DKNG (DraftKings) Stock Analysis: Buy at $22.63 | $35 Target

Table of Contents

Executive Summary

This DKNG stock analysis (DraftKings Inc.) covers fundamentals, technicals, SEC filings, market sentiment, insider activity, and our DKNG stock forecast for 2026 as of April 2026. Here is the bottom line:

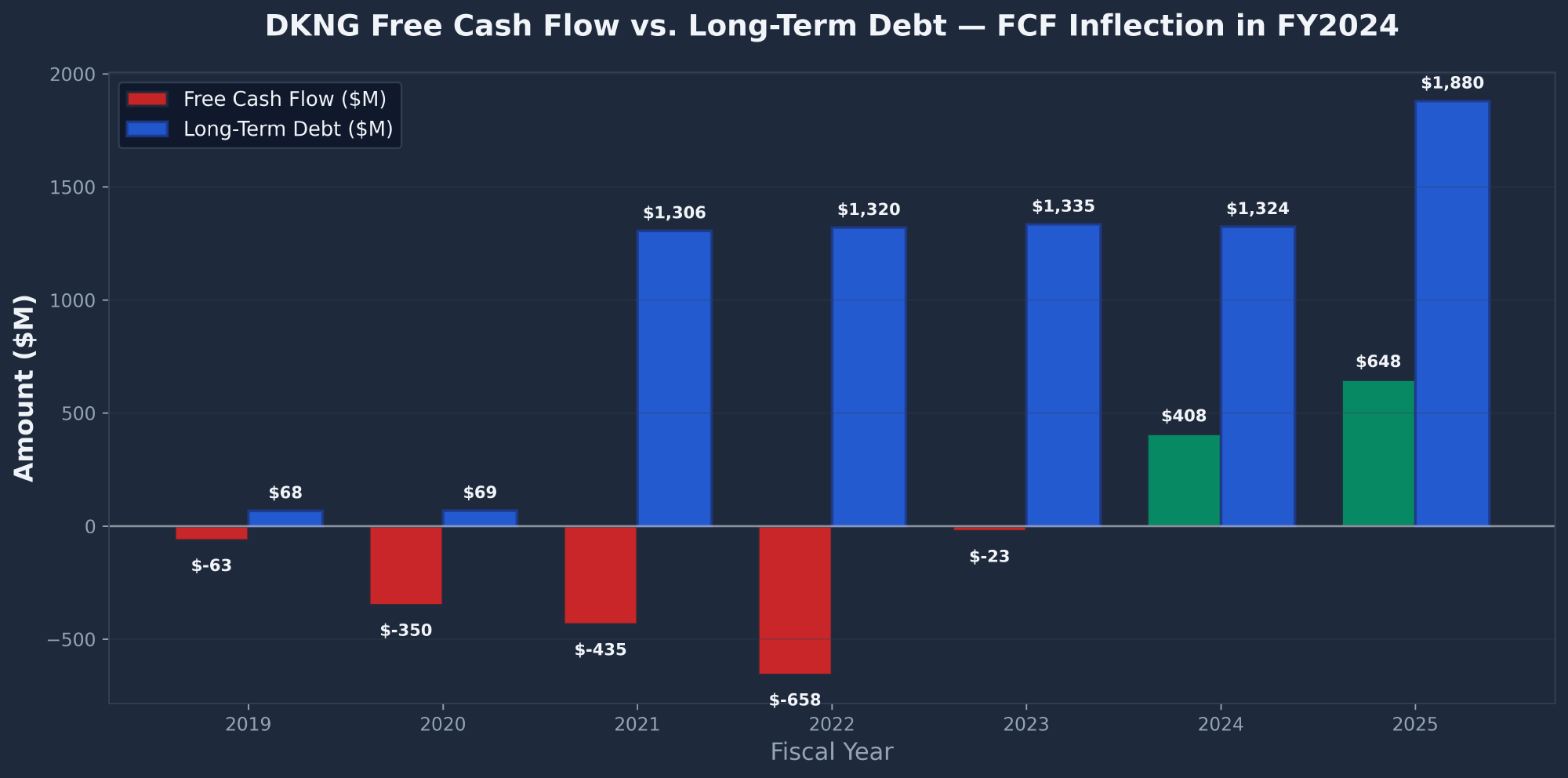

- BUY at $22.63 with a 12-18 month target of $35.00 (+54.7% upside). DraftKings has just delivered the cleanest profitability inflection in online gaming history — first-ever GAAP profit, Adjusted EBITDA +242% YoY, and free cash flow of $648M — yet the stock has crashed 58% from its February 2025 all-time high of $53.61.

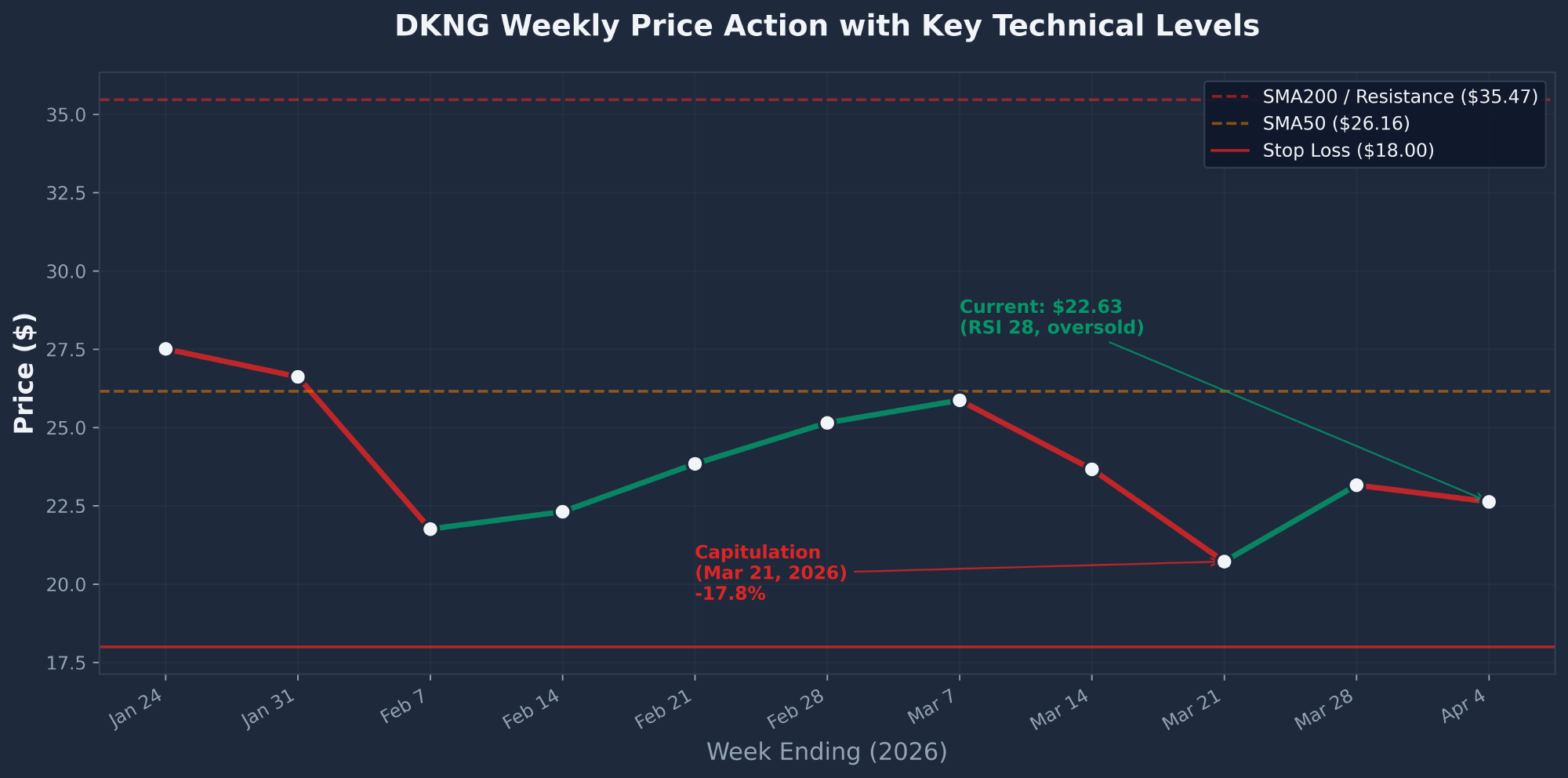

- Technically oversold at multi-year support. RSI sits at 28, price is 36% below its SMA200, and the March 28 capitulation reversal candle (+11.3%) suggests buyers stepped in at the $20.46 low. The $22.63 current price has a defined stop at $18.00 — the 2.67:1 risk/reward is compelling.

- Director Harry Sloan bought $2.2M at $21.85 in February 2026 — his second open-market buy in three months. That is the rare insider signal — a board member doubling down below his first purchase price. It is the only unambiguously bullish insider tell in an otherwise founder-heavy sell wall.

- Prediction markets (Kalshi, Polymarket, Robinhood) are the central bear narrative. Kalshi did $871M in Super Bowl volume and just won a federal court ruling on April 6. Goldman Sachs cut DKNG's price target from $54 to $31 on February 17. But at 1.85x forward sales, this narrative appears priced in.

- CEO Jason Robins filed a $54M proposed Form 144 sale on March 4 at $25.43 — into weakness. This is the largest single intended transaction on record and the key counterpoint to the bull thesis. Combined founder cashouts total $585M with zero buys. Position sizing matters.

| Report | Signal | Key Finding | Weight |

|---|---|---|---|

| Fundamentals | BULLISH | First GAAP profit, FCF +$648M, Adj EBITDA tripled to $620M, revenue +27% | 25% |

| SEC Filings | BULLISH | Net debt $231M, healthy balance sheet. New $576M Term B loan manageable. | 15% |

| Technical | BULLISH | RSI 28 oversold, 36% below SMA200, capitulation candle Mar 28 (+11.3%) | 20% |

| News & Events | BEARISH | Goldman PT cut $54→$31, Kalshi Super Bowl $871M, state tax hikes | 15% |

| Insider/Institutional | MIXED | Founders selling $585M cumulative, but Sloan bought $2.2M at lows | 15% |

| Sentiment | BEARISH | Reddit apathy at peak season, Twitter score 25/100 — contrarian indicator | 10% |

| COMPOSITE | MODERATELY BULLISH | 3 bullish, 1 mixed, 2 bearish across 6 reports. Washed-out sentiment is a feature, not a bug. | 100% |

Investment Thesis

DraftKings is a classic contrarian setup: a company hitting its fundamental inflection while the stock trades near multi-year technical support, RSI at an extreme oversold reading, and a director buying $2.2M on the open market at essentially today's price. The divergence between operating performance and share price is the investment opportunity.

In FY2025, DraftKings delivered its first-ever GAAP profitable year. Revenue grew 27% to $6.06B. Adjusted EBITDA tripled to $620M from $181M (+242% YoY). Free cash flow surged to $648M from $408M. Net income crossed into positive territory at $3.7M versus a $507M loss the prior year. This is the cleanest profitability inflection in the online gaming universe — the business model has finally hit operating leverage at scale.

Yet the stock is down 58% from its February 2025 all-time high of $53.61 to $22.63, including a 35% year-to-date decline in 2026 alone. The correction is driven by three fears: (1) prediction market disruption from Kalshi, Polymarket, and Robinhood; (2) state tax hikes (Illinois, NJ, NC); and (3) a soft FY2026 revenue guide that triggered a 12-15% earnings-day drop on February 12.

The thesis rests on four pillars. First, the profitability inflection is real and not a one-quarter fluke — FY2025 Q4 revenue grew 43% YoY and delivered positive EPS of $0.25. Second, prediction market fears appear fully priced in after Goldman's $54→$31 price target cut and the 35% YTD decline — when every bearish catalyst has landed and the stock has stopped going down, the setup shifts. Third, the technical capitulation is a classic setup — RSI 28 combined with a 36% deviation below SMA200 and a reversal candle on March 28 is the kind of washout that precedes meaningful bounces. Fourth, insider buying at these lows is rare — Director Sloan has bought twice in three months and is now underwater on his November buy at $30.30, which makes his February buy at $21.85 a real conviction signal.

The key risk is that prediction markets truly disintermediate traditional sportsbooks, compressing DKNG's vig (margin per bet) and pressuring the Adjusted EBITDA ramp. The CEO's proposed $54M sale at $25.43 while the stock is 35% down YTD adds tension — founders do not typically sell into weakness unless they see more weakness ahead. Position sizing at 3-5% with a hard $18 stop is essential.

Fundamental Analysis

Company Overview

DraftKings Inc. (NASDAQ: DKNG) is a Boston-based digital entertainment and gaming platform. Founded in 2012 and taken public in April 2020 via a SPAC merger with Diamond Eagle Acquisition Corp, DraftKings operates five primary business lines: online sportsbook (in 20+ U.S. states plus Ontario), online casino/iGaming, daily fantasy sports (the original product), a newly launched prediction markets platform (CFTC-approved, December 2025), and media/gaming content.

The company is led by co-founder Jason Robins as CEO, alongside co-founders Matt Kalish and Paul Liberman. It trades on the NASDAQ under ticker DKNG with CIK 0001883685 and SIC Code 7990 (Services — Miscellaneous Amusement & Recreation).

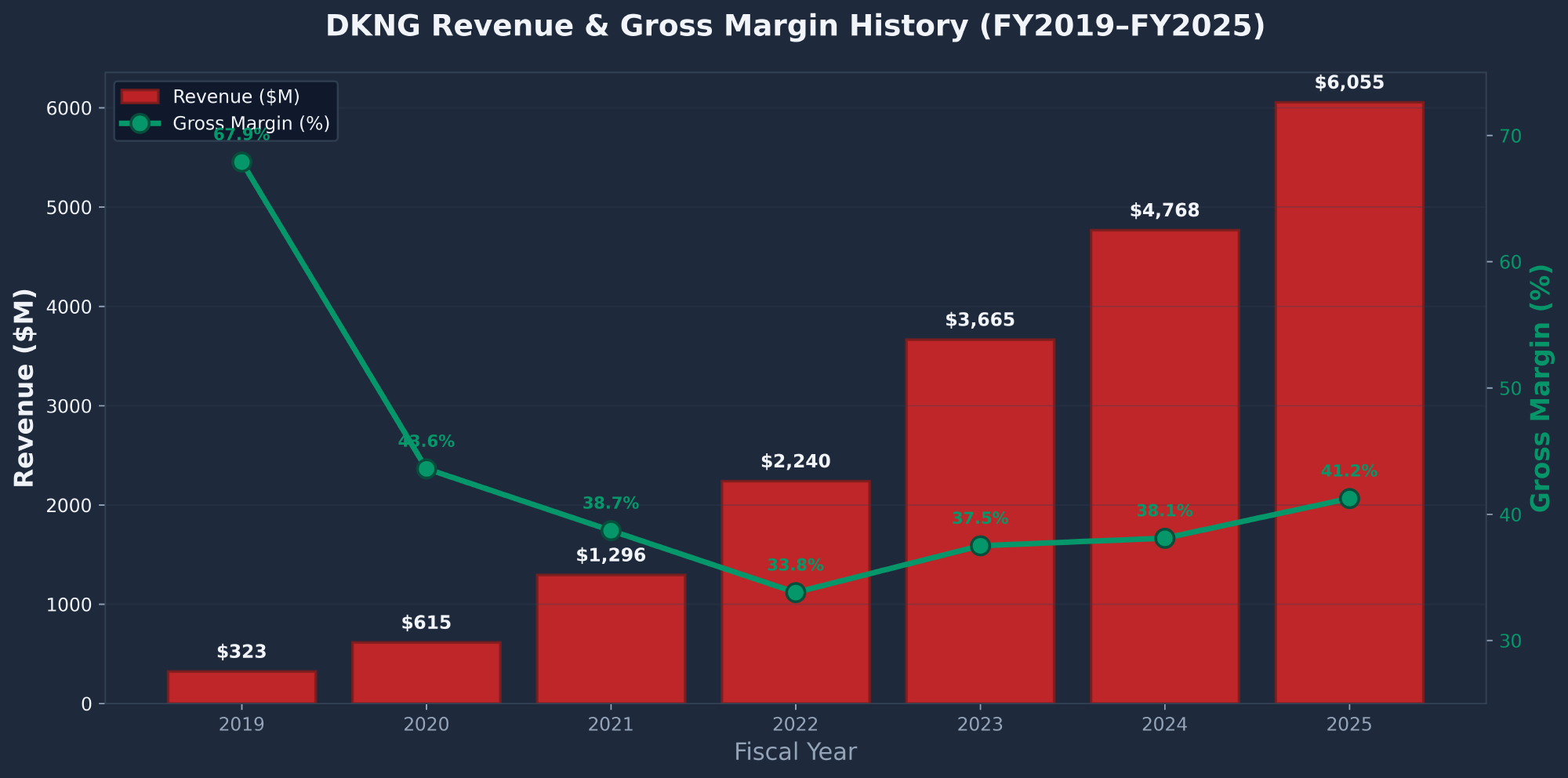

Revenue & Gross Margin History

Revenue has grown from $323M in 2019 to $6.06B in 2025 — a 62.6% compound annual growth rate. Gross margins bottomed at 33.8% in FY2022 during heavy state-expansion spending and have since recovered to 41.25% in FY2025 as the mix shifted toward more mature state operations.

| Metric ($M) | FY2019 | FY2020 | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|---|---|

| Revenue | 323 | 615 | 1,296 | 2,240 | 3,665 | 4,768 | 6,055 |

| Net Income | (143) | (1,232) | (1,523) | (1,378) | (802) | (507) | +4 |

| EBITDA | (133) | (766) | (1,440) | (1,343) | (550) | (231) | +273 |

| Operating Cash Flow | (47) | (338) | (420) | (626) | (2) | +418 | +663 |

| Free Cash Flow | (63) | (350) | (435) | (658) | (23) | +408 | +648 |

| Gross Margin | 67.9% | 43.6% | 38.7% | 33.8% | 37.5% | 38.1% | 41.25% |

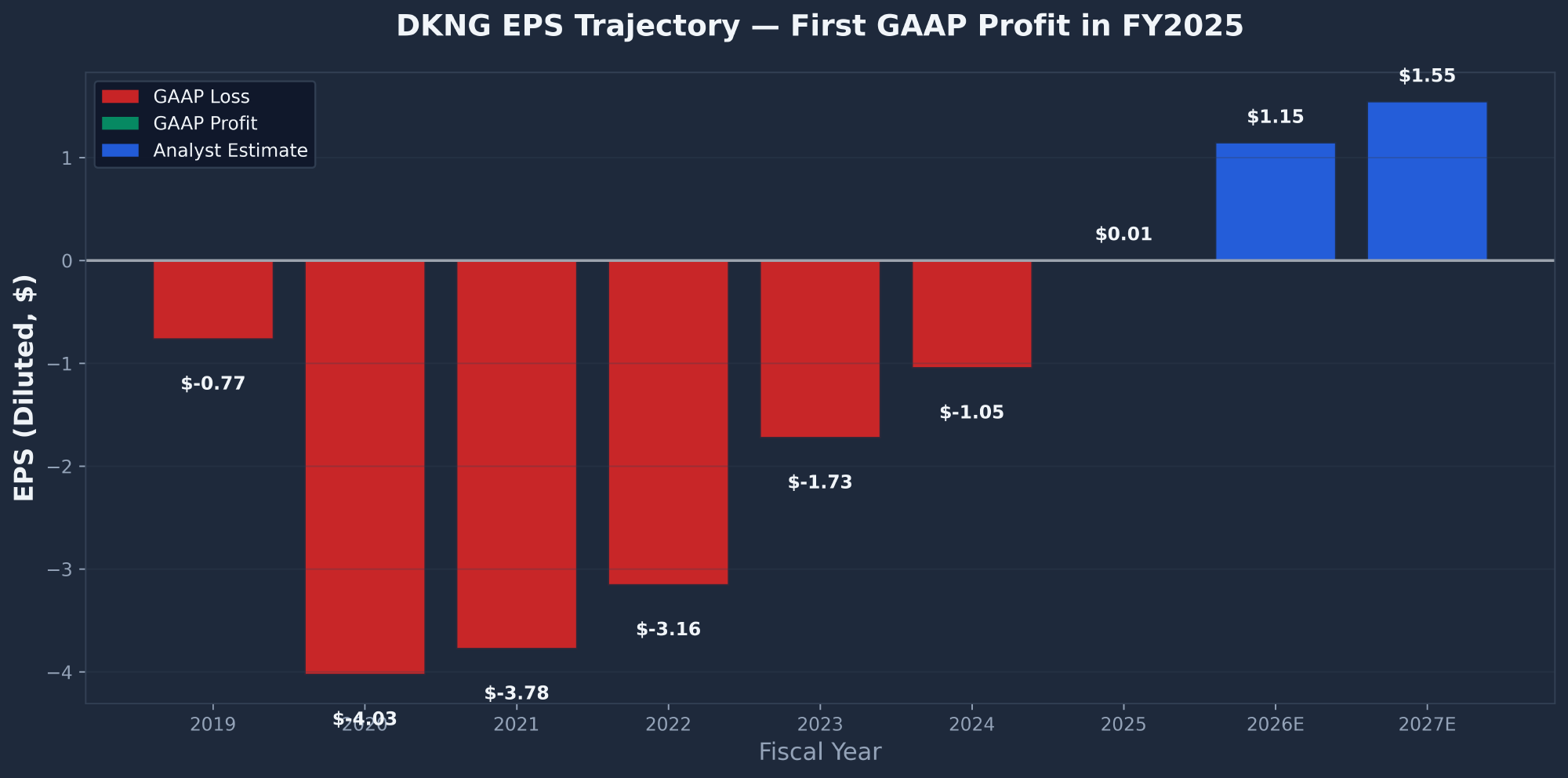

EPS Trajectory: The Profitability Inflection

DraftKings' EPS has crossed into positive territory for the first time in company history. FY2025 basic EPS came in at $0.01 versus -$1.05 in FY2024 — a quiet but structurally important flip. Analyst consensus calls for ~$1.15 in FY2026 and ~$1.55 in FY2027, implying a forward P/E of roughly 19.9x on current levels.

Quarterly Trajectory: Profitability Is Lumpy

| Quarter | EPS | Revenue ($M) | Notes |

|---|---|---|---|

| Q1 2025 | -$0.07 | $1,408 | Small loss |

| Q2 2025 | +$0.30 | $1,513 | First profit quarter |

| Q3 2025 | -$0.52 | $1,144 | Reverted to loss — favorite-heavy NFL weekends hurt hold % |

| Q4 2025 | +$0.25 | $1,989 (+43%) | Blowout quarter on revenue, soft FY2026 guide |

The lumpiness matters. Q3 2025's reversion to a loss was driven by sport outcomes (favorite-heavy weekends compress hold percentage) — a structural feature of the business that will repeat. Bulls need to model EPS quarterly, not just annually.

Valuation Snapshot

| Metric | Value | Metric | Value |

|---|---|---|---|

| Market Cap | $19.90B | Enterprise Value | $20.65B |

| P/S (TTM) | 3.29x | Forward P/S | 1.85x |

| EV/EBITDA | 77.63x | P/FCF | 30.73x |

| Forward P/E | 19.87x | P/B | 17.60x |

| Debt/Equity | 2.99x | Analyst Target | $35.32 |

Balance Sheet & Leverage

Despite the tension, net debt is just $231M ($1.88B debt minus $1.60B total cash). Net debt to Adjusted EBITDA of ~0.4x is healthy. The balance sheet has capacity — the question is whether management deploys it toward buybacks at better prices or the prediction market defense (Railbird acquisition at $250M, Polymarket clearinghouse partnership).

Analyst Consensus

The Wall Street consensus is a BUY rating of 1.54 with a mean price target of $35.32 — implying roughly 57% upside. The range of analyst actions has been dramatic over the past three months:

| Firm | Action | Date |

|---|---|---|

| Goldman Sachs | Price target $54 → $31 (biggest cut) | Feb 17, 2026 |

| Needham | Price target $52 → $35 | Feb 17, 2026 |

| Bernstein | Price target $41 → $32 | Feb 6, 2026 |

| Argus | Downgraded Buy → Hold | Mar 17, 2026 |

| Morgan Stanley | Price target $50 → $53 | Jan 16, 2026 |

| Wells Fargo | Upgraded Equal Weight → Overweight at $49 | Jan 15, 2026 |

| Berenberg | Upgraded Hold → Buy at $43 | Oct 2025 |

Peer Comparison

DKNG trades in line with online gaming peers on a P/S basis but at a premium on EV/EBITDA given its freshly positive EBITDA. Relevant peers include Flutter Entertainment (FLUT / FanDuel), MGM Resorts (MGM), Wynn Resorts (WYNN), Las Vegas Sands (LVS), Boyd Gaming (BYD), Caesars Entertainment (CZR), Penn Entertainment (PENN), Rush Street Interactive (RSI), and Evolution AB (EVVTY). Reddit value investors consistently cite Evolution AB's 12x forward P/E as a "better and actually profitable" alternative.

DKNG vs. FanDuel (Flutter Entertainment): Flutter trades at roughly 2.4x forward sales versus DKNG's 1.85x — a 30% discount. Flutter is profitable, global, and leads DKNG in most states on sportsbook handle, but DraftKings closed the gap in February 2026 per industry reports. The base-case $35 DKNG price target assumes this discount closes as the profitability inflection gets digested by the market.

Technical Analysis

DKNG is in a deep downtrend but showing a classic oversold reversal setup. The stock crashed 58% from the February 2025 ATH of $53.61, suffered two separate weekly capitulations (Feb 7, 2026 at -18.7% and Mar 21 at -17.8%), and now sits at RSI 28 — technically oversold. Price is 36% below its SMA200, an extreme deviation that rarely persists.

Moving Averages & Oscillators

| Indicator | Value | Price vs Indicator | Signal |

|---|---|---|---|

| SMA 10 | $23.98 | -5.6% | Just below — testing |

| EMA 10 | $23.41 | -3.3% | Resistance overhead |

| SMA 50 | $26.16 | -13.5% | Bearish medium-term |

| SMA 200 | $35.47 | -36.2% | Extremely extended (contrarian bullish) |

| RSI (14) | 28.12 | Oversold zone | BUY SIGNAL (oversold reversal) |

| MACD | -0.92 | Below zero | Bearish but stabilizing |

| MACD Histogram | -0.25 | Narrowing | Downside momentum fading |

Weekly Price Action

The weekly chart tells the story of the 2026 drawdown. After closing at $27.51 on January 24, DKNG crashed to $21.76 on February 7 (-18.7%) on the FY2026 guidance miss. A two-week relief rally carried the stock to $25.87 on March 7 before a second capitulation to $20.72 on March 21 (-17.8%) on the Kalshi Super Bowl volume shock. The March 28 reversal candle (+11.3%) printed a classic capitulation bottom pattern.

Support & Resistance

| Level Type | Price | Significance |

|---|---|---|

| Major Resistance (SMA200) | $35.47 | Long-term trend line — reclaim confirms trend change |

| Resistance (prior swing) | $30.00 | Psychological, Nov 2025 insider buy level |

| Resistance (SMA50) | $26.16 | Near-term overhead supply |

| Resistance (SMA10/EMA10) | $23.41–$23.98 | Current battle zone |

| CURRENT PRICE | $22.63 | Between support and first resistance |

| Support (recent low) | $20.46 | 52-week low set March 21, 2026 |

| Support (Oct 2023 swing) | ~$20.00 | Key multi-year support |

| Stop Loss Level | $18.00 | Below = long-term trend break |

SEC Filings Deep Dive

The DraftKings FY2025 10-K was filed in late February 2026. The company is domiciled in Boston with fiscal year ending December 31. SIC Code 7990 (Services — Miscellaneous Amusement & Recreation). CIK: 0001883685.

Capital Structure (From 10-K)

| Instrument | Amount | Notes |

|---|---|---|

| Convertible Notes | $1,259.1M | Dilutive conversion risk |

| Term B Loan (NEW in FY25) | $576.5M | Floating rate, drawn in FY25 |

| Total Debt | $1,835.6M | — |

| Total Cash (all) | $1,604.6M | $1,127.5M unrestricted + $7.6M restricted + $469.4M user-reserved |

| Net Debt | ~$231.0M | Very manageable given $620M Adj EBITDA |

| Net Debt / Adj EBITDA | ~0.4x | Healthy leverage ratio |

| Diluted Shares Outstanding | 495.9M | +2.9% YoY dilution from SBC |

Key Accounting Policies

- Revenue Recognition: Gaming revenue net of payouts, promotional credits, and jackpots.

- Liabilities to Users: $935.0M held as customer balances — matched with User-Reserved Cash of $469.4M on the asset side.

- Stock-Based Compensation: $339.3M in FY2025 (5.6% of revenue). Meaningful non-cash dilution that offsets reported FCF quality.

- Internally Developed Software: $131.2M capitalized in FY25, amortized over 3 years.

- Goodwill: $1,597.6M on the balance sheet — tested annually for impairment.

- Warrant Remeasurement: $4.7M gain in FY25 from SPAC-era warrant mark-to-market.

Management Credibility Scorecard

| Item | Grade | Notes |

|---|---|---|

| Delivering on profitability path | A | Hit first GAAP profit year on schedule |

| FY2026 guidance quality | D | Disappointed enough to trigger 15% drop and major PT cuts |

| Capital allocation (buybacks at elevated prices) | C | $829M spent on buybacks — not all at cheap prices |

| Strategic response to prediction markets | B+ | Launched own platform, acquired Railbird, CFTC advisory seat |

| Insider selling during downtrend | F | CEO filed $54M Form 144 at $25.43 — into the decline |

News & Catalysts

The news cycle over the past 30 days has been structurally negative, with roughly 45% bearish, 35% bullish, and 20% neutral sentiment across ~150+ articles. Five dominant themes shaped price action:

Theme 1: Prediction Markets (The Loudest Narrative)

| Date | Event | Impact |

|---|---|---|

| Oct 2025 | DKNG partnered with Polymarket as clearinghouse; agreed to pay $250M for Railbird acquisition | Strategic defense |

| Dec 19, 2025 | DKNG launched own prediction markets app in 38 states, CFTC-approved | Bullish — competitive move |

| Feb 2026 Super Bowl | Kalshi hit $871–900M Super Bowl volume; total prediction market SB volume $1.63B | Brutal — direct market share capture |

| Feb 2026 | NFL banned prediction market commercials from Super Bowl | "Treating Kalshi/Polymarket like tobacco" |

| Mar 23–24 | Bipartisan Senate bill to ban sports bets on prediction markets — DKNG jumped 7–8% | "DraftKings Stock Jumps" — Barron's |

| Mar 25 | Reversal — DKNG fell 6% as market re-priced the bill's chances | Bearish |

| Apr 6, 2026 | Kalshi won federal court ruling limiting state enforcement | Big bearish catalyst — Kalshi legal runway expands |

| Apr 2, 2026 | Tennessee regulator told prediction markets to stop offering sports event contracts | Small local win for DKNG |

| Ongoing | CFTC appointed Kalshi, Polymarket, AND DraftKings CEO to advisory panel | Regulatory seat at the table |

Theme 2: Q4 2025 Earnings & FY2026 Guidance

On February 12, DraftKings reported Q4 revenue +43% YoY — but FY2026 guidance disappointed and the stock crashed 12–15%. Headline: "DraftKings Hits Earnings Grand Slam, But Shares Tank 15% on Souring 2026 Outlook." Cathie Wood's ARK Invest unloaded shares on the drop.

Theme 3: State Tax Hikes

Illinois imposed a $0.25 per-bet tax in July 2025. DKNG and FanDuel initially added $0.50 surcharges but retracted them when FanDuel refused to match. New Jersey raised its online gaming tax in June 2025. North Carolina's 2026 budget proposal would double the sports betting tax to 36%. March 11 headline: "Illinois Sportsbooks Continue to Report Wagering Declines" — the IL tax is actively suppressing handle.

Theme 4: Super Bowl LX & March Madness Handle

Super Bowl LX (Seahawks vs Patriots, February 8) saw $1.76B in total wagers. DKNG rose 5% on strong handle numbers. "2026 Super Bowl Put More Than $8B at Risk for DraftKings Sportsbook." March Madness 2026 projected $4B in bets. On March 19: "February Handle Shows DraftKings Closing Gap on FanDuel."

Theme 5: Super App & Strategic Moves

| Date | Event |

|---|---|

| Mar 2, 2026 | DKNG unveiled "Super App" vision (Sportsbook + Casino + DFS + Predictions in one app) |

| Mar 3, 2026 | DKNG stock +9.2% on Super App vision announcement |

| Mar 9, 2026 | ESPN account linking announced |

| Apr 2, 2026 | Washington D.C. lawsuit dismissed |

| Apr 7, 2026 | GuruFocus: "Overweight Rating with Raised PT" |

| Apr 8, 2026 | "DKNG Pops on Bullish Endorsements amid Sell-Off" |

Upcoming Catalysts

Market Sentiment

Social sentiment is structurally bearish: Twitter/X score of ~25/100, Reddit activity has gone nearly silent at peak sports betting season, and two prominent voices (Gary Black of Future Fund, Brent Donnelly of Spectra Markets) are publicly short. The dominant narrative (~75% of bear signal) is that prediction markets — Kalshi, Polymarket, Robinhood — are structurally threatening DraftKings' economic moat.

Reddit Activity (Notable Silence)

Despite March Madness and peak sports betting season, the major finance subreddits have gone nearly silent on DKNG. This itself is a notable bearish signal — retail has moved on.

- r/wallstreetbets: Zero dedicated DKNG posts in the past month — apathy at peak season is telling.

- r/stocks: Silent. Top comment on any DKNG thread is bearish: "Robinhood and Kalshi are eating their lunch" (+61 upvotes).

- r/DKNG (dedicated sub): Top post is "Guess I'm One of You Now..." — a bagholder confession. Second: "Kalshi Lags DraftKings in Sports Betting Favorability."

- r/ValueInvesting: FLUT threads frame DKNG as an inferior alternative. "Compare to Evolution AB at 12x forward P/E and actually profitable."

Bull & Bear Side-by-Side

Reddit Bull Quotes

- "They're going to win the prediction market too" — dcdrums502

- "Most users of prediction market apps are in states DKNG can't legally operate. Forward price $50" — FreddieMac6666

- "Increased TTM revenue every quarter, first positive EBITDA quarter, double-digit CAGR through 2030" — reddorickt

Reddit Bear Quotes

- +61 upvotes: "Robinhood and Kalshi are eating their lunch. Every broker will roll out prediction markets."

- +55 upvotes: "DKNG more in trouble from prediction markets than NBA scandal."

- "Jason Robins isn't buying stock, he's selling. Says he's most bullish ever but proves it by selling." — GroundedAndGrateful1

- "Market is over saturated. 6 sportsbooks in 2020, now 60+." — csvt2354

Twitter/X Bearish Voices

Negligible_cap (4.2K views, Mar 19): "At $22B, Kalshi is now valued higher than $DKNG ($12B market cap) and $FLUT ($18.6B). DKNG had $26B at 52W high in Feb '25." Gary Black (Future Fund, 12K views): "$DKNG -15% post-market after FY'26 Rev forecast fell short." StockSavvyShay (40K views): "$DKNG $15B & Polymarket just raised at $10B. It's wild that a decentralized prediction market still in early innings is closing the gap."

Contrarian Bull Voices

- A_P_Capital (Mar 25): "$DKNG down 7% on bill to ban sports betting on prediction markets. This is a bill they lobbied for. Huge net positive. Should be UP 10%+."

- BMO (Brian Pitz, Nov 2025): Maintains $63 price target, says prediction market fears are "overblown."

Insider & Institutional Activity

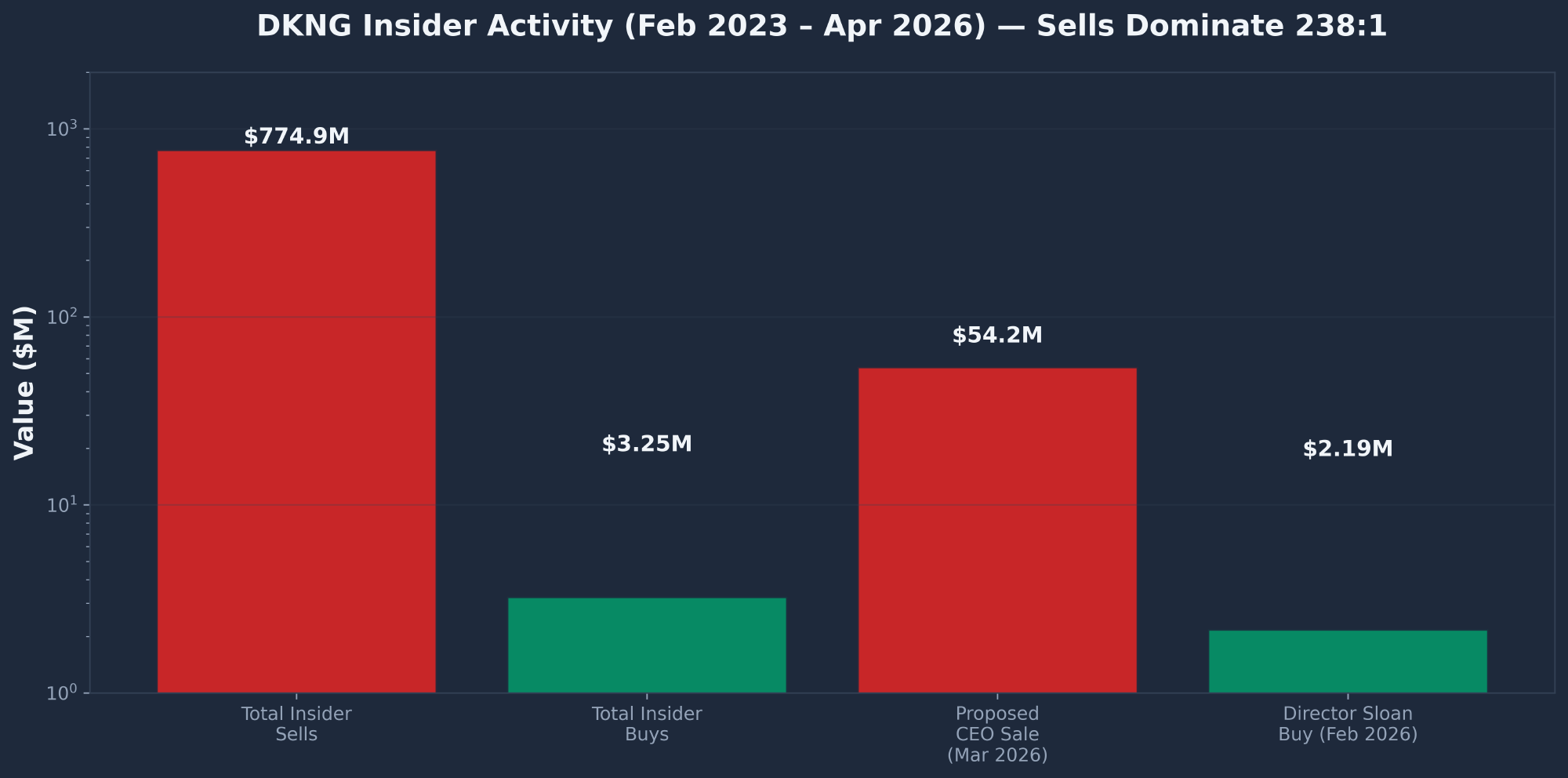

Headline Numbers (104-Trade Analysis, Feb 2023 – Mar 2026)

| Metric | Value |

|---|---|

| Total Sells | 101 transactions, 22.5M shares, $774.9M |

| Total Buys | 3 transactions, 135K shares, $3.25M |

| Sell/Buy Ratio (by dollar value) | 238.8x |

| Net Insider Activity | -$771.7M |

Co-Founder Sell Totals

| Insider | Role | Total Sold | Trades | Buys |

|---|---|---|---|---|

| Jason Robins | CEO | $226.0M | 23 | ZERO |

| Paul Liberman | Co-founder | $214.9M | 18 | ZERO |

| Matt Kalish | Co-founder | $144.4M | 11 | ZERO |

| R. Stanton Dodge | Chief Legal Officer | $110.8M | 25 | ZERO |

| Jason Park | Former CFO | $54.1M | — | ZERO |

| Combined Founder Cashouts | — | $585M | — | 0 |

Pending Form 144 Proposed Sales (The Bombshell)

The Contrarian Signal: Director Open-Market Buying

| Date | Insider | Shares | Price | Value |

|---|---|---|---|---|

| Feb 17, 2026 | Harry Sloan (Director) | +100,000 | $21.85 | +$2,185,000 |

| Nov 11, 2025 | Harry Sloan (Director) | +25,000 | $30.30 | +$757,500 |

| Nov 11, 2025 | Gregory Wendt (Director) | +10,000 | $30.27 | +$302,700 |

Institutional Ownership (Convertible Arb Dominated)

A critical nuance: most "institutional" ownership in DKNG is convertible arbitrage against DraftKings' $1.88B in convertibles, NOT real-money long-only. This makes the 87% institutional ownership figure misleading. Top holders:

| Holder | % of Portfolio | Type |

|---|---|---|

| AQR Arbitrage | 21.10% | Convertible Arb |

| Wolverine Asset Management | 19.36% | Convertible Arb |

| Calamos Advisors | 18.05% | Convertible Arb |

| DeepCurrents | 15.50% | Convertible Arb |

| Tudor Investment Corp | 13.66% | Convertible Arb |

| BlackRock | 12.33% | Long-only (only one in top 10) |

| Vanguard | 8.99% | Index |

Finviz shows institutional transactions at +8.10% last quarter — institutions were net buyers. Short interest stands at 37.5M shares (7.92% float), meaningfully shorted but not extreme.

Risk Factors

| Risk | Probability | Impact |

|---|---|---|

| Prediction market disruption. Kalshi, Polymarket, Robinhood capturing volume from traditional sportsbook — demonstrated by Kalshi's $871M Super Bowl handle and April 6 federal court win. Long-term margin compression risk is real. | MED-HIGH | HIGH |

| State tax hikes. Illinois $0.25 per-bet tax already suppressing handle. NJ and others raising rates. North Carolina proposed 36% tax rate. Federal excise tax risk looming. | HIGH | MEDIUM |

| CEO accelerated selling. Jason Robins' $54M proposed Form 144 sale at $25.43 after a 35% YTD decline is a high-weight bear signal. Founders do not typically sell this aggressively into weakness. | HIGH (already filed) | MEDIUM |

| Gambling outcome volatility. Sport results (favorite-heavy NFL weekends) can cause short-term hold % swings. Q3 2025 reverted to a loss on this. Will repeat quarterly. | HIGH | LOW |

| Heavy SBC dilution. $339M stock-based comp (5.6% of revenue) is real dilution that offsets reported FCF quality. Adds ~2.9% YoY to share count. | CERTAIN | LOW-MED |

| Debt load increased. New $576M Term B loan plus $1.26B converts = $1.84B total debt. Net debt to Adj EBITDA is only 0.4x, but the direction is concerning. | CERTAIN | LOW |

| Macro / recession. Discretionary consumer spending sensitivity. A recession would hit betting handle and player retention simultaneously. | LOW-MED | HIGH |

| Cybersecurity. Handles sensitive KYC data and payments; breach risk is operational. | LOW | MEDIUM |

| Responsible gaming / advertising restrictions. Problem gambling and reputational risk; potential regulatory advertising restrictions. | LOW-MED | MEDIUM |

Conclusion & Price Targets

Price Target Derivation

| Method | Input | Multiple | Per Share |

|---|---|---|---|

| EV/Sales | $7.2B 2026E revenue | 2.4x (Flutter-like) | ~$35 |

| EV/Adj EBITDA | $850M 2026E Adj EBITDA | 20x | ~$34 |

| DCF (mid-case) | 9% WACC, 3% terminal | — | ~$34 |

| Blended Target | — | — | $35.00 |

Scenario Analysis (12-Month)

| Scenario | Probability | Target | Return | Key Drivers |

|---|---|---|---|---|

| Bull | 25% | $45 | +99% | Q1 beat + guide raise + prediction market launch well-received |

| Base | 50% | $35 | +55% | Multiple re-rating toward Flutter comparable + in-line execution |

| Bear | 20% | $19 | -16% | Guidance cut, tax headwinds, mild recession |

| Worst | 5% | $14 | -38% | Prediction markets truly disrupt, federal tax shock |

| Probability-Weighted | 100% | ~$33.70 | +48.9% | Attractive expected value |

Bull Case: $45 (+99%)

- Q1 2026 revenue beat + FY2026 guidance raise

- DKNG prediction market launch captures meaningful share

- Senate ban on sports prediction markets passes

- Adj EBITDA crosses $900M on operating leverage

- Multiple re-rates to 2.5x forward P/S (Flutter premium)

- Robins halts additional Form 144 filings

Bear Case: $19 (-16%)

- Q1 2026 miss triggers second guidance cut

- Kalshi & Polymarket compound market share gains

- North Carolina passes 36% tax; Illinois raises again

- Robins executes $54M Form 144, sentiment collapses

- Q2/Q3 2026 sport outcomes return to unfavorable mix

- Multiple compresses toward 1.3x forward P/S

Action Plan

| Parameter | Recommendation |

|---|---|

| Portfolio Allocation | 3-5% of equity portfolio. Inherent volatility warrants moderate sizing. |

| Entry Strategy | Scale in 1/3 at $22.63, 1/3 on retest of $21.00, 1/3 if $20.00-$20.50 holds. |

| Stop-Loss | Hard stop on any weekly close below $18.00. Below = long-term trend break. |

| Profit Targets | Trim 25% at $30 (SMA50 retest). Trim 25% at $35 (target 1). Full exit at $42+ or thesis break. |

| Risk/Reward | ~55% upside to $35 target vs ~20% downside to stop = 2.67:1 risk/reward. |

| Key Review Dates | Q1 2026 earnings (late April/early May 2026). Exit entirely if Q1 misses or if Jason Robins executes $54M Form 144 without corresponding insider buying. |

The Bottom Line

This DraftKings stock analysis rates DKNG a medium-to-high conviction BUY at $22.63 with a 12-18 month price target of $35.00 (+55% upside). The core setup is simple: a company delivering its fundamental inflection (first GAAP profit, Adj EBITDA +242%, FCF +$648M) while the stock trades 58% below its all-time high, RSI at 28, and a director just bought $2.2M on the open market at essentially today's price. The prediction market narrative is real but appears priced in at 1.85x forward sales after Goldman's $54→$31 cut and the 35% YTD decline.

The risk/reward of 2.67:1 with upside to a Flutter-comparable multiple is the trade. Position at 3-5% of portfolio, scale in on weakness, and respect the $18 hard stop. Q1 2026 earnings in late April or early May is the key catalyst — a revenue beat combined with a stabilized FY2026 guide could trigger the first meaningful rally from these washed-out levels.

For options traders, DKNG's high implied volatility and contrarian setup make it a potential candidate for the wheel strategy. You can also review criteria for selecting the best stocks for the wheel strategy, consider selling cash-secured puts to build a position at a discount, or explore generating monthly income with options on high-IV stocks like DKNG. For reducing cost basis on shares you already own, see how to lower your stock basis using options.

Sources: SEC Filings, Finviz, Polygon.io, Google News, Reddit, Twitter/X. Report compiled April 9, 2026.

Frequently Asked Questions

Is DKNG a good stock to buy right now?

Based on this DraftKings stock analysis, DKNG is rated a BUY at $22.63 with a 12-18 month price target of $35.00 (+55% upside). The thesis rests on DraftKings' first-ever GAAP profitable year, oversold technical conditions (RSI 28, 36% below SMA200), and Director Harry Sloan's $2.2M open-market buy in February 2026. The primary risks are prediction market disruption from Kalshi/Polymarket and CEO Jason Robins' proposed $54M Form 144 sale. Position sizing should be 3-5% of a portfolio with a hard stop at $18.00.

What is the DraftKings stock price target?

The Wall Street consensus price target for DraftKings stock (DKNG) is approximately $35.32, representing roughly 57% upside from current levels. Individual analyst targets range from $31 (Goldman Sachs, after February cut from $54) to $53 (Morgan Stanley, January upgrade). This analysis sets a base-case 12-18 month target of $35.00 derived from an EV/Sales of 2.4x on $7.2B FY2026E revenue, supported by EV/Adjusted EBITDA of 20x on $850M 2026E Adjusted EBITDA.

Should I buy or sell DKNG stock?

The recommendation is to buy at current levels with a scaled entry: 1/3 position at $22.63, 1/3 on a retest of $21.00, and 1/3 if $20.00–$20.50 holds as support. Sell signals include a weekly close below $18.00 (long-term trend break) or a Q1 2026 earnings miss combined with FY2026 guidance cut. The primary upside trigger is Q1 2026 earnings in late April or early May — a revenue beat with stabilized guidance could catalyze the first meaningful rally from these washed-out levels.

What is the DraftKings stock forecast for 2026 and beyond?

In the base case, DKNG reaches $35.00 within 12-18 months driven by multiple re-rating toward a Flutter-comparable 2.4x forward P/S as the prediction market fear subsides. The bull case sees $45 if Q1 beats, FY2026 guidance is raised, and DraftKings' own prediction market platform captures meaningful share. The bear case is $19 if prediction market disruption accelerates and state tax hikes compound into FY2027. The stretch target is $42+ on a full multiple expansion. Key review catalysts: Q1 2026 earnings (April/May), March Madness handle data, and the Senate bill on sports prediction market regulation.

Will prediction markets like Kalshi kill DraftKings?

The short answer is probably not, but they will compress margins. Kalshi's April 6, 2026 federal court win expanded its legal runway, and its $871M Super Bowl volume proves the threat is real. However, DraftKings operates in 20+ licensed states with full KYC and responsible gaming compliance, whereas prediction markets exist in a regulatory gray zone that faces mounting state-level pushback (Tennessee blocked sports event contracts on April 2, and a bipartisan Senate bill to ban sports prediction markets was introduced March 23-24). DraftKings is also launching its own CFTC-approved prediction market platform — this becomes a feature war rather than a winner-take-all. At 1.85x forward sales, the prediction market fear appears fully priced in.

How does DKNG compare to Kalshi and prediction markets?

Kalshi did $871M in Super Bowl 2026 handle — directly competing with DraftKings' traditional sportsbook. The vig difference is the core bear case: for the Super Bowl, a $100 bet paid $77 on DKNG versus $88.70 on Kalshi — materially better odds for bettors on prediction markets. DraftKings' defensive response includes launching its own CFTC-approved prediction market platform in December 2025, acquiring Railbird for $250M, partnering with Polymarket as a clearinghouse, and securing a CFTC advisory seat. The bipartisan Senate bill introduced March 23–24, 2026 to ban sports bets on prediction markets would be a major catalyst for DKNG if it passes. For now, prediction markets operate in a regulatory gray zone that favors the incumbent sportsbooks in their licensed states.