IONQ (IonQ) Stock Analysis: Hold at $33 | $34 Target

Table of Contents

Executive Summary

This IonQ stock analysis covers IONQ's fundamentals, technicals, SEC filings, market sentiment, and insider activity as of March 2026. Here is the bottom line:

- HOLD — do not initiate at $32.98. The probability-weighted 12-month target is $34 (+3%), grossly insufficient risk compensation when the bear case implies -70%. The risk/reward is unfavorable at 0.5:1.

- Revenue growth is genuinely impressive: $0 to $130M in 5 years, with Q4 FY2025 at $61.9M (+429% YoY). IonQ is the first quantum computing company to surpass $100M in annual revenue. FY2026 guidance of $225–$245M crushed Street estimates of ~$190M.

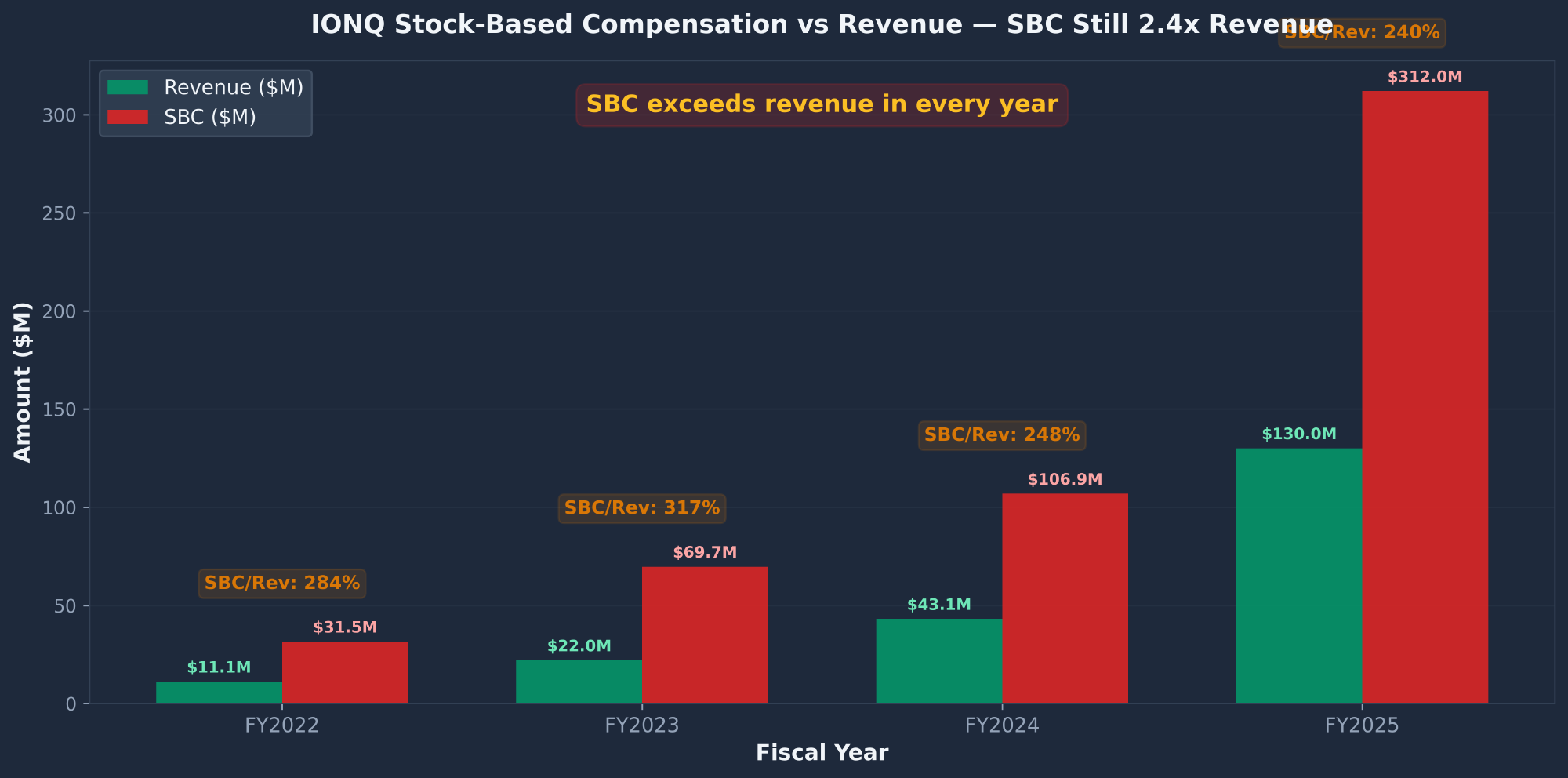

- The valuation is extreme. At 93x trailing P/S with -22.67% gross margins, the stock prices in a future that may be 5–15 years away. Stock-based compensation of $312M represents 240% of revenue — the company pays its employees 2.4x what it earns from customers.

- Insider selling is alarming. Founder Peter Chapman and CEO Niccolo de Masi executed coordinated exits totaling $335M within 2 days of each other. The sell-to-buy dollar ratio across all insiders is 117:1.

- Short interest has doubled to 24.04% (85.9M shares) since the Wolfpack Research short report in February 2026, which alleged 86% of 2022–2024 revenue came from canceled Pentagon earmarks.

| Report | Signal | Key Finding |

|---|---|---|

| Revenue Growth | BULLISH | $130M (+202%), Q4 +429%, guidance $225-245M vs Street $190M, RPO $370M (+380%) |

| Valuation | BEARISH | 93x P/S trailing, negative gross margins, 240% SBC/revenue ratio |

| Technical | BEARISH | -61% from ATH, below all MAs, death cross imminent, RSI 40 |

| Insider Trading | BEARISH | $335M coordinated exits (founder+CEO), 117:1 sell-to-buy ratio, 85 sells vs 3 buys |

| SEC Filings | BEARISH | $1.96B goodwill (likely impaired), 63% dilution in 1 year, $2.47B warrant liabilities, 9 acquisitions in 13 months |

| Sentiment | NEUTRAL | Score 4.5/10. Reddit 55% bearish. Wolfpack thesis intensely debated. WSB activity high. |

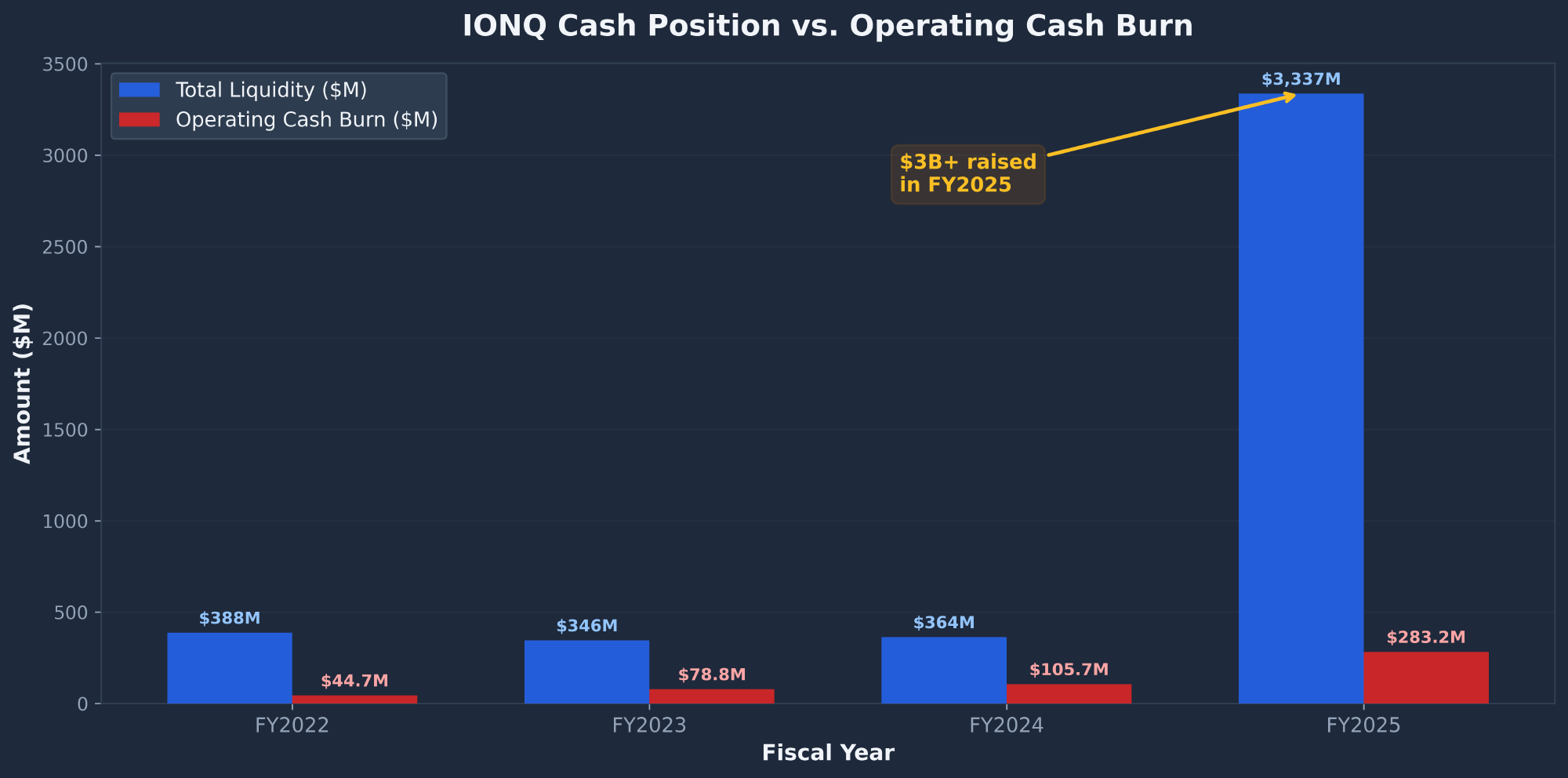

| Balance Sheet | BULLISH | $3.3B cash, zero debt, 15.5x current ratio, 11+ years runway at current burn |

| COMPOSITE | HOLD | 75% bearish signals, 15% bullish, 10% neutral. Revenue growth is real but doesn't justify the valuation. |

Investment Thesis

IonQ is the purest-play public quantum computing stock and the first quantum company to cross $100M in annual revenue. Its trapped-ion technology achieves industry-leading 99.99% two-qubit gate fidelity, operates near room temperature (no cryogenic cooling), and costs ~$30M per system versus ~$1B for superconducting competitors. The Q4 FY2025 earnings blowout ($61.9M revenue, +429% YoY, 55% above estimates) and FY2026 guidance of $225–245M confirm that IonQ is building a real business in a nascent industry.

The insider selling is the single most concerning signal. Founder Peter Chapman sold ~6M shares for $230M and CEO de Masi sold his entire indirect position for $105M — both via 10b5-1 plans adopted within 2 days of each other. When the people who know the technology best are liquidating at scale, it demands attention.

I assign 45% probability to the base case ($30 target), 25% to the bull case ($68), and 30% to the bear case ($10). The probability-weighted target of $34 offers only +3% upside — insufficient compensation for a stock with 2.76 beta and $2.81 daily ATR (8.5% swings). Wait for $20–22 or proof of positive gross margins before buying.

Fundamental Analysis

Company Overview

IonQ, Inc. (NYSE: IONQ) is a quantum computing company headquartered in College Park, Maryland with 1,132 employees. Founded by Duke University professors Christopher Monroe and Jungsang Kim, IonQ went public via SPAC merger in January 2021. The company provides quantum computing as a service (QCaaS) through Amazon Braket, Microsoft Azure Quantum, and Google Cloud, plus direct enterprise and government contracts.

IonQ completed 9 acquisitions in 13 months during FY2025, including Oxford Ionics ($1.59B), Capella Space ($425M), ID Quantique ($116M), and Vector Atomic ($182M). The pending $1.8B SkyWater Technology acquisition would give IonQ its own semiconductor foundry for vertical integration.

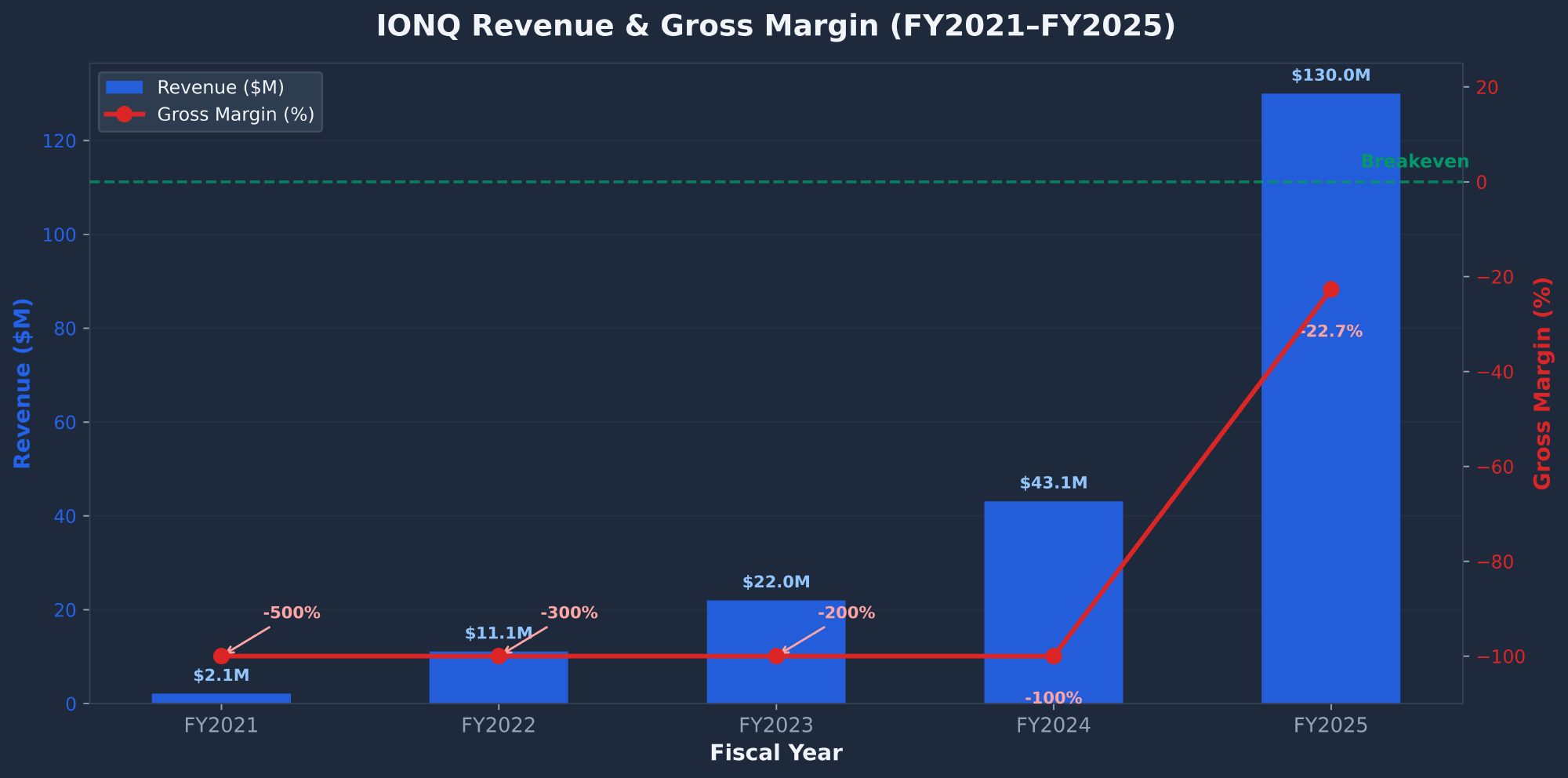

Revenue & Margin History

| Metric | FY2025 | FY2024 | FY2023 | FY2022 |

|---|---|---|---|---|

| Revenue ($M) | 130.0 | 43.1 | 22.0 | 11.1 |

| Revenue Growth | +202% | +96% | +98% | +57% |

| Gross Margin | -22.67% | Deep neg. | Deep neg. | Deep neg. |

| Net Loss ($M) | (512) | (332) | (201) | (157) |

| SBC ($M) | 312 | 107 | 70 | 32 |

| SBC / Revenue | 240% | 248% | 317% | 284% |

| RPO ($M) | 370 | 77 | — | — |

SBC vs Revenue

Cash Position

Peer Comparison

| Metric | IONQ ($32.98) | RGTI ($16.17) | QBTS ($17.55) |

|---|---|---|---|

| Revenue (TTM) | $130M | ~$13M | ~$25M |

| P/S (TTM) | 93x | ~440x | ~280x |

| Technology | Trapped-ion | Superconducting | Quantum annealing |

| Cash | $3.3B | ~$700M | ~$900M |

| Short Interest | 24.04% | ~20% | ~12% |

Technical Analysis

IONQ is in a clear downtrend, trading 61% below its $84.64 ATH and below all major moving averages. A death cross (SMA 50 crossing below SMA 200) is imminent within 2–4 weeks. The only bullish technical signal is a fading MACD crossover from early March. Beta of 2.76 means this stock moves nearly 3x the market.

| Indicator | Value | Signal |

|---|---|---|

| SMA 50 | $40.27 | BEARISH (-18.1%) |

| SMA 200 | $47.44 | BEARISH (-30.5%) |

| RSI (14) | 40.12 | NEUTRAL-WEAK |

| MACD | -1.36 / Signal: -1.47 | FADING (crossover exhausting) |

| Beta | 2.76 | EXTREME VOLATILITY |

| ATR (14) | $2.81 (8.5%) | EXTREME |

Key levels: Support at $30 (psychological), $25–26 (Jan crash low), $17.88 (52-week low). Resistance at $35.55 (SMA 10), $40.27 (SMA 50), $47.44 (SMA 200).

SEC Filings Deep Dive

I analyzed 94 SEC filings. The two most concerning findings: $1.96B in goodwill from acquisitions paid with stock at $55–$93/share (stock now at $33 — likely impaired), and $2.47B in warrant liabilities creating massive earnings volatility.

The revenue composition is notable: Quantum Hardware was $69.9M (54%) and Platform/Consulting/Support was $60.1M (46%) in FY2025. International revenue grew from 5% to 33%, driven by the ID Quantique acquisition in Switzerland and the Romania quantum key distribution network deployment.

News & Catalysts

Analyst Ratings

| Firm | Rating | Target | Upside |

|---|---|---|---|

| Jefferies | Buy | $100 | +203% |

| Mizuho | Outperform | $90 | +173% |

| Needham | Buy | $80 | +143% |

| Wedbush | Outperform | $60 | +82% |

| JP Morgan | Neutral | $47 | +43% |

Consensus target: $67 (+103%). The stock trades 51% below even the lowest analyst target ($47). Analyst consensus is "Strong Buy" (1.40 rating) — a striking disconnect with the 75% bearish signal composite.

Key Events Timeline

| Date | Event | Impact |

|---|---|---|

| Jan 6, 2025 | Jensen Huang "15–30 years" comment | -46% in one week. 248M shares traded. |

| Feb 4, 2026 | Wolfpack Research short report | -14%. Alleges 86% of revenue from canceled Pentagon earmarks. |

| Feb 26, 2026 | Q4 earnings blowout | +21%. Revenue $61.9M (+429%), beat by 55%. Guidance $225-245M. |

| Mar 11, 2026 | Cambridge 256-qubit partnership | BofA calls it the "next fire moment." Major tech milestone. |

Market Sentiment

Sentiment scores 4.5/10 — mixed-to-bearish. Reddit is 55% bearish / 35% bullish, with WSB activity high. The Wolfpack short thesis is extensively debated. The dominant refrain on r/stocks: "Incredible growth but insane valuation." Multiple commenters cite the CEO selling $290M+ as "the single most damning data point for retail bulls."

Insider & Institutional Activity

Founder Peter Chapman sold ~6M shares for $230M via a 10b5-1 plan adopted March 14, 2025. CEO de Masi sold his entire indirect position (2.6M shares) for $105M via a 10b5-1 plan adopted March 12, 2025 — two days before Chapman's. The coordination is striking. The only meaningful buy: Director Scannell purchased $2M at $21.81 (now up 51%).

Risk Factors

| Risk | Probability | Impact |

|---|---|---|

| Quantum timeline extends beyond 2030. Useful quantum computing may be decades away. | 60% | -50 to -70% |

| Big tech breakthrough obsoletes trapped-ion. Google, IBM, Microsoft have $175B+ combined capex. | 30% | -80%+ |

| Wolfpack thesis validated. Government contract dependency confirmed; 86% earmark revenue allegation. | 35% | -40 to -60% |

| Goodwill impairment. $1.96B at risk. Acquisitions paid at $55-93/share; stock at $33. | 30% | -15 to -25% |

| SkyWater acquisition failure. $1.8B deal pending; integration of a foundry is complex. | 25% | -25 to -40% |

| Continued dilution. 63% dilution in FY2025. SBC at 240% of revenue. 79M warrants outstanding. | 70% | -10 to -20% annually |

Conclusion & Price Targets

| Scenario | Prob. | FY27 Rev | Gross Margin | Target P/S | 12-Mo Target | Return |

|---|---|---|---|---|---|---|

| Bull | 25% | $520M | +18% | 50x | $68 | +106% |

| Base | 45% | $380M | +5% | 30x | $30 | -9% |

| Bear | 30% | $260M | -15% | 15x | $10 | -70% |

| Probability-Weighted Target | $34 | +3% | ||||

Bull Case ($68)

- Revenue exceeds $280M in FY2026, $520M by FY2027

- Gross margins flip positive as quantum hardware scales

- SkyWater vertical integration reduces system costs

- Cambridge 256-qubit system validated; defense contracts expand

- Short squeeze: 24% SI, 4 days to cover, 85.9M shares

Bear Case ($10)

- Quantum timeline extends; commercial advantage years away

- Wolfpack thesis confirmed; government revenue at risk

- $1.96B goodwill impairment triggered

- $335M insider exits signal lack of confidence

- Big tech (Google/IBM/MSFT) breakthrough obsoletes trapped-ion

- Continued dilution: 63% in FY2025, SBC at 240% of revenue

Action Plan

| If You... | Action |

|---|---|

| Have no position | Do not initiate. Wait for $20–22 or two quarters of positive gross margins. |

| Already own shares | Hold with a hard stop at $25. Q1 2026 earnings (May) is the next major test. |

| Want to speculate | Consider selling cash-secured puts at the $20 strike to collect premium while waiting for a better entry. |

For options income strategies on volatile quantum computing stocks, see the wheel strategy guide or learn how to lower your stock basis using options. For contrasting analyses, see the STX (Seagate) analysis or the RIVN (Rivian) analysis.

Frequently Asked Questions

Is IONQ a good stock to buy?

IONQ is a Hold, not a Buy, at $32.98. While IonQ has genuine revenue growth ($130M, +202% YoY) and is the leading pure-play quantum computing stock, the 93x trailing P/S ratio with negative gross margins (-22.67%) and $312M in annual stock-based compensation (240% of revenue) make the current price unjustifiable on fundamentals. The $335M coordinated insider selling by the founder and CEO is a significant red flag. Wait for $20–22 or proof of positive gross margins for two consecutive quarters before buying.

What is the IONQ price target for 2026?

The analyst consensus IONQ price target is $67 (+103% upside), ranging from $47 (JP Morgan) to $100 (Jefferies). My probability-weighted target is $34 based on three scenarios: bull $68 (25% probability), base $30 (45%), and bear $10 (30%). The wide analyst range reflects deep uncertainty about quantum computing timelines and IonQ's ability to convert its technology lead into profitable operations.

Should I buy or sell IONQ?

Neither — hold if you own it (with a $25 stop), avoid buying at current prices. The risk/reward is unfavorable at 0.5:1 (+3% upside vs -70% bear case). The stock would become attractive below $20–22, which would provide a 40%+ margin of safety. If you want speculative quantum computing exposure, selling cash-secured puts at the $20 strike lets you collect premium while waiting for a better entry.

IONQ stock forecast for 2026 and beyond?

IONQ's near-term trajectory depends on execution against FY2026 guidance of $225–245M. The first test is Q1 2026 earnings (May 2026). Longer-term, consensus estimates project $380–520M by FY2027 and $570–850M by FY2028, with first profitability unlikely before FY2029–2030. The quantum computing TAM is projected at $50–100B+ by 2035, and IonQ's trapped-ion technology positions it well — but Google's Willow chip, Microsoft's Majorana 1, and IBM's $1B+ quantum revenue demonstrate that big tech competition is intensifying rapidly.

Sources: SEC Filings (10-K, 10-Q, 8-K, DEF 14A), Finviz, Polygon.io, Google News, Reddit, Twitter/X, Wolfpack Research. Report compiled March 16, 2026.