ETSY (Etsy) Stock Analysis: Hold at $61.90 | $65 Target

Table of Contents

Executive Summary

This ETSY stock analysis (Etsy, Inc.) covers fundamentals, technicals, SEC filings, market sentiment, insider activity, and our Etsy stock forecast 2026 as of April 2026. If you are asking "is ETSY a good stock to buy?" — the short answer is hold. Here is the bottom line:

- HOLD at $61.90 with a 12-18 month target of $65 (+5% upside). The Wall Street consensus target of $61.79 sits literally at market price — meaning the Street sees zero edge from here. This is not a conviction entry point.

- RSI 72.5 overbought heading into a binary Q1 2026 earnings event on April 29, 2026 (11 days from report compilation). ETSY has missed EPS in 3 of the last 6 quarters and reacted -5% to -15% on report day. The stock has surged +17.5% in the last week on the Depop sale, stretching every indicator.

- Activist thesis is intact but priced in: Elliott Management holds 5.19% (Marc Steinberg joined the Board February 5, 2024) plus Impactive Capital's 3.16% equals 8.35% of the register explicitly activist. The playbook is executing — Reverb divested, CEO transition, Depop sold to eBay for $1.2B.

- Valuation is genuinely cheap on free cash flow (9.3x P/FCF) — cheapest among peers (EBAY 11x, W 12x, AMZN 30x, SHOP 50x). But P/E TTM 45.6x, negative book value of -$11.32/share, and 3 consecutive years of negative GMS growth argue against paying a premium.

- $1.2B Depop proceeds inbound Q2 2026 funds the $649.9M October 2026 debt cliff plus $550M of incremental buybacks. Pro-forma deployable cash post-retirement is ~$2.25B — that is the downside cushion at $45.

| Report | Signal | Key Finding | Weight |

|---|---|---|---|

| Fundamentals | MIXED | Cheap on FCF (9.3x) but P/E 45 TTM, negative book value, $1.5B M&A destruction | 20% |

| SEC Filings | MIXED | Elliott activist confirmed (bullish) but management credibility moderate-trending-low; $650M Oct 2026 cliff | 20% |

| Technical | MIXED | Bullish momentum (+40% YoY) but RSI 72.5 overbought into earnings; $63-65 resistance | 15% |

| News & Events | MIXED | 42 articles, two-wave narrative — Feb bullish Depop/earnings then March reset on soft guide | 15% |

| Insider/Institutional | MIXED | 100% insider selling (mostly mechanical 10b5-1) but Elliott 5.19% + Impactive 3.16% activist bullish | 15% |

| Sentiment | MIXED | Bear arguments dominate Reddit but loudest short flipped bullish post-Depop announcement | 15% |

| COMPOSITE | 6/6 MIXED | No clear directional edge justifies HOLD — not BUY, not SELL | 100% |

Investment Thesis

Etsy is a "show-me" stock 11 days from a binary catalyst. Every report signal comes back mixed. Elliott Management is running the activist playbook from the boardroom, $1.2B in Depop proceeds is en route, and the stock trades at a reasonable 9.3x price-to-free-cash-flow. But management has destroyed $1.5B on failed mergers and acquisitions (Depop $897M goodwill impairment, Elo7 $147M, Reverb $102M), core marketplace GMS just posted its first positive quarter in two years (a trend of exactly one data point), and the analyst consensus $61.79 target sits literally at the current price. The Street sees zero edge.

The thesis has four pillars. First, Elliott is running the playbook from the boardroom. Marc Steinberg (Elliott Partner, 35) joined the Etsy Board on February 5, 2024. Every subsequent strategic action fits the activist script: $1B buyback (October 2024), new CFO Lanny Baker (November 2024), Reverb sale (June 2025), Silverman out as CEO (December 2025), Wilson out as Chair (December 2025), universal-proxy bylaws (December 2025), $750M buyback authorization (December 2025), Depop sale to eBay for $1.2B cash (February 2026). With Impactive Capital's 3.16% added to Elliott's 5.19%, 8.35% of the register is explicitly activist. That is a real catalyst — but one the market has already mostly absorbed.

Second, the April 29 earnings print is a binary event on a stretched technical setup. ETSY is up 17.5% in the last week and 14.4% in the last month, pushing RSI to 72.5 (overbought) and the price to 17.1% above the 20-day SMA. Q4 2025 delivered the first positive Etsy marketplace GMS quarter (+0.1%) in two years — but one data point is not a trend. Q1 2026 consensus is $0.61 EPS on $621M revenue; Etsy's Q1 2025 was -$0.49 vs. estimate +$0.47, a -204% miss on the Reverb impairment. Buying here 11 days before the print, with the stock extended and consensus target at the tape, is asymmetric in the wrong direction.

Third, valuation is fair, not compelling. On trailing P/FCF (9.3x) ETSY is genuinely cheap for a 71.6%-gross-margin marketplace. On forward P/E (17.7x) it is reasonable. Applying a probability-weighted framework (25% bear $45, 50% base $65, 25% bull $90) yields $66.25 — rounds to $65. Fourth, position sizing matters more than the call. With beta 1.84, short float 16.54%, RSI 72.5 into earnings, and a 5-year return of -72%, this is a high-variance name. The right position size is 1-2% of book given binary catalysts. The right entry is a pullback to $50-55 (below the 50-day SMA) where risk/reward improves to roughly 3:1, or a confirmed post-earnings breakout above $75 on volume. Not $61.90 the week before earnings.

Fundamental Analysis

Company Overview

Etsy, Inc. (NYSE: ETSY) operates a peer-to-peer online marketplace for handmade, vintage, and craft goods. Founded in Brooklyn, New York in 2005 and taken public on the NASDAQ in April 2015 at $16 per share, Etsy transferred to the NYSE in October 2025. The company employs 2,375 people. Sellers are largely independent micro-merchants; Etsy monetizes via transaction fees, listings, Etsy Ads (including Offsite Ads), and Etsy Payments. The dividend is zero — capital return runs exclusively through buybacks.

Leadership as of April 2026: Kruti Patel Goyal (CEO since January 1, 2026), Josh Silverman (Executive Chair, former CEO 2017-2025), Charles "Chuck" Baker (CFO since November 2024), Colin Stretch (Chief Legal Officer). Marc Steinberg of Elliott Investment Management sits on the Board since February 5, 2024 — a governance inflection that explains every subsequent strategic action.

The segment structure has been dramatically simplified. Etsy core (90%+ of GMS) is the flagship handmade marketplace. Reverb (musical instruments) was divested in April 2025 for $105M. Depop (Gen Z resale fashion) was sold to eBay for $1.2B cash announced February 18, 2026, closing Q2 2026. Elo7 (Brazilian crafts) was wound down at a total loss. The company is now a single-platform pure-play handmade/vintage marketplace.

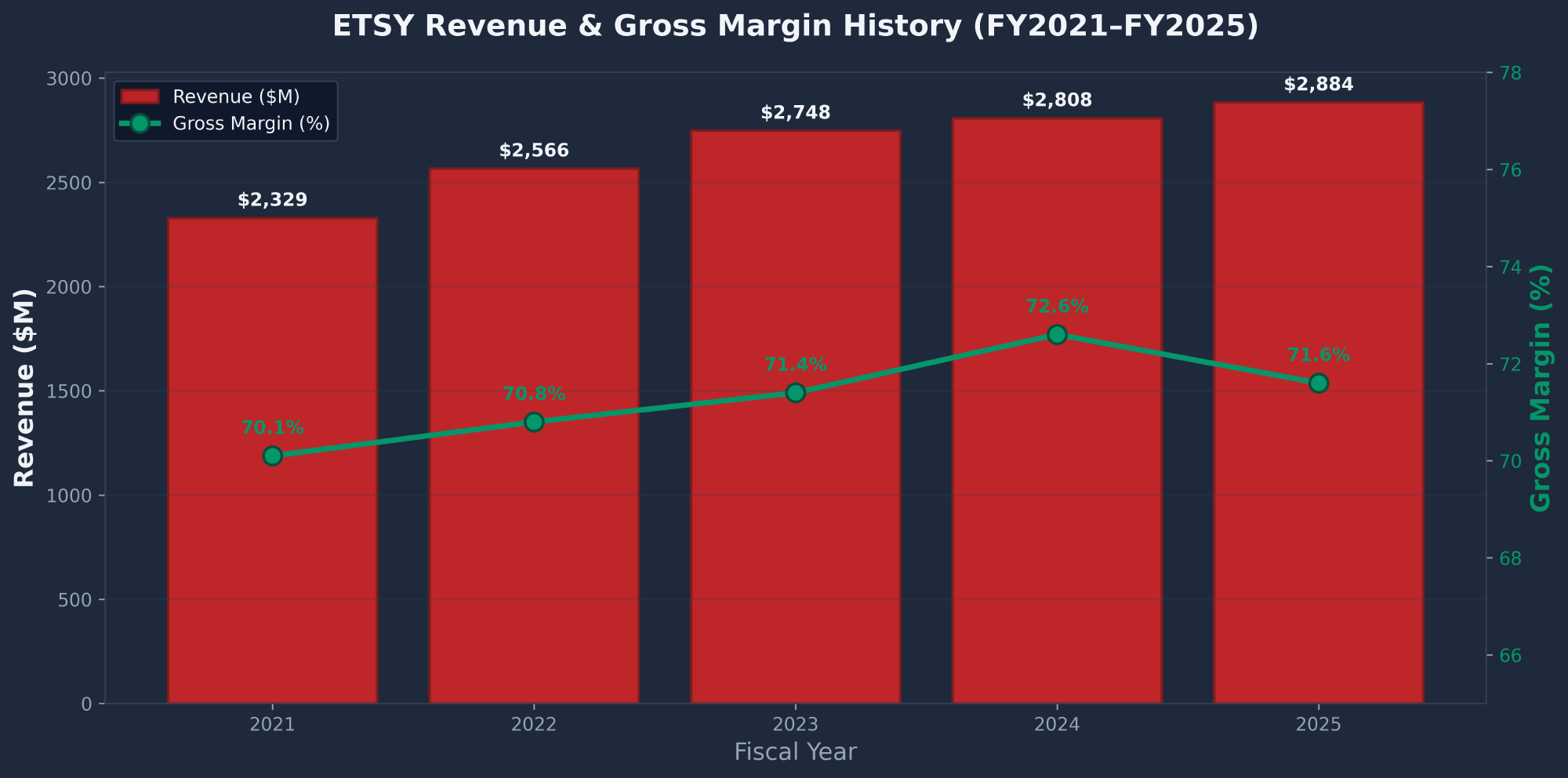

Revenue & Gross Margin History

Revenue has grown from $2.33B in 2021 to $2.88B in 2025 — a compound annual growth rate of only 5.5%. Gross margins have been extraordinarily stable at 70-73%, reflecting the asset-light marketplace model. The key tension: FY2025 revenue was up just 2.68% year-over-year while net income fell 46% — driven by the Q1 2025 Depop-related goodwill write-down of $293M plus ongoing Depop operating losses.

Multi-Year Income Statement

| Metric ($M) | FY2024 | FY2025 | YoY |

|---|---|---|---|

| Total Revenue | 2,808.33 | 2,883.51 | +2.68% |

| Gross Profit | 2,039.43 | 2,065.71 | +1.29% |

| Operating Income | 407.85 | 366.25 | -10.20% |

| EBITDA | 515.92 | 468.09 | -9.27% |

| Net Income | 303.29 | 162.97 | -46.27% |

| Diluted EPS | $0.59 | $0.34 | -42.4% |

| Stock-Based Comp | 223.45 | 207.42 | -7.17% |

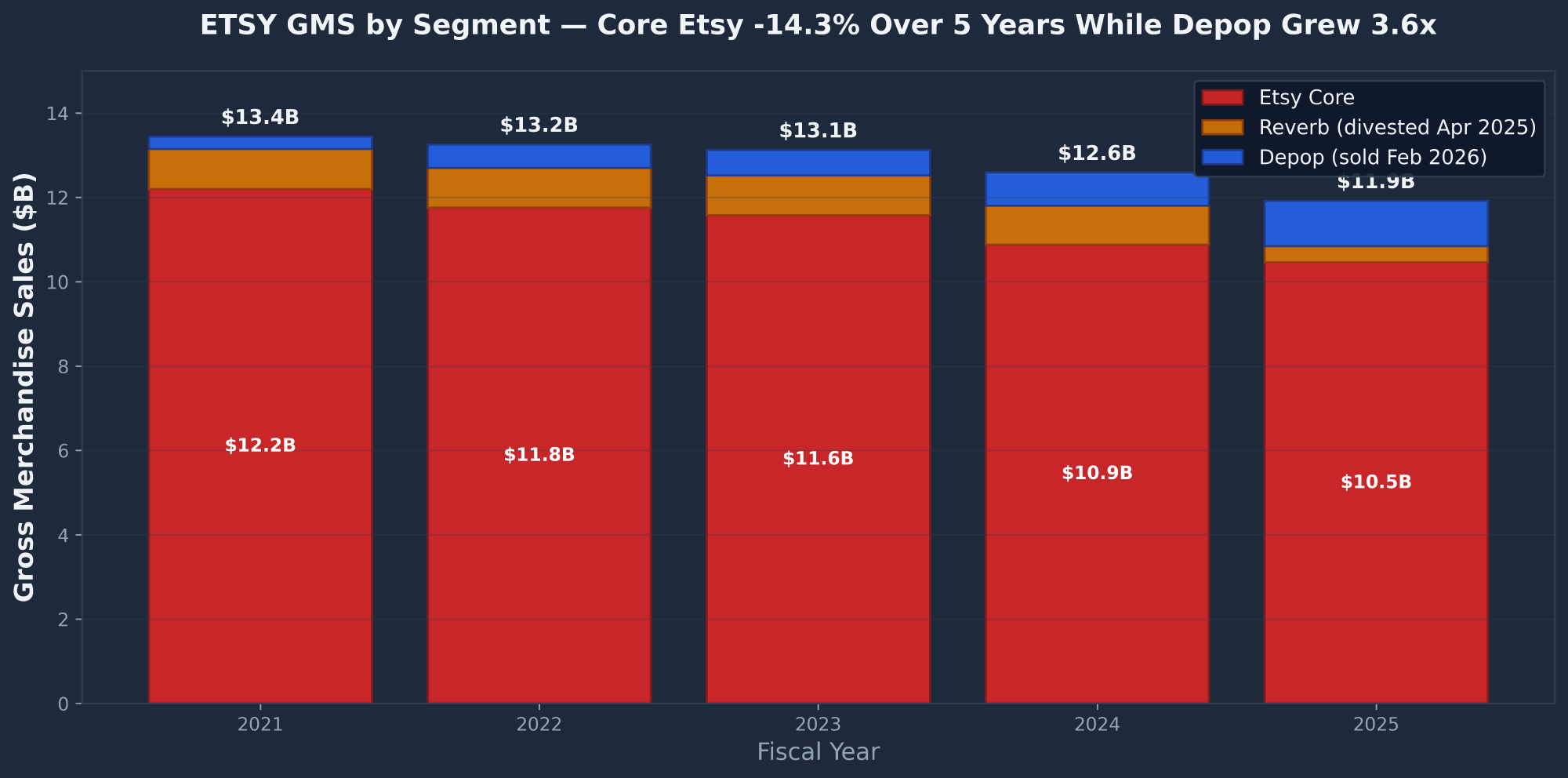

GMS by Segment — The Core Problem

Here is the unvarnished story: Core Etsy GMS has declined every year since 2021. Depop was the entire "growth" narrative — and Etsy just sold it to eBay. The core marketplace shrank from $12.20B (2021) to $10.46B (2025), a 14.3% decline over four years, while global e-commerce grew.

| Year | Etsy Core ($M) | Reverb | Depop | Elo7 | Total GMS | YoY |

|---|---|---|---|---|---|---|

| 2021 | 12,196.7 | 948.0 | 294.4 | 32.0 | 13,491.8 | +31.2% |

| 2022 | 11,754.1 | 942.5 | 552.1 | 69.7 | 13,318.4 | -1.3% |

| 2023 | 11,577.4 | 942.1 | 599.6 | 42.1 | 13,161.2 | -1.2% |

| 2024 | 10,880.1 | 917.9 | 788.9 | — | 12,587.0 | -4.4% |

| 2025 | 10,460.7 | 381.3 | 1,074.9 | — | 11,916.9 | -5.3% |

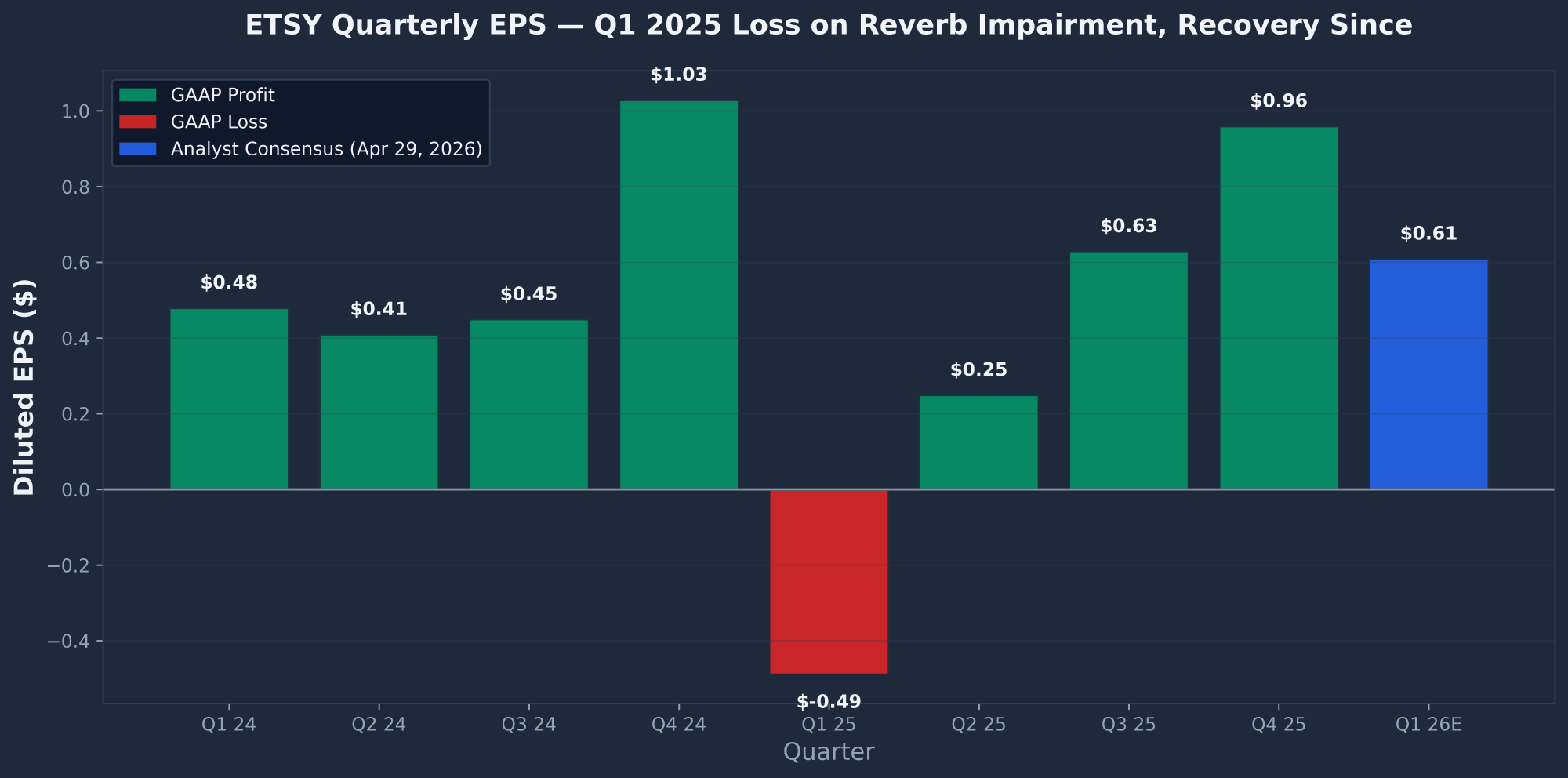

EPS Trajectory — Lumpy but Improving

The quarterly picture is more informative than annual. Q4 2025 delivered EPS of $0.96 on revenue of $881.64M (+3.5% YoY) — the best quarter in company history. Operating income of $130.50M at a 14.8% operating margin shows real leverage. Core Etsy marketplace GMS grew +0.1% — the first positive print in two years (since Q3 2023). US buyer GMS grew +0.3% — the first positive in four years. Q1 2026 consensus: $0.61 EPS on $621M revenue, reporting BMO April 29, 2026.

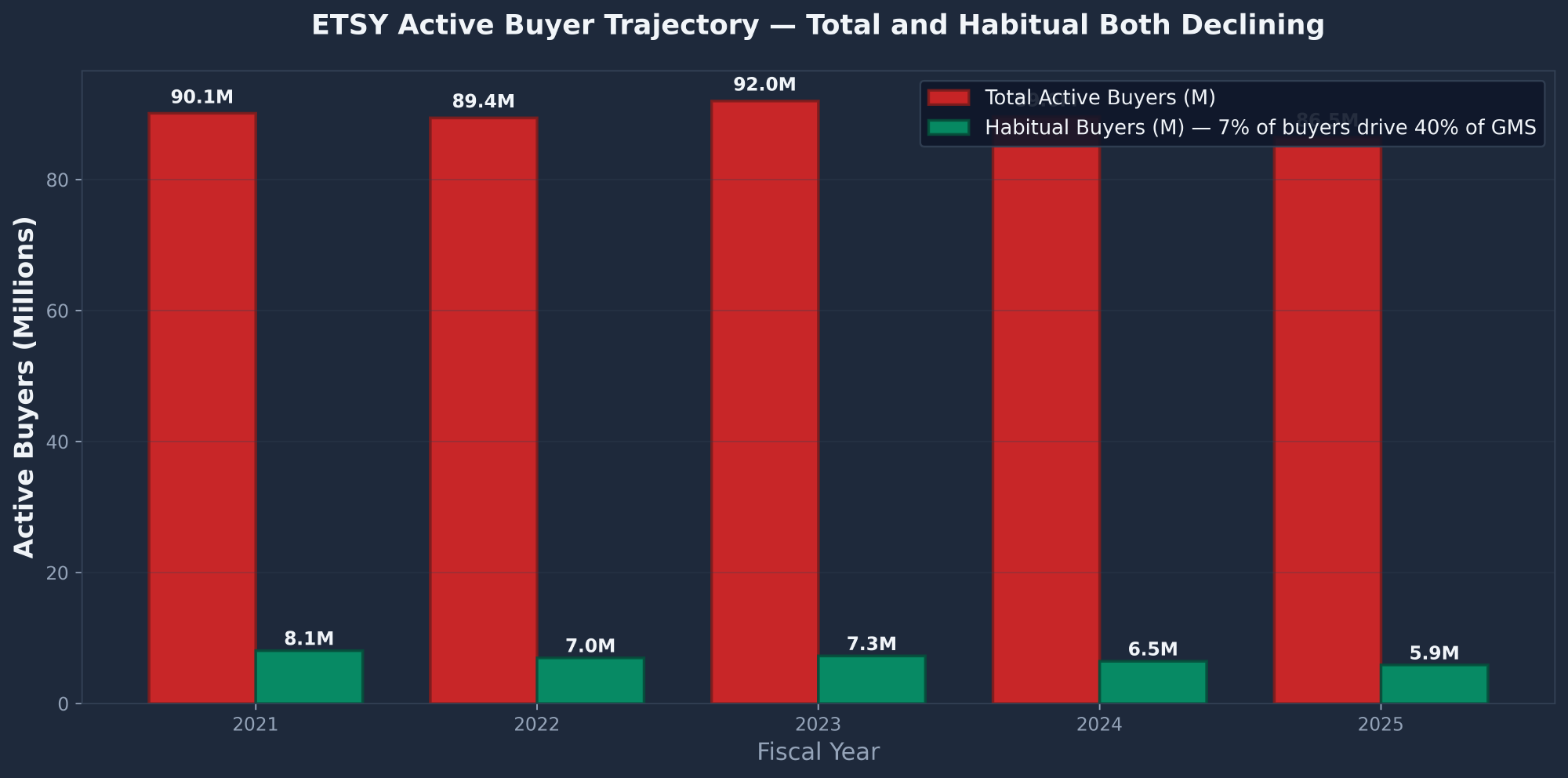

Active Buyer Trajectory

Etsy.com active buyers have declined from 90.1M (2021) to 86.5M (2025). More concerning, habitual buyers (6+ purchase days and $200+ TTM spending) have dropped from 8.1M to 5.9M — and this 7% of the buyer base drives roughly 40% of GMS. The extreme concentration means buyer churn at the top has outsized impact. Reactivated buyers hit a record 30.0M in 2025, but the company is harvesting lapsed users rather than acquiring new ones.

Valuation Snapshot

| Metric | Value | Metric | Value |

|---|---|---|---|

| Market Cap | $5.96B | Enterprise Value | $7.45B |

| P/E TTM | 45.61x | Forward P/E | 17.67x |

| PEG | 0.40 | P/FCF | 9.33x |

| P/Sales | 2.07x | EV/EBITDA | 15.92x |

| Gross Margin | 71.64% | Operating Margin | 12.70% |

| ROIC | 11.93% | Book Value/Share | -$11.32 |

| Cash/Share | $16.83 | Analyst Target | $61.79 |

Peer Comparison

| Peer | Fwd P/E | P/FCF | EV/EBITDA | Notes |

|---|---|---|---|---|

| EBAY (eBay) | ~11 | ~11 | ~9 | Most direct comp — mature marketplace, low growth |

| SHOP (Shopify) | ~55 | ~50 | ~35 | Growth premium — not a valuation comp |

| W (Wayfair) | ~25 | ~12 | ~18 | Discretionary marketplace; margin-challenged |

| AMZN (Amazon) | ~30 | ~30 | ~18 | AWS inflates multiple — not pure comp |

| ETSY (target) | 17.7 | 9.3 | 15.9 | Cheapest P/FCF in group; above-EBAY EV/EBITDA |

Technical Analysis

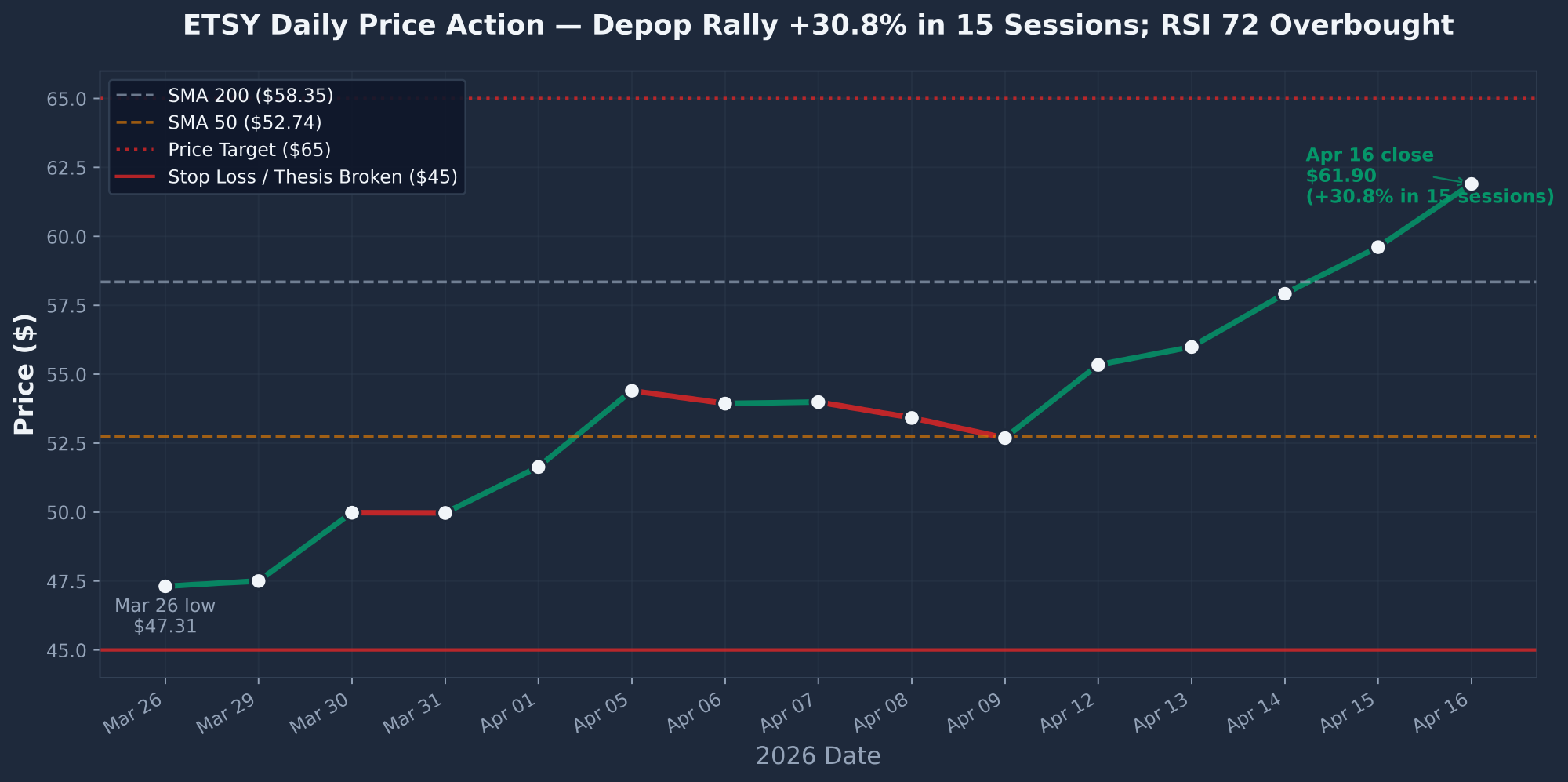

ETSY just executed a V-bottom reversal from the February 2026 low of $45.56, rallying +38% to $61.90 into the April 29 earnings print. The technical setup is bullish but stretched: price is 17.4% above the 50-day SMA and just reclaimed the 200-day SMA at $58.35 on April 15. RSI surged from 51 to 72.5 in just six sessions — overbought, though not yet extreme.

Moving Averages & Indicators

| Indicator | Value | Price vs | Signal |

|---|---|---|---|

| SMA 10 | $55.92 | +10.7% | Bullish — first pullback target |

| SMA 20 | ~$52.86 | +17.1% | Extended above 20-day |

| SMA 50 | $52.74 | +17.4% | Clean break above intermediate MA |

| SMA 200 | $58.35 | +6.1% | Just reclaimed — crucial inflection |

| RSI (14) | 72.52 | Overbought | Caution — mean-reversion risk |

| MACD Line | +1.68 | Above zero | Bullish |

| MACD Histogram | +1.14 | Expanding | Strong momentum acceleration |

| Beta | 1.84 | High vol | Moves ~2x market |

| ATR (14) | $2.49 | ~4.0% daily | Elevated volatility profile |

Daily Price Action — The Depop Rally

The last 15 sessions tell the story. After closing at $47.31 on March 26, ETSY rallied to $61.90 by April 16 — a +30.8% gain in 15 trading sessions. Four consecutive green candles from April 12-16 reclaimed the SMA 200 and breached the $58 resistance pivot. Volume confirmed the move, with 3.26M shares on April 16 versus the 20-day average of ~2.5M.

Support & Resistance

| Level Type | Price | Significance |

|---|---|---|

| ATH (Dec 2023) | $89.58 | All-time high — long-term upside target |

| 52W High | $76.52 | Major resistance — last year ceiling |

| Oct 2025 High | $74.00 | Reversal pivot — -17% week followed |

| Fib 61.8% (2023-25) | $70.64 | Strong resistance — 2025 July high area |

| Target / Pivot Zone | $63–$65 | Immediate resistance — first big test |

| CURRENT PRICE | $61.90 | Between support and first resistance |

| SMA 200 | $58.35 | Major support — just reclaimed |

| SMA 10 | $55.92 | Ascending support from Feb lows |

| SMA 50 | $52.74 | Strong support — Fib 61.8% confluence |

| Feb V-Bottom | $45.00 | Critical — thesis broken below |

| Stop Loss | $45.00 | Sustained break stops out activist value thesis |

SEC Filings & Activist Playbook

Etsy spent 2019-2021 building a "House of Brands" via acquisitions, then spent 2023-2026 unwinding every piece of it. The February 2024 arrival of Elliott Management on the Board is the inflection point that explains every subsequent action.

Corporate Timeline

| Date | Event |

|---|---|

| 2005 | Etsy founded in Brooklyn, NY |

| April 2015 | IPO on NASDAQ at $16/share |

| May 2017 | Josh Silverman becomes CEO; Fred Wilson becomes Chair |

| August 2019 | Reverb acquired (~$275M); 2019 Notes issued ($649.9M, 0.125%, Oct 2026) |

| 2020 | COVID surge: GMS doubles to $10.3B |

| July 2021 | Depop acquired ($1.493B) + Elo7 acquired ($212M) — "House of Brands" begins |

| Q3 2022 | Goodwill impairments: $897.9M Depop + $147.1M Elo7 — 14 months after purchase |

| August 2023 | Elo7 divested at loss ($2.6M sale + $68.1M impairment) |

| Feb 5, 2024 | Marc Steinberg (Elliott Management Partner) joins Board — governance inflection |

| October 2024 | $1B buyback program authorized |

| November 2024 | New CFO Lanny Baker replaces Glaser |

| April-June 2025 | Reverb sold for $105M — $101.7M Q1 impairment + $5.1M sale loss |

| June 11, 2025 | $700M 2025 Notes issued (1.00%, June 2030, $85.79 conversion) — NO capped call |

| October 13, 2025 | NASDAQ → NYSE listing transfer — unusual for mature issuer |

| October 24, 2025 | Silverman CEO step-down announced; Kruti Patel Goyal named successor |

| December 16, 2025 | Defensive bylaws (Rule 14a-19) + $750M new buyback authorization |

| Jan 1, 2026 | Patel Goyal CEO; Silverman → Exec Chair; Wilson → Lead Independent Director |

| Feb 18, 2026 | Depop sold to eBay for $1.2B cash — six weeks into new CEO's tenure |

Management Credibility Scorecard

| Promise | Verdict | Delivery |

|---|---|---|

| House of Brands strategy (2021) | MISSED | Elo7, Depop, Reverb all divested at loss |

| Seven core geographies (2022) | MISSED | UK revenue -15%; India de-emphasized |

| Reignite GMS growth (2022-2024) | MISSED | GMS -4.4% 2024, -5.3% 2025 |

| Etsy Ads ML relevancy | DELIVERED | Services revenue +11.3%, +$62.2M ads |

| 11% workforce reduction | DELIVERED | Completed Q1 2024; $26.6M charge |

| Return FCF via buybacks | DELIVERED | $2.1B stock bought 2023-2025 |

| Offset dilution with buybacks | DELIVERED | Shares 126.4M → 102.4M = -19% |

Pro-Forma Cash Ladder (Post-Depop, Post-Debt)

| Cash & equivalents (Dec 31, 2025) | $1,395.8M |

| + Short-term investments | $224.1M |

| + Long-term investments | $134.4M |

| = Total liquid assets | ~$1,754M |

| + Depop sale proceeds (Q2 2026) | +$1,200M |

| Pro-forma cash | ~$2,954M |

| − 2019 Notes repayment (Oct 2026) | -$650M |

| Post-retirement deployable cash | ~$2,254M |

| + Undrawn $400M revolver (Mar 2028) | $400M |

News & Catalysts

Etsy's 60-day news cycle follows a clean two-wave narrative. Wave 1 (mid-February) was decisively bullish: the $1.2B Depop sale to eBay (Feb 18) plus a Q4 beat (EPS $0.92 vs $0.88) and the first positive core GMS print in 2 years (+0.1%) drove the stock +10-14% in a single session. Wave 2 (mid-to-late March) was a reset — shares fell -5.2% on March 24 as the market digested soft 2026 guidance (GMS $2.38-$2.43B, take rate ~25.5%, EBITDA margin 28-30%) and a "show-me" tone settled across sell-side notes.

Top Stories

| Date | Story | Impact |

|---|---|---|

| Feb 18, 2026 | Etsy sells Depop to eBay for $1.2B cash. Paid $1.625B in 2021 — realizes ~26% loss on original purchase. Closes Q2 2026. | Stock +10-14% on news |

| Feb 19, 2026 | Q4 2025 earnings beat. EPS $0.92 vs $0.88 consensus. Revenue $881.6M (+3.5% YoY). Core Etsy GMS +0.1% — first positive print in 2 years (since Q3 2023). US buyer GMS +0.3% — first positive in 4 years. | Confirms GMS inflection |

| Feb 19, 2026 | Q1 2026 guidance issued. GMS $2.38-$2.43B (+2-4% YoY). Take rate ~25.5%. Adjusted EBITDA margin 28-30%. Mid-range implies deceleration vs Q4. | Triggered -5.2% Mar 24 selloff |

| Jan 1, 2026 | CEO transition. Kruti Patel Goyal takes over from Silverman. Previously ran Etsy's marketplace & Depop. April 29 will be her first earnings call. | Structural/strategic |

| Feb 19, 2026 | $750M new buyback authorization. Brings total capacity to ~$1B when combined with prior authorization. | EPS tailwind |

| Feb 11, 2026 | Google Universal Commerce Protocol co-developer. Etsy launch partner alongside OpenAI, Microsoft Copilot, Stripe. Agentic traffic up 15x YoY. | Long-term optionality |

| Sep 2025 (context) | OpenAI Instant Checkout partnership — drove +16% single-day move at announcement. | Narrative anchor |

Analyst Ratings — The $40 Spread

Consensus is 2.50 (Hold) with an average target of $61.79 — essentially spot. But the spread is $40 wide, from Arete's Sell at $43 to Truist's Buy at $83. Analysts genuinely disagree on whether this is a terminal decline or a turnaround.

| Firm | Rating / PT | Date |

|---|---|---|

| Truist Securities | Buy $83 | Feb 23, 2026 |

| Barclays | Equal → Overweight | Mar 1, 2026 |

| Bank of America | Buy $65 | Mar 12, 2026 |

| Needham | Buy $65 | Mar 10, 2026 |

| Morgan Stanley | Equal-Weight $60 (cut from $65) | Mar 14, 2026 |

| JP Morgan | Neutral $58 | Feb 26, 2026 |

| Stifel | Hold $55 | Feb 28, 2026 |

| UBS | Neutral $53 | Feb 24, 2026 |

| Wells Fargo | Underweight $47 | Mar 20, 2026 |

| Arete | Sell $43 | Jun 11, 2025 |

| Goldman | Sell $45 | Feb 20, 2026 (maintained) |

Market Sentiment

Sentiment is mixed, leaning cautiously bullish post-Depop sale. Bears dominate volume on Reddit but the loudest short — u/HunterMichael92 with 150K shares short — flipped bullish with a $62.50 EV-based target. Twitter/X features quieter, thoughtful bulls: GMT Capital's Thomas Claugus II (verified account @tclaugus2) holds a 6% position and added at $48.20 in March 2026. Chatter level is below average; r/wallstreetbets has had zero dedicated threads in 6 months — the "forgotten name" setup.

Bull & Bear Side-by-Side

Reddit & Twitter Bull Quotes

- "DCF: 6% growth, 9% FCF yield, 18x forward P/E = $101 fair value vs $61.90 spot. ~63% upside." — u/KnowledgePatient7813

- "Was short 150K shares at $35 target; flipped post-Depop sale. Target $62.50." — u/HunterMichael92 (the biggest short)

- "24.9% FCF margin; TTM FCF = 26% of LT debt; 27x interest coverage." — r/ValueInvesting

- "$750M buyback = 17.7% of market cap. Board conviction signal." — u/TowelNo234

- "GMT Capital's Claugus at 6% position, added at $48.20 in March." — @tclaugus2

Reddit & Twitter Bear Quotes

- "Etsy lost its soul — flooded with mass-produced junk and dropshipped crap." — r/stocks top comment

- "Silverman took $300M comp over 10 years. Depop $1.625B → $1.2B (loss). Elo7 impaired 90%. Reverse Midas touch." — r/investing

- "P/E 37-38 vs eBay 20. Some see low $30s." — r/ValueInvesting

- "Take-rate at 2x decade ago (21%). Squeezing sellers to mask underlying volume weakness." — r/stocks

- "200-day MA rejection after 32% bounce. P/C 2.26 bearish flow." — @SkilletHb

Insider & Institutional Activity

Headline Numbers (5-Year Aggregate)

| Metric | 5 Years | 12 Months |

|---|---|---|

| Open-Market Purchases | 0 | 0 |

| Sell Transactions | 198 | 41 |

| Total Dollar Value Sold | $313.8M | $58.5M |

| Buy/Sell Ratio | 0/198 = 0.00 | 0/41 = 0.00 |

100% selling over 5 years: $313.8M across 198 transactions from 20 insiders with zero buys. Silverman alone sold $218.5M (2,075,086 shares) — two-thirds of total insider selling. But nearly all sales were via Rule 10b5-1 mechanical trading plans (adopted August 12, 2021 & November 5, 2024) plus estate-planning trusts. This dilutes the "panic sell" signal. The pattern looks mechanical rather than informational.

Insider Ownership Roster (Current Officers & Directors)

| Insider | Current Title | Shares Owned | 5Y $ Sold |

|---|---|---|---|

| Silverman Josh | Exec Chair (former CEO) | 358,791 | $218.5M |

| Patel Goyal Kruti | CEO (since Jan 2026) | 91,565 | $9.4M |

| Baker Charles | CFO | 6,161 | $411K |

| Stretch Colin | Chief Legal Officer | 66,767 | — |

Institutional Ownership — Convertible-Arb Dominated

A critical nuance: institutional ownership stands at 120.62% — mathematically impossible except via derivative overlap. The top 10 institutional holders are dominated by convertible-arbitrage and event-driven hedge funds (D.E. Shaw +269%, Davidson Kempner +139%, Sona Asset Management +121%, Tenor Capital +104%, Soros Fund Management +86%, Calamos Advisors +71%, Camden Asset +68%, Shenkman Capital +58%) — not long-only mutual funds. This is almost certainly driven by the $650M 2019 convertible notes maturing October 1, 2026. These funds are long the convert, short the stock — which both explains the 16.54% short float and signals that the trade unwinds in October regardless of fundamentals.

Risk Factors

| Risk | Probability | Impact |

|---|---|---|

| Q1 2026 earnings miss on April 29. EPS or GMS below consensus. ETSY has missed 3 of last 6 quarters. | 30% | -$10 to -$15 |

| Core GMS returns to negative. Q4 2025 +0.1% was a one-off. 3 years of declining core GMS preceding. | 35% | -$15 to -$20 |

| Temu/Shein/Amazon marketplace share loss. Commoditization of handmade category, AI-generated listings compounding the problem. | 50% (MT) | Structural |

| Recession hits discretionary spend. Etsy is 70%+ gifts, crafts, non-essential purchases. | 30% | -20% binary |

| 2025 Notes dilution if stock > $85.79. NO capped call hedge (unique among ETSY note series). | LOW | HIGH severity |

| AI disintermediation. Flip side of ChatGPT integration — AI could cut marketplace middleman via Shopify + agents. | MEDIUM (LT) | HIGH |

| Habitual buyer decline. 5.9M buyers drive 40% of GMS; concentration risk if churn accelerates. | 40% | MEDIUM |

| UK market erosion. UK revenue -14.9% two-year. Exposure to European macro. | HIGH | LOW |

Conclusion & Price Targets

Earnings Model — FY2026E & FY2027E

| Scenario | Probability | FY26E Revenue | FY26E Op Margin | FY26E EPS | FY27E EPS | Price Target |

|---|---|---|---|---|---|---|

| BEAR — Core GMS reverts negative | 25% | $2.80B (-3%) | 9.0% | $1.50 | $1.65 | $45 |

| BASE — Q4 inflection holds, GMS +2% | 50% | $2.95B (+2%) | 12.5% | $2.30 | $2.70 | $65 |

| BULL — AI agent commerce pays off | 25% | $3.15B (+9%) | 15.0% | $3.50 | $4.20 | $90 |

| Probability-Weighted | 100% | — | — | — | — | $66.25 ≈ $65 |

Target derivation: Base-case FY27E EPS $2.70 × 18x blended forward P/E = $48.60 core equity value. Add $12/share in net cash post-Depop ($2.25B / ~92M shares) = $60.60. Add ~$4/share activist-catalyst option value (buyback acceleration + potential strategic alternatives) = $65.

Bull Case: $90 (+45%)

- Q1 2026 GMS growth +2% or better confirms Q4 inflection

- Core Etsy marketplace GMS sustains positive for 2-3 quarters

- Agentic AI partnerships drive incremental GMS >2% by YE

- $1.2B Depop cash deployed to buybacks at <$65/share

- Elliott activism escalates — strategic alternatives review

- Multiple re-rates to 22x forward P/E as profitability stabilizes

Bear Case: $45 (-27%)

- Q1 2026 earnings miss triggers second guidance cut

- Core GMS reverts negative — Q4 was a one-off

- Temu/Shein/AI commoditize handmade category further

- Habitual buyer base drops below 5.5M — concentration risk

- Take-rate ceiling hit, can't squeeze sellers further

- Multiple compresses to 12x forward P/E on growth concerns

Action Plan

| Parameter | Recommendation |

|---|---|

| Position Size | 1-2% max of portfolio given beta 1.84, short float 16.54%, and binary April 29 earnings risk. |

| Preferred Entry | Scale-in on pullback to $50-55 (below 50-day SMA, above Feb 2026 V-low of ~$45). Risk/reward improves from ~1:1 at $61.90 to ~3:1 at $52. |

| Alternative Entry | Confirmed post-earnings breakout above $75 on above-average volume if Q1 confirms the inflection. Chase only on confirmation, not hope. |

| Exit Targets | Trim at $72 (upper resistance, near 52W high). Full exit at $85 (2025 Notes conversion at $85.79 — watch dilution). Stop-loss at $45 (thesis-broken level). |

| Existing Holders | Size down to ≤2% before April 29 earnings. Sell covered calls above $70 strike (June expiry) to monetize elevated IV heading into the print. |

| Key Review Dates | Q1 2026 earnings April 29, 2026 BMO. Depop close Q2 2026. Oct 1, 2026 — $649.9M 2019 Notes mature. Dec 31, 2026 — Silverman exits Board Chair role. |

The Bottom Line

This Etsy stock analysis rates ETSY a medium-conviction HOLD at $61.90 with a 12-18 month price target of $65 (+5% upside). The core tension: Elliott Management is running the activist playbook from the boardroom, $1.2B in Depop proceeds is en route, and the stock trades at a reasonable 9.3x P/FCF. But management has destroyed $1.5B on failed M&A, core GMS just posted its first positive quarter in two years (a trend of exactly one), and the analyst consensus $61.79 target sits literally at the current price. The Street sees zero edge.

If you already own ETSY, size it to sleep through April 29 earnings — the options market is pricing in a ~10% move with IV at 148%. If you don't, wait for a pullback to $52-55 where risk/reward becomes 3:1, or wait for Q1 2026 to confirm the core marketplace inflection is real before paying up. This is not a conviction buy at current levels — it is a show-me stock.

For options traders, ETSY's high implied volatility and binary earnings setup make it a potential candidate for the Options Cafe course strategies such as selling cash-secured puts at the $50 or $52.50 strike to get paid to wait for the desired entry. Existing holders can lower their stock basis using options by selling covered calls above $70 strike. Review criteria for selecting wheel strategy stocks or explore generating monthly income with options on high-IV names like ETSY.

Sources: SEC Filings (10-K FY2025, DEF14A 2026, 8-Ks, Form 4s, Form 144s), Finviz Elite, FactSet, Reddit sentiment analysis, Twitter/X. Report compiled April 18, 2026.

Frequently Asked Questions

Is ETSY a good stock to buy right now?

Based on this Etsy stock analysis, ETSY is rated a HOLD at $61.90 with a 12-18 month price target of $65 (+5% upside). The Wall Street consensus target of $61.79 sits literally at current price, meaning the Street sees zero edge. The thesis is intact (Elliott Management activism, Depop sale, first positive core GMS in 2 years) but the setup is poor: RSI 72.5 overbought, price +17% above the 50-day SMA, and 11 days from binary Q1 2026 earnings on April 29. Better entry points are $52-55 (below the 50-day SMA) or a confirmed post-earnings breakout above $75 on volume.

What is the Etsy stock price target?

The Etsy stock price target from Wall Street consensus is $61.79 — essentially spot at current levels of $61.90. Analyst dispersion is unusually wide: Arete Sell at $43, Wells Fargo Underweight at $47, UBS Neutral $53, Stifel Hold $55, JPM $58, Morgan Stanley Equal-Weight $60, Bank of America Buy $65, Needham Buy $65, Truist Buy $83. This $40 spread signals that analysts genuinely disagree on whether this is a terminal decline or a turnaround. Our base-case 12-18 month target is $65 derived from FY27E EPS $2.70 × 18x forward P/E plus $12/share Depop cash equivalent.

Should I buy or sell ETSY stock?

The recommendation is HOLD. The setup is not compelling enough to buy aggressively here and not broken enough to sell. If you already own ETSY, size down to 1-2% of portfolio before April 29 earnings and consider selling covered calls above $70 strike (June expiry) to monetize elevated IV (currently 148%). If you don't own it, wait for a pullback to $52-55 or a confirmed breakout above $75. Sell signals: weekly close below $45 (thesis broken) or Q1 2026 earnings miss with FY2026 guidance cut.

Will Elliott Management take Etsy private?

Unlikely in the near term, but strategic alternatives pressure is possible. Elliott Management's Etsy stake sits at 5.19% with Marc Steinberg on the Board since February 5, 2024. The activist playbook has been executing at pace: $1B buyback authorized (October 2024), new CFO (November 2024), Reverb divested (April 2025), Silverman out as CEO (December 2025), $750M additional buyback (December 2025), Depop sold to eBay for $1.2B (February 2026). Combined with Impactive Capital's 3.16% and GMT Capital's ~6%, roughly 14% of the register is activist or value-conviction. A take-private bid or sale to a strategic acquirer is the tail-end bull case, but the more probable scenario is continued operational discipline plus aggressive capital return.

What is the ETSY stock forecast for 2026 and beyond?

In the base case (50% probability), ETSY reaches $65 within 12-18 months as Q4 2025 core GMS inflection holds and the $1.2B Depop cash funds accelerated buybacks. The bull case (25%) is $90 if agentic AI commerce partnerships (OpenAI ChatGPT Shopping, Google Universal Commerce Protocol) drive incremental GMS growth above 2% by year-end. The bear case (25%) is $45 if core GMS reverts to negative and Temu/Shein/AI-generated listings commoditize the handmade category further. Key catalysts: Q1 2026 earnings (April 29), Depop close (Q2 2026), October 2026 convertible notes retirement, 2027 agentic commerce revenue disclosure. The probability-weighted target is $66.25, which rounds to $65.

How does Etsy compare to eBay, Amazon, and Shopify?

ETSY is the cheapest on price-to-free-cash-flow in the peer group at 9.3x versus eBay 11x, W 12x, AMZN 30x, and SHOP 50x. On forward P/E, ETSY is 17.7x versus EBAY 11x and SHOP 55x. The most direct competitor is eBay — both are mature marketplaces with low growth and similar gross margin profiles. Shopify is a growth premium story and not a valuation comp. Amazon's multiple is inflated by AWS. Etsy's differentiation is the handmade/vintage/craft niche — a curation moat that Amazon Handmade has struggled to replicate over 10 years. But the counter-argument from Reddit value investors is persistent: Evolution AB (EVVTY) at 12x forward P/E is "actually profitable" and a better marketplace exposure, and eBay just bought Depop specifically to target Gen Z/Millennial buyers where ETSY was losing share.