GTLB Stock Analysis: Hold at $22.69 | $32 Target

Table of Contents

Executive Summary

This GitLab stock analysis covers GTLB fundamentals, technicals, SEC filings, market sentiment, and insider activity as of March 2026. I rate GTLB a HOLD with speculative accumulation below $20. Here is the bottom line:

- Extraordinary fundamental value. GTLB trades at 2.68x EV/Sales with 87% gross margins, $222M in free cash flow, $1.26B in cash, and zero debt. The enterprise value of $2.56B for a $955M revenue DevSecOps platform is buyout-grade pricing.

- The technicals are catastrophic. RSI at 28.88, death cross confirmed, 45% below the 200-day MA, trading at an all-time low of $22.69. There is a 70-75% probability the stock tests $20 before any meaningful recovery.

- Growth is decelerating sharply. FY27 guidance of 15-17% revenue growth (vs. 26% in FY25) blindsided analysts. Net retention rate has collapsed from 152% to 119%. The AI question — does it kill or supercharge DevSecOps demand — remains genuinely unresolved.

- Insiders are selling relentlessly. Founder Sijbrandij has cashed out $300M+ since IPO and continues clockwork $5M/month sales. CEO Staples' $125K purchase is the only officer buy in the entire dataset. Short interest has surged 4x to 8.89%.

- The $400M buyback provides a floor. Authorized March 2, 2026, it could retire 11.5% of shares at current prices — the first net anti-dilution event in GTLB's history. But SBC of $170M/year consumes most of the benefit.

| Report | Signal | Key Finding | Score |

|---|---|---|---|

| Fundamentals | BULLISH | $955M revenue, 87% GM, $222M FCF, $1.26B cash, zero debt. EV/Sales 2.68x is absurdly cheap vs. 7-9x peers. | 8/10 |

| Technicals | BEARISH | RSI 28.88 (oversold). Death cross. 45% below 200-day MA. At all-time low. 8 of 10 days red. | 2/10 |

| SEC Filings | MIXED | Revenue 9.3x in 5 years, fortress balance sheet. But SBC 24% of revenue, extreme C-suite turnover, securities litigation. | 5/10 |

| News & Events | MIXED | 82 articles evenly split. Q4 beat overshadowed by FY27 guidance shock. Multiple analyst downgrades. TCS partnership positive. | 5/10 |

| Sentiment | MIXED | Forgotten on Reddit (zero WSB chatter). Twitter cautiously bullish contrarian. Acquisition thesis gaining traction. | 5/10 |

| Insider Activity | BEARISH | Founder clockwork selling $300M+ cumulative. Only 1 officer purchase ($125K). Short interest up 4x. Eminence/Atreides accumulating. | 3/10 |

| COMPOSITE | HOLD | Exceptional fundamental value offset by devastating technicals and bearish insider activity. A classic fundamental/technical divergence. | 4.7/10 |

Investment Thesis

GitLab sits at the intersection of extraordinary fundamental value and catastrophic technical destruction. On pure numbers, this is a $955M revenue business with 87% gross margins, $222M in free cash flow, $1.26B in cash, zero debt, and an enterprise value of just $2.56B — representing 2.68x EV/Sales and 17x P/FCF. Those are buyout-grade multiples for a high-margin SaaS platform serving 50%+ of the Fortune 100.

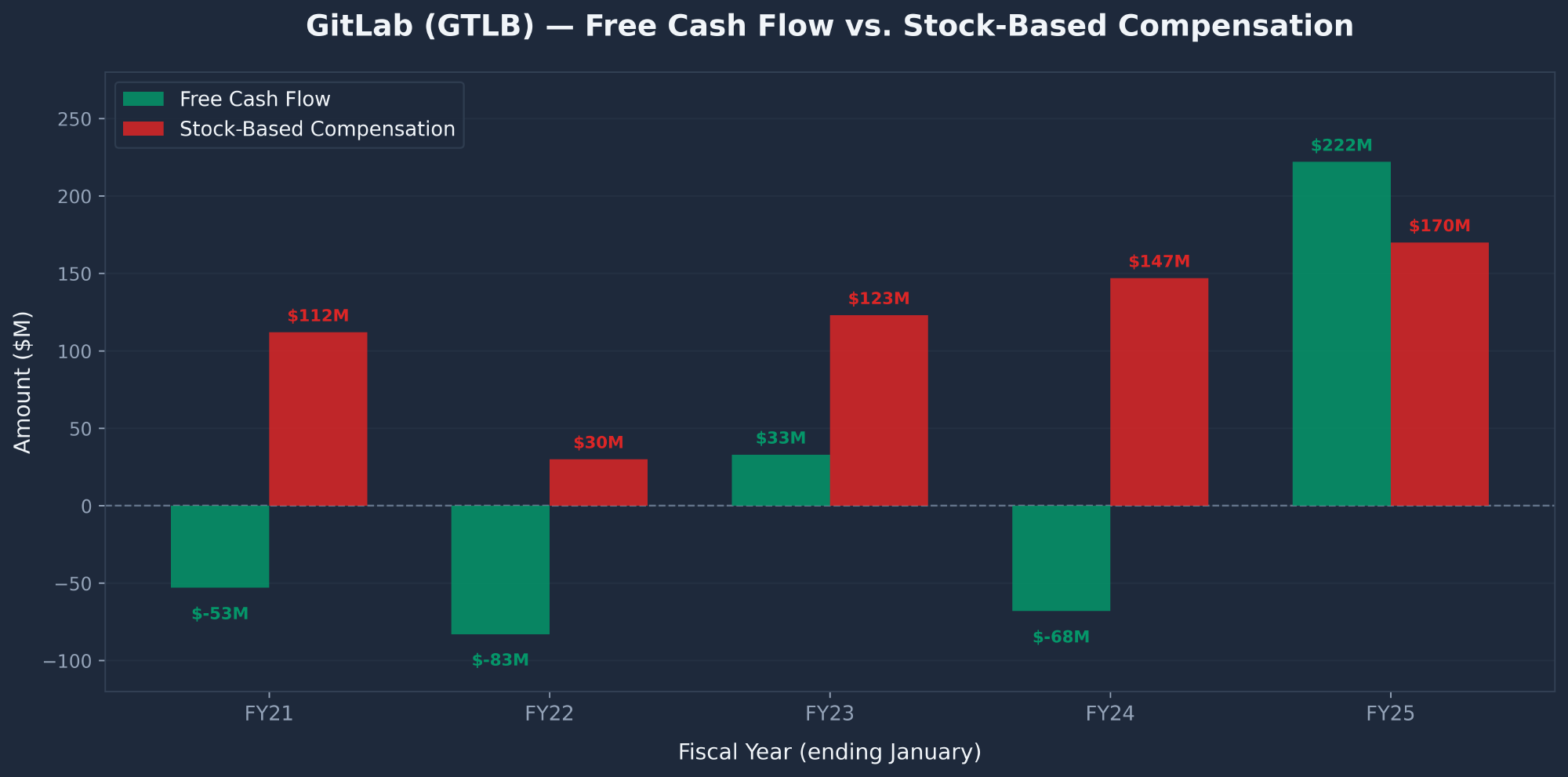

The bear case is equally compelling. Growth is decelerating fast: FY27 guidance of 15-17% was a dramatic step down from 26% in FY25, blindsiding analysts expecting 22-24%. Net retention rate has collapsed from 152% to 119%, signaling that expansion within existing customers is slowing materially. Stock-based compensation of $170M/year consumes 77% of free cash flow, making the "cash machine" argument weaker than it appears.

The right move is a small starter position (1-2% of portfolio) at current levels with a plan to add aggressively in the $18-20 range. The Q1 FY27 earnings report (June 2026) is the binary event that will either validate the value thesis or confirm the value trap. At $20, you would be paying ~$1.8B EV for a business generating $222M in FCF (8x P/FCF) with $1.26B in cash backing — that is PE buyout territory. For more on how I approach asymmetric setups like this, see the strategies I discuss on this website.

Fundamental Analysis

Company Overview

GitLab Inc. (NASDAQ: GTLB) is the leading DevSecOps platform providing a single application for the entire software development lifecycle: planning, source code management, CI/CD, security testing, packaging, deployment, and monitoring. Founded in 2011 by Sid Sijbrandij and Dmitriy Zaporozhets, GitLab went public on October 14, 2021 at $77/share. The company operates as a fully remote organization with approximately 2,375 employees and zero office space.

GitLab competes primarily against GitHub (owned by Microsoft), Atlassian (Jira/Bitbucket), and JFrog. Its key differentiator is the single-platform approach versus competitors' point solutions, plus the ability for enterprises to self-host the platform — critical for government and regulated industries. GitLab Duo, the company's AI-powered coding assistant, represents the next frontier for monetization through the Duo Agent Platform.

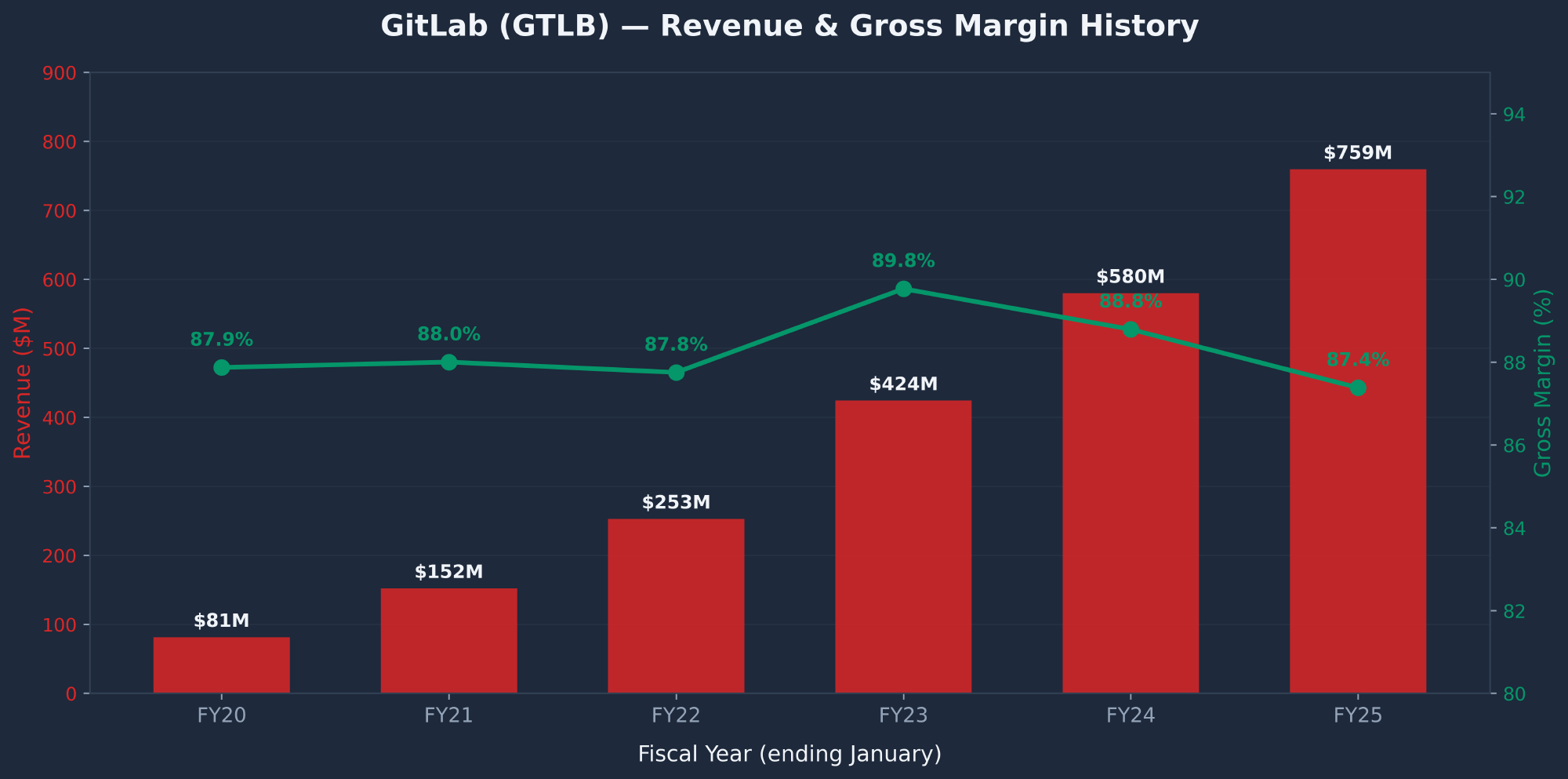

Revenue & Gross Margin History

| Metric ($M) | FY25 | FY24 | FY23 | FY22 | FY21 | FY20 |

|---|---|---|---|---|---|---|

| Revenue | 759 | 580 | 424 | 253 | 152 | 81 |

| Revenue Growth | +31% | +37% | +68% | +66% | +87% | — |

| Gross Profit | 835 | 674 | 521 | 372 | 222 | 134 |

| Gross Margin | 87.4% | 88.8% | 89.8% | 87.8% | 88.0% | 87.9% |

| Operating Income | (67) | (136) | (179) | (212) | (128) | (214) |

| Operating Margin | -7.1% | -17.9% | -30.9% | -50.0% | -50.8% | -140.6% |

| Free Cash Flow | 222 | (68) | 33 | (83) | (53) | — |

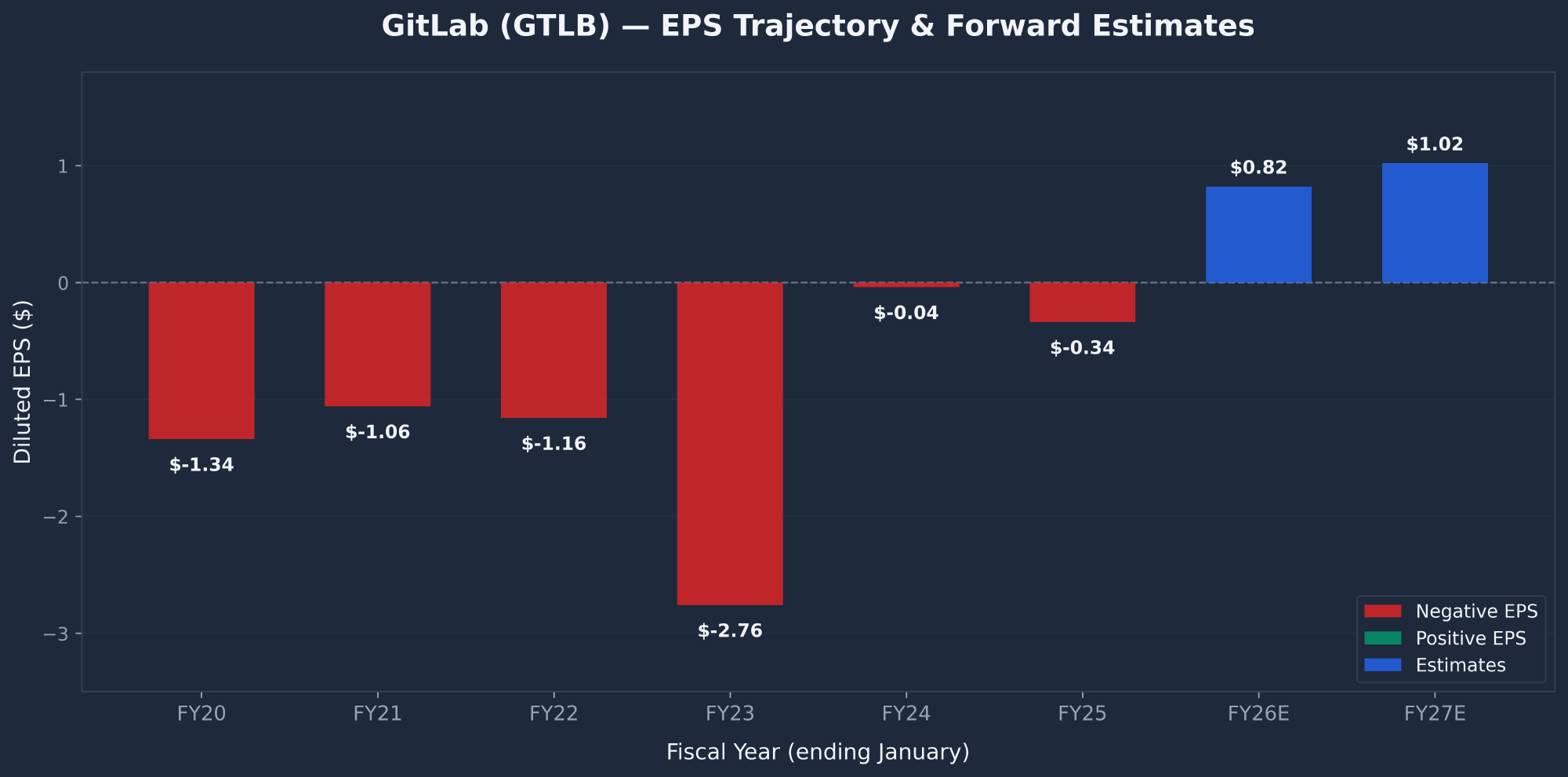

EPS Trajectory

GitLab is approaching a major inflection point: GAAP profitability. Forward EPS consensus of $1.02 implies the company will cross into the black in FY27. Non-GAAP operating income was already positive in FY25 at ~10% margin. However, the key caveat is that non-GAAP profitability depends entirely on excluding $170M+ in stock-based compensation — GitLab still loses money on a GAAP basis when SBC is included.

Valuation Snapshot

| Metric | GTLB | TEAM (Atlassian) | Peer Median |

|---|---|---|---|

| EV/Sales (Fwd) | 2.3x | ~7.5x | ~7-9x |

| P/FCF | 17x | ~35x | ~30-40x |

| Forward P/E | ~22x | ~45x | ~35-50x |

| Gross Margin | 87% | ~83% | ~75-83% |

| Revenue Growth | 15-17% (guided) | ~15-18% | ~18-25% |

| Cash/Share | $7.57 (33% of price) | ~$6.50 | — |

| Debt | $0 (ZERO) | ~$1.1B | — |

Free Cash Flow vs. Stock-Based Compensation

Customer Metrics & Net Retention

| Metric | Q3 FY26 | FY25 | FY24 | FY23 | FY22 |

|---|---|---|---|---|---|

| $100K+ ARR Customers | 1,405 | 1,229 | 955 | 697 | 492 |

| $1M+ ARR Customers | — | 123 | 96 | 63 | — |

| Dollar-Based Net Retention | 119% | 123% | 130% | >130% | >152% |

| Base Customers (>$5K ARR) | 10,475 | 9,893 | 8,602 | 7,002 | — |

Technical Analysis

GTLB's technical picture is unequivocally bearish across every timeframe and every indicator. The stock sits at its all-time low of $22.69, down 73.6% from the ATH of ~$86 and 69.4% from the January 2025 high of $74.18. All moving averages are stacked bearishly (Price < SMA10 < SMA50 < SMA200) with each MA declining — a full death cross confirmation.

| Indicator | Value | Signal |

|---|---|---|

| SMA 10 | $24.47 | BEARISH (-7.3%) |

| SMA 20 | $25.80 | BEARISH (-12.0%) |

| SMA 50 | $31.17 | BEARISH (-27.2%) |

| SMA 200 | $41.23 | BEARISH (-45.0%) |

| RSI (14) | 28.88 | OVERSOLD |

| MACD | -2.39 / Signal: -2.35 | BEARISH (crossover failed) |

| Beta | 0.82 | NEUTRAL |

| ATR (14) | $1.71 (7.5%) | ELEVATED |

Support & Resistance

| Level | Price | Significance |

|---|---|---|

| Support 1 | $22.66 | ALL-TIME LOW (hit Mar 13). Final line of defense. Break below = no historical floor. |

| Support 2 | $20.00 | Psychological round number. No historical support — below IPO range. |

| Resistance 1 | $24.47 | SMA 10. First hurdle for any bounce to have legs. |

| Resistance 2 | $26-28 | Prior 2022 crash low zone. Now dense overhead resistance. |

| Resistance 3 | $31.17 | SMA 50. Major confluence resistance zone. |

Technical bottom line: I assign a 70-75% probability that GTLB tests $20 before any meaningful recovery. Every Fibonacci retracement level from the Jan 2025 high ($74.18) has been broken. The stock is in uncharted territory with no structural floor. The only marginally bullish signal is the oversold RSI at 28.88, but in a strong downtrend RSI can remain oversold for weeks. Watch for RSI divergence as the first sign of exhaustion.

SEC Filings Deep Dive

I analyzed 60 SEC filings spanning 4x 10-K, 13x 10-Q, 34x 8-K, 4x DEF 14A, and the original S-1. GitLab grew revenue 9.3x in 5 years (from $81M in FY2020 to $759M in FY2025), with subscription revenue consistently representing 87-91% of total revenue.

Management Turnover — Red Flag

GitLab has experienced unprecedented C-suite turnover in the last 18 months:

| Date | Event | Details |

|---|---|---|

| Jul 2023 | CRO Departed | Michael McBride out. Chris Weber (from UiPath) hired. |

| Aug 2024 | CRO Departed Again | Chris Weber out after 13 months. Ashley Kramer (CMO) named interim CRO. |

| Dec 2024 | CEO Transition | Sid Sijbrandij resigned (health: osteosarcoma). Bill Staples appointed CEO ($38.9M package). |

| Sep 2025 | CFO Departed | Brian Robins resigned. Jessica Ross hired (from Frontdoor/Salesforce). |

| Jan 2026 | CTO Departed | Sabrina Farmer resigned. Sivaprasad Padisetty hired (from New Relic/Amazon). |

Kilo Code ROFR — Hidden Wildcard

Securities Litigation

The Dolly v. GitLab class action (filed September 2024) covers June 5, 2023 to June 3, 2024, alleging misrepresentations about AI monetization and feature adoption. Two derivative suits (Preciado and Jones) followed in February 2025. GitLab planned to file a motion to dismiss. Most ambulance-chaser suits settle or dismiss, but this creates an overhang on the stock.

Dual-Class Structure

GitLab maintains a dual-class share structure: Class A (1 vote) and Class B (10 votes). With ~19.5M Class B shares outstanding, Sid Sijbrandij retains approximately 57% of total voting power despite owning only ~12% of economic interest. No deal happens without his consent, which complicates any potential acquisition scenario.

News & Catalysts

The news flow for GTLB stock is evenly split across 82 articles, with the FY27 guidance shock dominating recent coverage. Multiple analyst downgrades from Morgan Stanley, Wells Fargo, Piper Sandler, and Truist have pressured the stock, while the TCS partnership and $400M buyback authorization provide bullish counterpoints.

Analyst Ratings

| Firm | Rating | Target | Upside |

|---|---|---|---|

| Guggenheim | Buy | $70 | +209% |

| BTIG | Buy | $52 | +129% |

| Morgan Stanley | Equal Weight | $29 | +28% |

| TD Cowen | Hold | $29 | +28% |

| Piper Sandler | Neutral | $28 | +23% |

| Barclays | Underweight | $34 | +50% |

Consensus target: $34.20 (+51% upside). Even the bears have targets above the current price, which underscores the extreme nature of this sell-off.

Catalyst Timeline

| Timing | Catalyst | Direction |

|---|---|---|

| Mar-May 2026 | $400M buyback execution begins. Pace of repurchases will signal management conviction. | Bullish Floor |

| Jun 2026 | Q1 FY27 Earnings — THE make-or-break event. First data point on whether 15-17% guidance is conservative or realistic. | Binary |

| Aug 2026 | Kilo Code ROFR deadline (Aug 24). Does GitLab exercise its right on Sid's AI company? | Wildcard |

| Ongoing | Duo Agent Platform adoption. Any disclosure of Duo ARR or customer count would be a major positive catalyst. | Bullish (if disclosed) |

Market Sentiment

GTLB is essentially a "forgotten stock" on social media. Reddit activity is VERY LOW — zero mentions on WallStreetBets in the last 7 days, minimal discussion on r/stocks and r/investing. This "forgotten" status can paradoxically be contrarian bullish: maximum pessimism is often when value investors find opportunity.

Dominant Narratives

| Narrative | Details |

|---|---|

| FY27 Guidance Shock | 15-17% growth guidance blindsided analysts expecting 22-24%. Non-CRPO growth collapsed to just 3%, raising pipeline fears. |

| AI: Friend or Foe? | The central debate: more AI code = more GitLab (bullish) vs. fewer developers = fewer seats (bearish). Duo Agent is early-stage and unproven. |

| Deep Value vs. Value Trap | At 2.7x EV/Sales with $1.2B cash, GTLB screens as deep value. But SBC consuming 77% of FCF and relentless insider selling keep the "value trap" argument alive. |

| M&A Target | $2.56B EV for $955M revenue, 87% GM, $222M FCF, zero debt, Fortune 100 customers. Classic PE buyout candidate. But dual-class structure complicates. |

The media tone skews cautiously bullish: Motley Fool has been relentlessly optimistic, while Investing.com argues the selloff is overdone. Analyst downgrades from the major banks provide the bearish counterpoint.

Insider & Institutional Activity

Founder Sijbrandij — Clockwork Seller

Sytse Sijbrandij sells on a precise 10b5-1 schedule: monthly conversions of 54,300-108,600 Class B shares to Class A, then immediate sale. He still holds ~15.25M Class B shares (supervoting).

| Period | Amount Sold | Notes |

|---|---|---|

| IPO (Oct 2021) | $192.5M | IPO sell-down |

| Dec 2023 | ~$89M | Large block sale |

| Mar 2024 – Present | ~$5M/month | Steady monthly 10b5-1 sales (54,300-108,600 shares) |

Institutional Activity

Institutional ownership is 78.42% with net transactions at +0.20%. GV (Google Ventures) accumulated ~$75M in shares during 2022-2023. More recently, Eminence Capital increased its position by 15.9% and Atreides Management by 38.9% — providing countervailing demand against the insider selling.

CEO Bill Staples made the only officer open-market purchase in the dataset: 3,276 shares at $38.08 ($124,750) on December 31, 2025. Symbolically important but small relative to company scale.

Risk Factors

| Risk | Probability | Impact | Details |

|---|---|---|---|

| AI Seat Compression | Medium | HIGH | If AI reduces developer headcount, per-seat pricing shrinks. Hybrid pricing pivot is an admission of this risk. |

| Growth Deceleration | High | HIGH | FY27 guidance of 15-17% is a sharp step down. NRR falling from 152% to 119%. Non-CRPO growth at 3%. |

| GitHub/Microsoft Competition | High | MEDIUM | GitHub has 100M+ developers, Copilot at $2B+ ARR, deep Azure integration. GitLab is the smaller player vs. a tech giant. |

| SBC Dilution | Certain | MEDIUM | $170M/yr SBC = ~5.6% annual dilution. Buyback partially offsets but does not eliminate the drag. |

| Management Turnover | Materialized | MEDIUM | CEO, CFO, CRO (2x), CTO all departed in 18 months. New team untested. Execution uncertainty elevated. |

| Securities Litigation | Low | LOW | Dolly v. GitLab class action + 2 derivative suits. Creates overhang but most likely settles for immaterial amount. |

| Founder Selling | Certain | MEDIUM | Sid continues $5M/month selling even at depressed prices. Erodes confidence in "deep value" narrative. |

Conclusion & Price Targets

Earnings Model — FY27 (Ending Jan 2027)

| Metric | Bear Case | Base Case | Bull Case |

|---|---|---|---|

| FY27 Revenue | $1.08B (+13%) | $1.11B (+16%) | $1.15B (+20%) |

| Gross Margin | 86% | 87% | 88% |

| Non-GAAP EPS | $0.72 | $0.82 | $1.05 |

| Free Cash Flow | $210M | $250M | $290M |

Price Target Framework

Bull Case ($40-$50)

- Duo Agent Platform adoption accelerates

- FY27 guidance proves conservative (beat-and-raise)

- AI narrative flips from threat to tailwind

- PE/strategic acquisition bid at 5x+ EV/Sales

- Re-rate to peer multiples

Probability: 20%

Bear Case ($16-$18)

- Growth decelerates below 15%

- NRR falls under 110%

- AI seat destruction thesis confirmed

- Class action settlement

- Stock trades to 2x EV/Sales

Probability: 30%

Probability-weighted 12-month price: (0.30 x $17) + (0.45 x $31) + (0.20 x $45) + (0.05 x $33.50) = $29.73 (+31%). The expected value is positive, but the wide outcome range and 30% bear case probability justify HOLD rather than aggressive BUY.

Position Sizing

| Approach | Details |

|---|---|

| Starter Position | 1-2% portfolio allocation at current levels ($22-23). This is "watching money" to track the position. |

| Add Zone | $18-20 range. Increase to 3-4% portfolio. At $20, EV drops to $1.8B (1.9x EV/Sales), P/FCF to 13x. PE buyout pricing. |

| Full Position | Only after Q1 FY27 earnings (June 2026) confirms growth trajectory and NRR stabilization. Scale to 4-5% if beat-and-raise. |

| Mental Stop | $15 (-34%). At that price, the market is pricing in existential AI disruption and you need to reassess the thesis entirely. |

If you're interested in how I use options strategies to manage risk in high-conviction setups, check out my guide on mastering the wheel strategy and how to lower your stock basis using options. Selling cash-secured puts at the $18-20 strike could be an attractive way to get paid while waiting for a better entry. Learn more about that approach in my cash-secured puts guide.

Frequently Asked Questions

Is GTLB a good stock to buy?

GTLB stock presents a compelling value case at $22.69 with 87% gross margins, $1.26B cash, zero debt, and 2.7x EV/Sales — far below the 7-9x peer average. However, the technicals are catastrophic (all-time low, death cross, RSI oversold) and growth is decelerating sharply (26% to 15-17%). I rate it a HOLD with speculative accumulation below $20 for patient investors willing to accept the AI disruption uncertainty and wait for the Q1 FY27 earnings catalyst in June 2026.

What is the GTLB price target for 2026?

My probability-weighted 12-month GTLB stock price target is $29.73, representing +31% upside from $22.69. The base case target is $28-$34 (45% probability), with a bull case of $40-$50 (20% probability) and a bear case of $16-$18 (30% probability). Consensus analyst target is $34.20. The key variable is Q1 FY27 earnings in June 2026 — a beat-and-raise could push the stock to $35+ rapidly, while a miss could confirm the value trap and send it to $18.

Should I buy or sell GTLB?

If you already own GTLB stock, hold your position — selling at the all-time low after a 73% decline locks in maximum losses. If you do not own it, consider a small starter position (1-2% of portfolio) at current levels with a plan to add aggressively in the $18-20 range. The risk/reward is asymmetric (41% upside to $32 target vs. 21% downside to $18 risk), but the technical picture demands patience. Do not commit a full position until the Q1 FY27 earnings report provides clarity on the growth trajectory.

GTLB stock forecast for 2026 and beyond?

GitLab's long-term outlook depends on whether AI proves additive or destructive to the DevSecOps market. In the bull scenario, more AI-generated code drives more demand for GitLab's pipeline, security, and deployment tools — the platform is tool-agnostic and benefits regardless of who writes the code. If this narrative takes hold, GTLB could re-rate to $50+ (5x EV/Sales) by 2027. In the bear scenario, AI reduces developer headcount, shrinking the addressable market, and growth decelerates to single digits — sending the stock to $15-18. The $400M buyback, fortress balance sheet ($1.26B cash, zero debt), and approaching GAAP profitability provide a floor, but the dual-class structure and relentless insider selling create governance headwinds. This is a show-me story with genuinely asymmetric potential in both directions.

Sources: SEC Filings (10-K, 10-Q, 8-K, DEF 14A, S-1), Finviz, Polygon.io, Google News, Reddit, Twitter/X, Motley Fool, Investing.com, GlobeNewswire. Report compiled March 15, 2026.