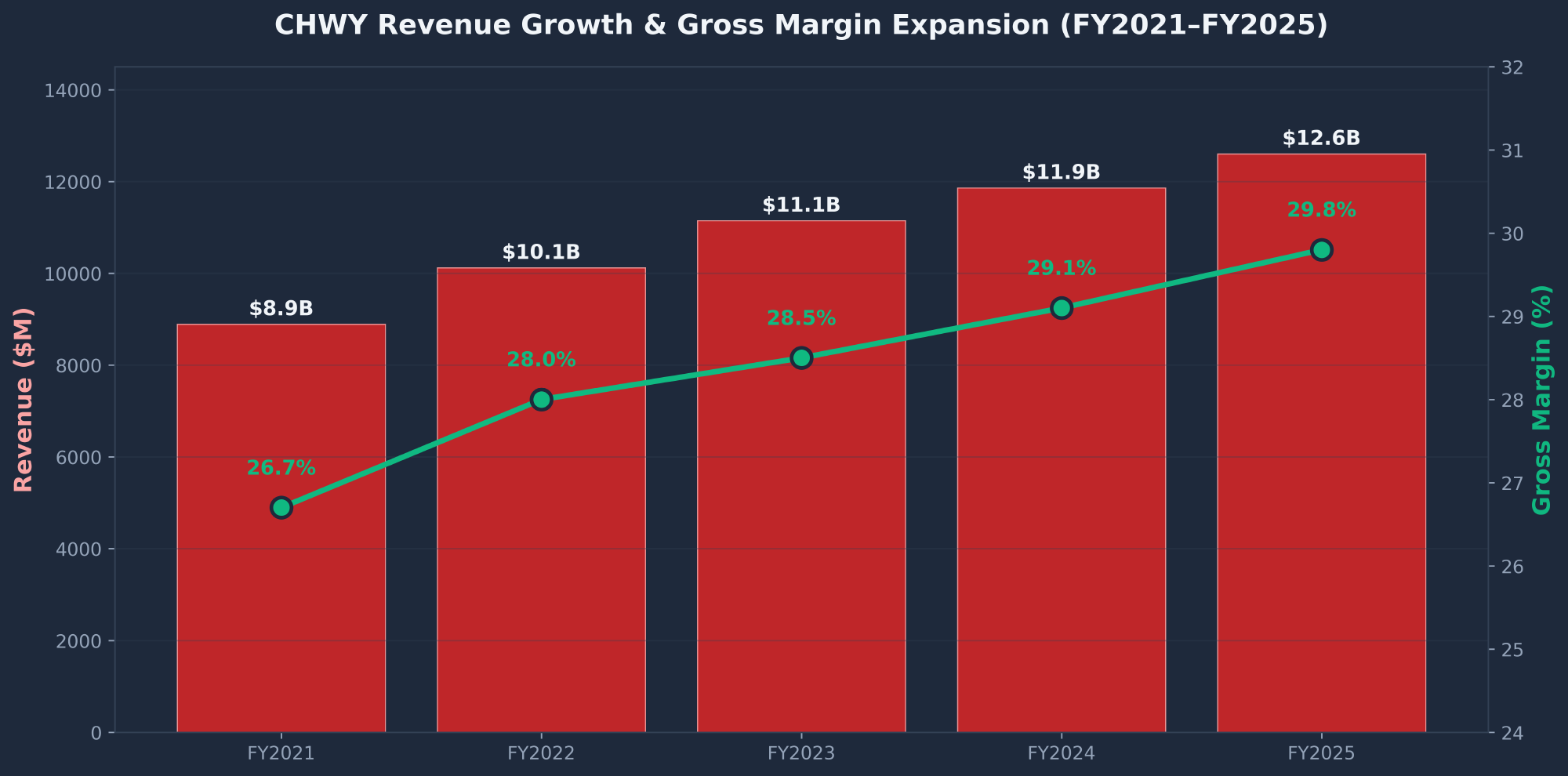

CHWY Revenue Growth and Margin Expansion

The headline number that bears love — revenue growth decelerating from 24% to 6% — obscures the more important story underneath. Gross margin expanded 310 basis points over four years (26.7% → 29.8%), and adjusted EBITDA margin expanded 480 basis points (0.9% → 5.7%). FY2024 was a 53-week year worth $227M, so the FY2025 6.2% reported growth was actually 8.3% on a comparable 52-week basis.

| Metric ($M) | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Revenue | 8,891 | 10,119 | 11,148 | 11,861 | 12,602 |

| Revenue YoY % | 24.4% | 13.6% | 10.2% | 6.4% | 6.2% |

| Gross Margin % | 26.7% | 28.0% | 28.5% | 29.1% | 29.8% |

| Adj. EBITDA Margin | 0.9% | 2.1% | 3.3% | 4.8% | 5.7% |

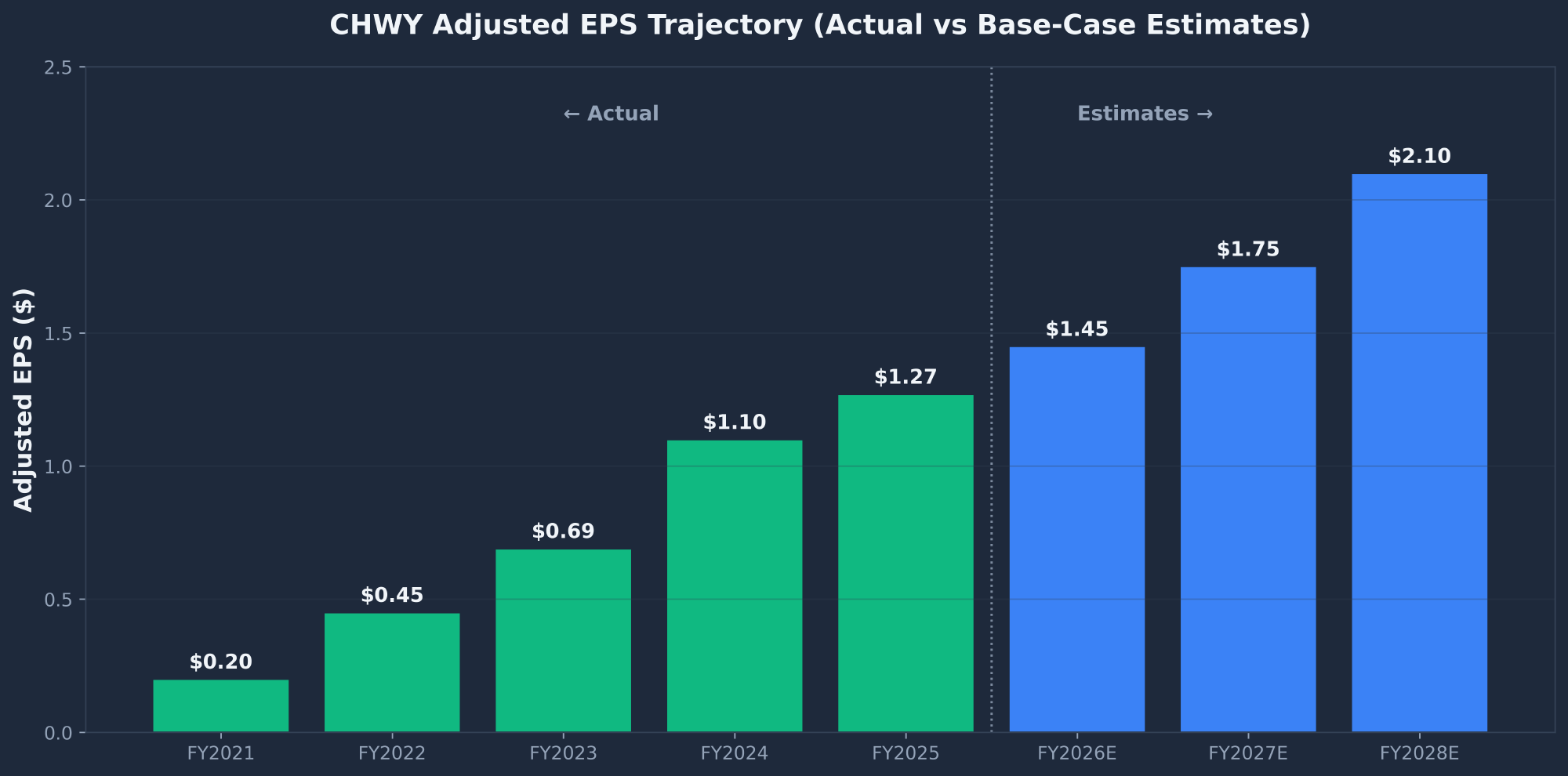

| Adj. EPS | $0.20 | $0.45 | $0.69 | $1.10 | $1.27 |

Chewy Free Cash Flow Compounding 60x in 4 Years

Free cash flow is where the Chewy story gets interesting. FCF grew from $9M (FY2021) → $110M → $343M → $453M → $562M (FY2025). That's a 62x increase in four years on a low-single-digit revenue growth base. Capital expenditures peaked at $230M in FY2022 and have declined to $129M in FY2025 even as the company opens vet clinics and pharmacy facilities — this is pure operating leverage, not a CapEx holiday. At $22.97, the market is paying ~17x FCF for a business that grew FCF 24% year-over-year and has a debt-free balance sheet.

The Autoship Subscription Moat

Autoship is the most underappreciated piece of the Chewy stock analysis. Autoship customer sales hit $10.50B in FY2025, equaling 83.3% of net sales — up from 68% in FY2020. This is the strongest indicator of customer stickiness. Subscription customers pre-commit, churn less, and grow Net Sales Per Active Customer (NSPAC) faster. NSPAC rose from $372 (FY2020) to $591 (FY2025) — that's 59% growth even while gross customer count plateaued during the post-COVID unwind. The economics resemble a consumer staples business with recurring revenue, not a discretionary retailer.

CHWY Pristine, Debt-Free Balance Sheet

| Balance Sheet Item | Value (Feb 1, 2026) |

|---|---|

| Cash + Marketable Securities | $879M |

| Total Traditional Debt | $0 |

| ABL Revolving Facility | $800M capacity, undrawn |

| Accordion Option | $250M available |

| Operating Lease PV | $557M (10.2-yr avg term) |

| Goodwill | $39M (Petabyte 2022) |

Zero traditional debt is unusual for a low-margin retailer. The current ratio of 0.88 looks weak in isolation but is funded by trade payables — Chewy collects from customers faster than it pays suppliers. The only goodwill on the books is $39M from the Petabyte acquisition in 2022. This is a genuinely-built business, not a roll-up.

CHWY Valuation Metrics and Forward P/E

| Metric | Value | Interpretation |

|---|---|---|

| P/E (TTM) | 43.92 | Elevated on GAAP — depressed by SBC and FY2024 tax base effect |

| Forward P/E | 19.04 | Reasonable given 38% expected EPS growth |

| PEG | 0.50 | Cheap on growth-adjusted basis |

| P/S | 0.76 | Below 1x revenue for a 30%-gross-margin retailer |

| P/FCF | 17.02 | Reasonable for compounding FCF stream |

| EV/Sales | 0.73 | Below 1x after net cash adjustment |

| ROIC | 21.92% | Strong capital efficiency |

Chewy Peer Comparison: CHWY vs AMZN, WMT and COST

CHWY trades at the lowest P/S of its comp group despite having the highest gross margin of any e-commerce comp and subscription-like Autoship characteristics that arguably warrant a Costco-style premium multiple.

| Ticker | P/S | P/E Fwd | EV/EBITDA | Profile |

|---|---|---|---|---|

| CHWY | 0.76 | 19.0 | 23.3 | Online pet retailer (subscription anchor) |

| WMT | 1.05 | 32.0 | ~17 | Mass retail leader |

| COST | 1.45 | 50.0 | ~30 | Subscription retailer |

| AMZN | 3.30 | 35.0 | ~17 | Direct e-commerce competitor |

| TSCO | 1.55 | 22.0 | ~16 | Pet/farm specialty retailer |

CHWY Technical Analysis

CHWY is in a confirmed downtrend with all three primary moving averages stacked bearishly. SMA 200 sits at ~$32.30, a 29% gap to current price — an extreme deviation typically seen at capitulation extremes. RSI (14) at 33.62 is near oversold and printed sub-30 intraday during the May 8 Modern Animal selloff. Relative volume is running 1.71x average on the decline, which is climactic-style action that often marks short-term lows when followed by lower-volume basing.

| Indicator | Value | Signal |

|---|---|---|

| Price vs SMA 20 | -11.02% | BEARISH (below) |

| Price vs SMA 50 | -10.83% | BEARISH (below) |

| Price vs SMA 200 | -28.94% | DEEPLY BELOW |

| RSI (14) | 33.62 | APPROACHING OVERSOLD |

| Beta | 1.49 | HIGH (49% more volatile than SPX) |

| ATR (14) | $1.21 | ~5% average daily range |

| Relative Volume | 1.71x | ELEVATED (capitulation-like) |

| 52W Position | +1.01% off low | NEAR 52W LOW |

CHWY Support, Resistance and Price Target Levels

The first technical reversal signal is a daily close above $25.81 (SMA 20). Above that, the next resistance is the SMA 200 at ~$32-33, followed by the BC Partners final exit price at $37.65 (now widely held above), the analyst consensus target at $41.24, and the 52-week high at $48.62. On the downside, the recent 52-week low at $22.74 is the immediate support, with $20 as the psychological/2024-BC-floor level, $17-18 as the 2024 base, and $14 as the absolute April 2024 low.

CHWY Technical Scenarios and Trade Setups

Bullish Case (40% probability)

Trigger: Daily close above $25.81 (SMA 20) on average or higher volume.

- $28.20 — 78.6% Fib (initial)

- $32.67 — 61.8% Fib + SMA 200

- $35.68 — 50% Fib (base case)

- $41.24 — analyst consensus

Bearish Case (35% probability)

Trigger: Break below $22.74 on volume, especially on a Q1 FY2026 miss or antitrust escalation.

- $20 — psychological + 2024 BC floor

- $17-18 — 2024 base support

- $14 — ultimate support (Apr 2024 low)

The remaining 25% probability is a range-bound chop between $22-28 awaiting the Q1 FY2026 earnings catalyst.

Chewy SEC Filings Deep Dive

I reviewed 40 Chewy filings (FY2021 through Q3 FY2025) on EDGAR. Five things stand out.

1. Stock-Based Compensation Dwarfs GAAP Earnings

SBC + payroll taxes were $311M in FY2025 vs $223M of GAAP net income. In FY2024, SBC ($332M) was nearly equal to NI ($393M, itself flattered by a $275M tax valuation allowance release). At 2.5% of revenue, Chewy's SBC ratio is roughly 5x the typical mature retailer (~0.5%). Total RSU + PRSU overhang is 22.8M unvested + 76.5M reserved = ~99M of potential dilution, or ~24% of shares outstanding. Buybacks have offset only ~32M shares. Adjusted EPS is essentially "EPS before paying employees."

2. BC Partners Used Chewy's Cash to Buy Themselves Out

Of the $1.2B in FY2024-FY2025 share repurchases, approximately $950M was direct purchases from BC Partners' vehicle Buddy Chester Sub LLC at progressively higher prices ($28.49 → $29.40 → $31.32 → $41.75). Only ~$210M was open-market repurchases benefiting minority holders. Chewy effectively funded its sponsor's exit instead of returning capital to remaining shareholders. The remaining $250M authorization is small relative to the float.

3. Three CFOs in Three Years

| Date | Event |

|---|---|

| Jul 2023 | Mario Marte (long-tenured CFO) resigns |

| Dec 2023 | David Reeder appointed CFO with $16.8M new-hire equity grant |

| May 2025 | Reeder departs after 15-month tenure; total comp $27.8M |

| Feb 2026 | Christopher Deppe (ex-Amazon, internal VP Finance since 2022) promoted to CFO |

CFO churn at this rate is a serious governance red flag — typically signals tension with the CEO or strategic/accounting disagreements. The Reeder $27.8M for 15 months of work is particularly jarring.

4. CEO's Wife Runs the Highest-Growth Segment

CEO Sumit Singh's wife, Aseemita Malhotra, is President of Healthcare at Chewy — the company's highest-growth vertical. Both Singh and Malhotra adopted 10b5-1 plans on January 16, 2026. Malhotra's plan authorizes 76,710 shares; Singh's plan authorizes up to 612,185 shares through January 2027. This is a related-party concentration that doesn't show up in most retail screens.

5. Management Credibility Scorecard

| Promise | Outcome | Verdict |

|---|---|---|

| Grow active customers continuously | Customers fell in FY2022 / FY2023 | MISSED |

| Sustained revenue growth + margin expansion | Growth slowed 14% → 6%, but margins did expand | MIXED |

| Launch Canada + international expansion | 3 years in, no revenue disclosure, $95M foreign NOL | BEHIND |

| Chewy Vet Care — 8 clinics FY2024 | 18 operational + 25 with leases by FY2025 | DELIVERED |

| Adj. EBITDA margin improvement | 0.9% → 5.7% over 4 years | DELIVERED |

| Free cash flow generation | $9M → $562M in 4 years | STRONGLY DELIVERED |

| Buyback execution | ~$950M to BC Partners vs ~$210M open market | QUESTIONABLE |

CHWY News and Catalysts

CHWY has received above-baseline media coverage this month — 89 articles in the last 30 days, 44 in the last 7. Sentiment breaks down as 38 neutral / 30 bullish / 21 bearish. The dominant narrative is "strategically right, tactically painful": analysts and writers across Motley Fool, Seeking Alpha, simplywall.st, and BNN Bloomberg argue the long-term moves are correct but the market is punishing the spend.

Recent Headlines

| Date | Source | Headline | Tone |

|---|---|---|---|

| May 8, 2026 | MarketBeat | CHWY Hits New 1-Year Low at $22.73 | Bearish |

| May 8, 2026 | Pet Food Processing | Chewy Expands Into Vet Services With Modern Animal Acquisition | Neutral |

| May 7, 2026 | The Motley Fool | Chewy Is Down 25% This Year — Investors Should Be Eager to Buy | Bullish |

| May 5, 2026 | GeekWire | Amazon VP Is Now Chewy CTO | Bullish |

| May 5, 2026 | Investing.com | CEO Sumit Singh Sells $2.24M In Stock (10b5-1) | Bearish |

| Apr 24, 2026 | Seeking Alpha | Chewy: Durable Demand And Consistent Earnings Growth | Bullish |

| Apr 17, 2026 | Yahoo Finance / Zacks | Zacks Upgrades CHWY to Strong Buy | Bullish |

| Apr 14, 2026 | MarketBeat | Tanking Stocks Announcing Buybacks (CHWY Included) | Bullish |

Upcoming Catalysts

| Date | Event | Bull / Bear Outcome |

|---|---|---|

| Late May / Early June 2026 | Q1 FY2026 Earnings (primary catalyst) | Customers 21M+, Autoship 84%+ / Customer decline, SBC outpaces FCF |

| Ongoing | Buyback execution at sub-$25 | $100M+ open market = conviction / Quiet quarter = none |

| Q1 FY2026 | SmartPak Equine first revenue ($175M Feb 2026 deal) | Accretive / Margin drag |

| Q2 FY2026 (~Sept 2026) | Modern Animal first integration disclosure | Unit economics positive / Open-ended spend |

| Ongoing | California antitrust developments | Resolves manageably / Material damages |

| March 2027 | FY2026 10-K with potential ads segment breakout | Sponsored ads formal segment / No disclosure |

CHWY Market Sentiment

The internet's read on CHWY at $22.97 is bifurcated: financial media is bullish, Reddit has gone cold, and Twitter is dominated by spam. This media/retail divergence often precedes inflection points — when retail rediscovers a name that media has been bullish on, multiple expansion can be sharp.

Reddit Activity

| Subreddit | Activity | Tone |

|---|---|---|

| r/wallstreetbets | LOW (cooling) | Last post Sept 2025 oversold thesis — buyers wiped out |

| r/stocks | VERY LOW | Indifferent |

| r/investing | NONE | Off the radar |

| r/ValueInvesting | LOW but recent | Polarized; bull OP, bear top comments |

Bull vs Bear Community Arguments

Bull (Financial Media)

- "Down 25% YTD — investors should be eager to buy" (Motley Fool)

- Consumer-staples-like demand profile (Seeking Alpha)

- 83% Autoship locks in loyal customers (r/WSB)

- Vet expansion to ~275 clinics by 2030 (Morgan Stanley)

- Zacks Strong Buy upgrade April 17

- Private-label margin push (Frisco, Vibeful, Get Real)

Bear (Reddit Value Crowd)

- "Stock down 26% in 10y, 77% in 5y" (r/ValueInvesting)

- "SBC of $307M+ eats free cash flow; only $60M real FCF"

- "No moat, 2% net income margin, dilution treadmill"

- "Vets hate Chewy" — vet clinic headwind

- Canada/EU 3 yrs in — no revenue disclosure

- P/FCF doesn't justify 80% upside scenarios

CHWY Insider and Institutional Activity

The single most important data point in the entire CHWY stock analysis: Argos Holdings = 0 shares as of October 9, 2025. After 22 months and nine secondary offerings totaling ~$4.15B, the pre-IPO controlling sponsor has fully exited. Combined with net institutional accumulation of +3.09% Q/Q despite the price drop, this is the most constructive structural setup CHWY has had since IPO.

BC Partners (Argos Holdings) Exit Timeline

| Date | Shares (M) | Price | Value |

|---|---|---|---|

| Jan 9, 2024 | 12.32 | $20.29 | -$250M |

| Jun 26, 2024 | 22.88 | $28.87 | -$660M |

| Sep 23, 2024 | 26.87 | $29.40 | -$790M |

| Dec 13, 2024 | 19.83 | $31.32 | -$621M |

| Jan 6, 2025 | 7.00 | $35.77 | -$250M |

| Jun 25, 2025 | 29.94 | $41.75 | -$1,250M |

| Oct 9, 2025 | 13.28 | $37.65 | -$500M (FULLY EXITED) |

Smart Money Entries

(Halvorsen, Tiger Cub)

~$310M position Dec 2025

(Brandon Haley, Citadel-bred)

Initiated May 2025

Q/Q accumulation despite drawdown

Insider Activity (5-Year Summary)

| Metric | Value |

|---|---|

| Total Insider Buys (5y) | 5 trades / +422K shares / +$12.3M |

| Total Insider Sells (5y) | 124 trades / -141M shares / -$4.66B |

| Buy : Sell Ratio | $1 buys per $378 sells |

| BC Partners share of sales | ~$4.15B (89% of all sales) |

| Only insider buyer in 5 years | Director James A. Star (5 buys, 2021-2023) |

| Most recent insider sale | CEO Singh, May 4, 2026 ($2.24M, 10b5-1) |

CHWY Risk Factors

Below are the material risks to the CHWY stock analysis thesis, ranked by probability and impact.

| Risk | Probability | Impact | Mitigation |

|---|---|---|---|

| Active customer count plateaus or declines again | HIGH | HIGH | Stop at $20 if customers < 21M in Q1 FY2026 |

| SBC continues to exceed GAAP NI — dilution treadmill | HIGH | MEDIUM | Already priced in — PEG 0.50 reflects this |

| New CFO Deppe has another short tenure | MEDIUM | HIGH | Sentiment-killer if it happens; trim immediately |

| Canada/international expansion definitively fails | MEDIUM | MEDIUM | Limited downside — only $95M foreign NOL |

| Amazon Pharmacy + Walmart pet sub erode share | MEDIUM | MEDIUM | Watch Pet Health YoY trend |

| California antitrust case escalates with damages | LOW | MEDIUM | Watch major outlet coverage for escalation |

| Vendor concentration (top 3 = 39% of sales) | LOW | MEDIUM | Mature relationships; manageable |

| Tariffs (Mexico/China) impact private-label margin | MEDIUM | MEDIUM | Diversify suppliers; pass through pricing |

CHWY Conclusion and Price Targets

Adjusted EPS Trajectory

3-Scenario Earnings Model

| Scenario | FY2026E Rev | FY2027E Rev | FY2027 EBITDA Margin | FY2027 Adj EPS |

|---|---|---|---|---|

| Bear | $13.0B (+3%) | $13.3B (+2%) | 5.5% | $1.15 |

| Base | $13.6B (+8%) | $14.7B (+8%) | 7.0% | $1.75 |

| Bull | $13.9B (+10%) | $15.5B (+12%) | 8.0% | $2.30 |

Valuation Analysis

| Method | Inputs | Implied Price |

|---|---|---|

| Base P/E | FY2027 EPS $1.75 × 20x | $35.00 |

| Base EV/EBITDA | FY2027 EBITDA $1.03B × 15x + $850M net cash | $39.00 |

| P/FCF | FY2027 FCF $720M × 20x P/FCF | $34.00 |

| DCF (10% disc, 3% term) | 5-yr FCF forecast w/ base case | $37.00 |

| Bull P/E | FY2027 EPS $2.30 × 22x | $50.00 |

| Bear P/E | FY2027 EPS $1.15 × 14x | $16.00 |

| Analyst Consensus | 1.52 Strong Buy | $41.24 |

Bull and Bear Targets

Bull Case ($40-50)

- Gross margin expands 30% → 32%, EBITDA 6% → 8%

- FY2027 adj. EPS reaches ~$2.00-2.30

- Multiple re-rates as Autoship subscription moat is recognized

- Sponsored ads segment formally broken out

- Smart money (Viking, Holocene) accumulation continues

- 20-22x P/E = $40-50

Bear Case ($15-18)

- Growth decelerates further to 3-4%

- Margin expansion stalls as private-label saturates

- SBC dilution accelerates relative to operating leverage

- Amazon Pharmacy / Walmart erode high-growth segments

- FY2027 adj. EPS flat at $1.15-1.30

- 12-14x P/E = $15-18 (forward multiple to retail trough)

Action Plan

| Parameter | Action |

|---|---|

| Position size | 1.5%-3% of portfolio (Beta 1.49 = high volatility) |

| Entry strategy | 50% at $22.97, 25% on $21 retest, 25% on confirmed reclaim of SMA 20 ($25.81) |

| Hard stop | $20 — below this, technical damage extends to $17 quickly |

| Trim level 1 | $32-33 (SMA 200) — take 25% off |

| Trim level 2 | $41 (analyst consensus) — take another 25% off |

| Hold core through | $50+ retest of ATH zone |

| Time horizon | 12-18 months for full target realization |

For investors who prefer options to outright stock, CHWY's high beta (1.49) and current oversold setup make it a candidate for a cash-secured put strategy at the $20 or $22.50 strike — either get assigned at favorable prices or collect premium. With Autoship-driven recurring revenue and a debt-free balance sheet, CHWY also fits the profile of stocks suitable for the wheel strategy at the right entry point. Review the criteria for selecting the best stocks for the wheel strategy, and if you already own CHWY shares above the current price, see how to lower your stock basis using options. For more research like this CHWY stock analysis, browse all of my stock analysis reports or visit the Options Cafe homepage.

Frequently Asked Questions

Is CHWY a good stock to buy in 2026?

At $22.97, CHWY rates a Buy with a $35 price target and 12-18 month time horizon. The thesis is structural rather than earnings-driven. BC Partners has just completed a $4.15B exit after nine secondary offerings over 22 months, removing the largest known share-supply overhang in the company's history. Smart money — Viking Global (5.70%) and Holocene Advisors (5.54%) — has begun replacing the freed-up float. Underneath the supply/demand reset is a debt-free FCF compounder ($562M FY2025 FCF on $0 traditional debt) with an 83.3% Autoship subscription moat. Forward P/E 19x with PEG 0.50 makes the risk/reward asymmetric.

What is the CHWY price target for 2026?

My base case is $35 by mid-2027 (+52% from $22.97), supported by a $1.75 FY2027 adjusted EPS estimate × 20x multiple. The bull case is $40-50 if margin expansion continues and sponsored ads is formally broken out as a segment. The bear case is $15-18 if growth decelerates below 5% and SBC dilution accelerates. Analyst consensus is $41.24 with a 1.52 Strong Buy rating — my $35 target builds in a haircut for governance and SBC dilution risk.

Should I buy or sell CHWY stock?

I rate CHWY a Buy at $22.97, but with strict position sizing (1.5%-3% of portfolio) and a hard stop at $20. The setup is asymmetric — approximately $3 of downside to firm support versus $12-18 of upside to mean reversion targets. The right approach is scaling in: 50% at market, 25% on a $21 retest, and 25% on a confirmed reclaim of the SMA 20 at $25.81. Trim 25% at $32-33 (SMA 200) and another 25% at $41 (analyst consensus). Sell only if customers fall below 21M in Q1 FY2026 or if the stock breaks below $20 on volume.

What is the CHWY stock forecast for 2026 and beyond?

For FY2026 my base case has revenue at $13.6B (+8%), adjusted EBITDA margin at 6.3%, and adjusted EPS of $1.45. For FY2027 base case revenue is $14.7B (+8%) with EBITDA margin 7.0% and adjusted EPS $1.75. For FY2028 base case revenue is $15.8B (+7%) with EBITDA margin 7.8% and adjusted EPS $2.10. The key drivers are vet vertical optionality, SmartPak Equine integration, NSPAC compounding, and sponsored ads margin lift. The biggest swing factor is whether sponsored ads gets formally broken out as a segment — that disclosure alone could re-rate the multiple.

Why has Chewy stock dropped so much?

CHWY is down 30% year-to-date and 67% over five years for three reasons. First, BC Partners' 22-month $4.15B distribution suppressed every rally since 2024 by adding supply on top of any demand. Second, revenue growth decelerated from 24% to 6% as the company matured past its COVID pull-forward customer base. Third, the Modern Animal vet acquisition (April 2026) plus an optically bearish CEO 10b5-1 sale on May 5 drove the final leg down to the $22.74 52-week low. The current setup is constructive because the first reason — BC distribution overhang — is now permanently resolved, and the other two are misjudged on time horizon.

Sources: SEC EDGAR filings, Finviz, Polygon.io, Google News, Reddit, Twitter/X. Report compiled May 10, 2026.