META (Meta) Stock Analysis: Buy at $612 | $750 Target

Table of Contents

Executive Summary

This META stock analysis covers Meta Platforms' fundamentals, technicals, SEC filings, market sentiment, and insider activity as of April 8, 2026. The full Meta Platforms stock analysis below is built on the FY2025 10-K, 900 parsed insider transactions across five years, a Reddit and Twitter sentiment sweep, and 164 articles from the past 30 days. Bottom line:

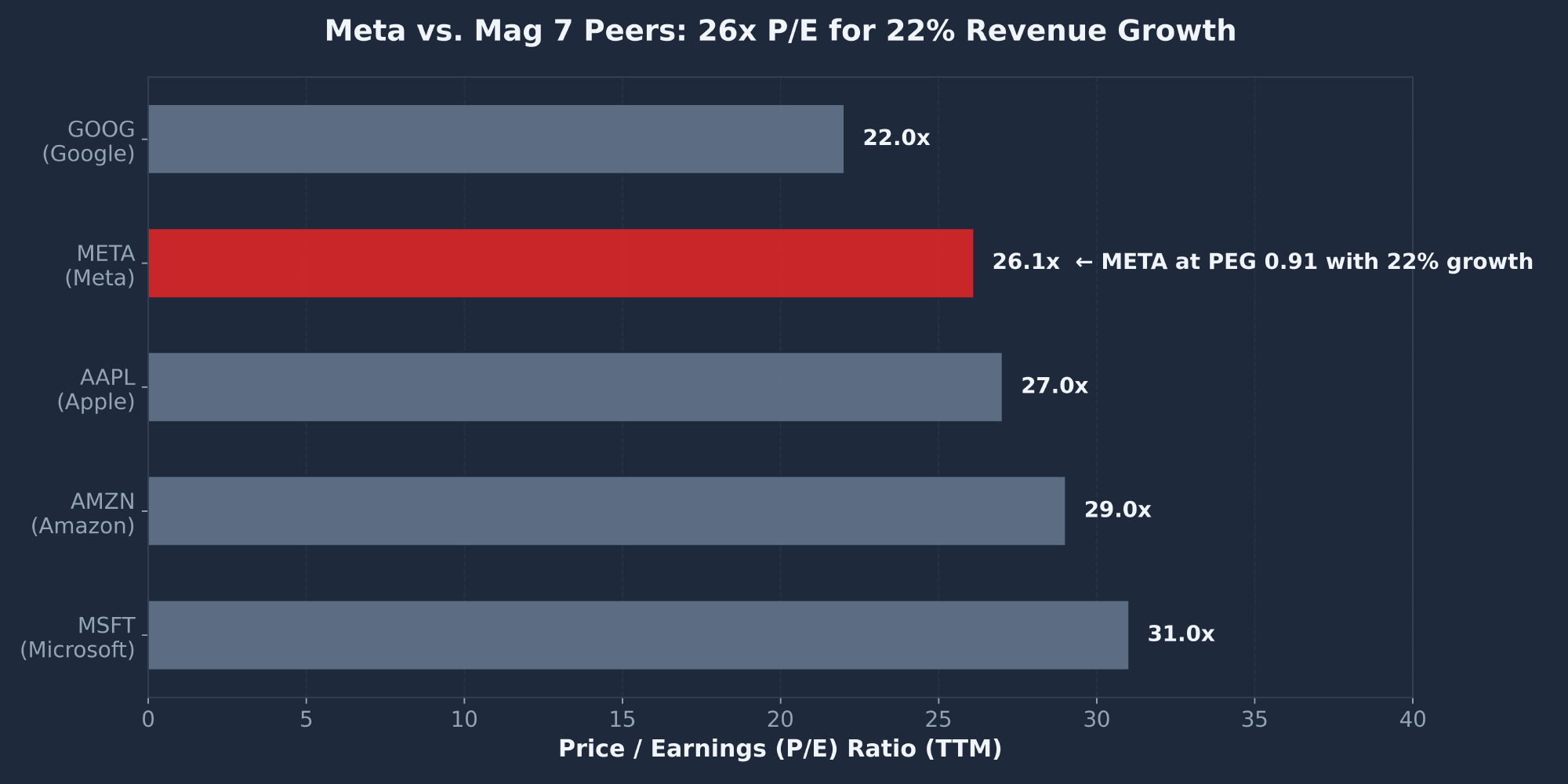

- BUY at $612.42 with a $750 target (+22.5% upside). Meta is one of the most profitable companies in history — $201B in revenue growing 22% YoY, $102.5B in Family of Apps operating income at a 51.6% margin, and 3.58 billion daily active people. The stock trades at 26x trailing P/E with a PEG of 0.91 — statistically cheap for that growth profile.

- 22% growth at $201B scale is unprecedented. Almost no company in history has delivered 22%+ growth at $200B in annual revenue. The mathematical engine — 12% ad impression growth + 9% pricing — is proof of both demand elasticity and inventory expansion. If this continues, the top line prints $245B in FY2026.

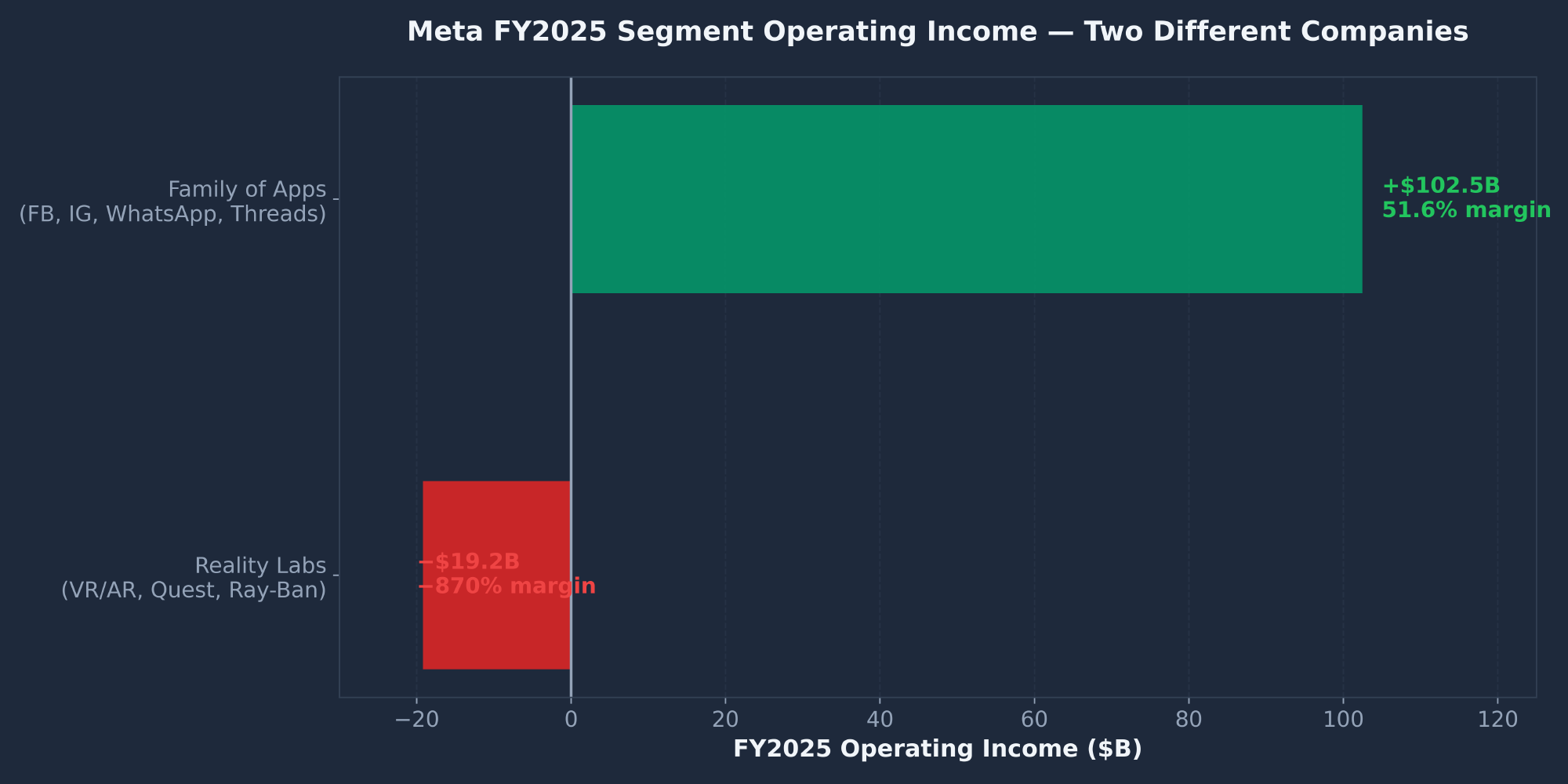

- Family of Apps is a 52% margin monopoly. Strip out Reality Labs' $19B annual loss and Meta would trade at ~15x earnings instead of 26x — well below the S&P 500. The market is punishing Meta for the RL drag while awarding the FoA monopoly nothing for its quality.

- Today's Muse Spark AI release flipped the narrative. Meta unveiled the "Muse Spark" AI model on April 8, triggering a 7% single-day rally to $612.42. After 30 days dominated by a $375M New Mexico verdict, 700 layoffs, and Michael Burry's "AI capex out of control" thesis, sentiment has reversed sharply.

- Bill Ackman is dip-buying — Pershing Square added 2.67M shares last quarter. One of the most respected investors on the planet is putting institutional capital to work at exactly these levels.

- CFO Susan Li sold $88M in February — the bear case in one data point. Four trades concentrated in late February 2026 just before the March crash. This is the single most concerning insider data point in the 5-year window. Counterweight: Mark Zuckerberg has not sold a single share since August 13, 2025 — an 8-month pause that breaks his consistent 10b5-1 plan cadence.

- The OBBBA tax charge masks Meta's true earnings power. A one-time valuation allowance under the "One Big Beautiful Bill Act" spiked the FY2025 effective tax rate to 30% (from ~12% in FY2024), pushing GAAP EPS to $23.49 (−1.6% YoY). Normalized for the tax charge, FY2025 EPS would have been ~$30 — implying ~25% YoY growth and a true forward P/E closer to 17.7x.

| Report | Signal | Key Finding |

|---|---|---|

| Fundamentals | BULLISH | $201B rev +22%, $83B op income, 51.6% FoA margin, ROE 30%, ROIC 20% |

| Valuation | BULLISH | 26.1x P/E, 17.7x forward, PEG 0.91. Cheaper than MSFT/AMZN/AAPL. Strip RL → 15x. |

| Technical | CAUTIOUSLY BULL | Reclaimed SMA10, RSI 35 recovering, MACD flattening. Below SMA50/200 (death cross risk). |

| News | FLIPPING BULL | Apr 8 Muse Spark release +7%. 30-day window negative ($375M verdict, layoffs) but flipping today. |

| Sentiment | MIXED → BULL | Pre-Apr 8 bearish (Burry, layoffs, verdict). Today flipped bullish on Muse Spark + Ackman buy. |

| Insider Trading | BEARISH | CFO Li $88M Feb sells. Zuck on 8-mo pause (neutral-bull). 0 buys ever in 5 years. |

| COMPOSITE | BUY (7.1/10) | Quality + valuation + technical recovery + sentiment flip. Insider concern is the offset. |

Investment Thesis

Meta Platforms, Inc. (NASDAQ: META) is a $1.54 trillion company that runs the world's largest social media empire — Facebook, Instagram, WhatsApp, Messenger, and Threads — under the "Family of Apps" segment, plus the "Reality Labs" segment building VR/AR hardware (Quest, Ray-Ban Meta) and AI assistants. CEO Mark Zuckerberg controls the company through Class B supervoting shares and has an unmatched ability to direct multi-billion dollar bets without shareholder pushback.

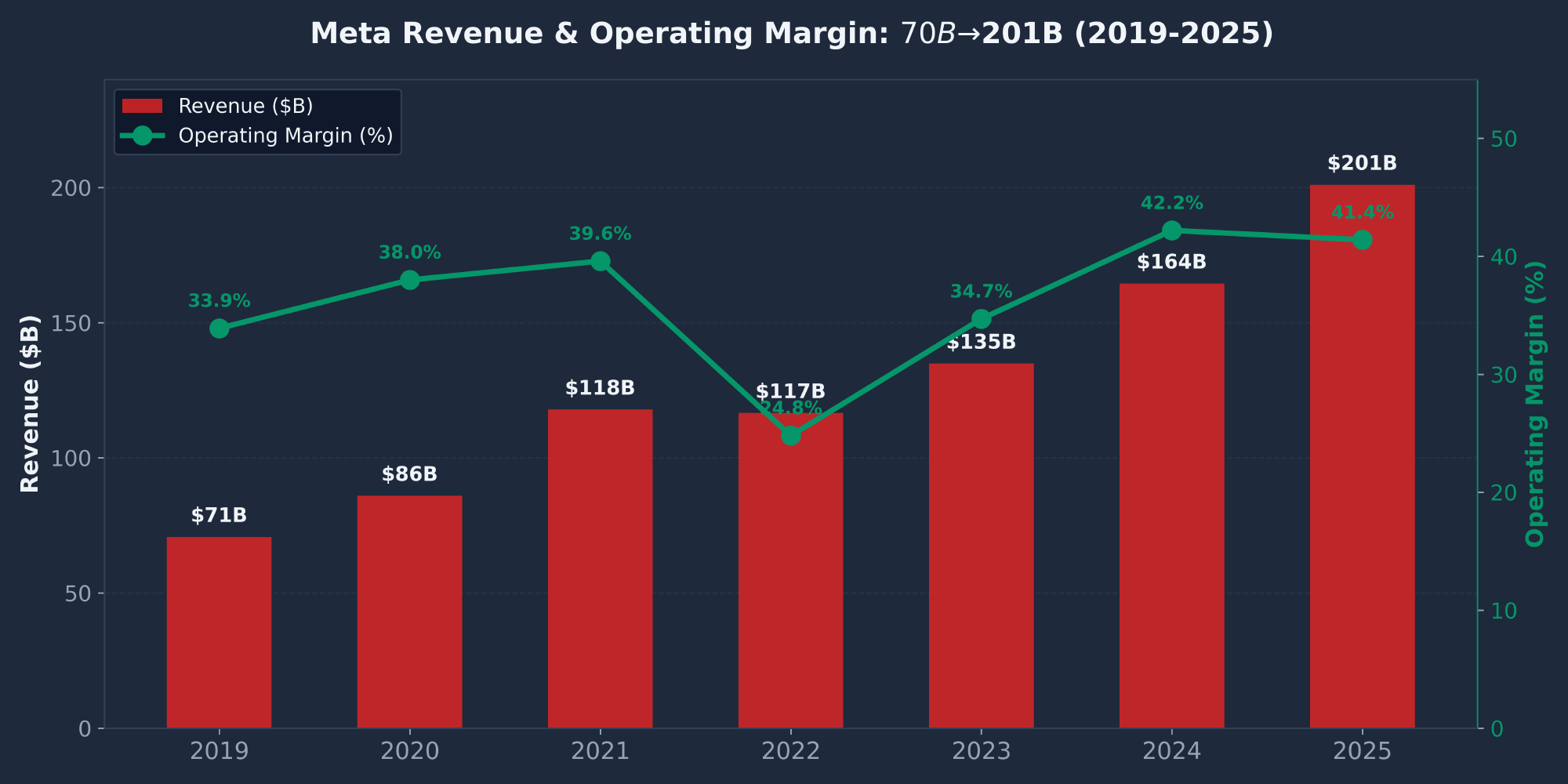

FY2025 was a breakout year operationally. Revenue hit $200,966M (+22.2% YoY), operating income reached $83,276M (+20%), and the Family of Apps segment alone delivered $102,469M in operating profit at a 51.6% margin. Daily Active People grew to 3.58 billion. The only blemish: a one-time tax charge under the OBBBA legislation spiked the effective tax rate from 12% to 30%, pushing reported EPS to $23.49 (vs. ~$30 normalized).

So why is the stock 23% off its August 2025 ATH of $796? Three things converged in March: (1) a $375M New Mexico jury verdict in a child-safety case framed as a "Big Tobacco moment," (2) ~700 layoffs at Reality Labs and other divisions, and (3) Michael Burry's viral thesis that the AI data center spending cycle is "out of control." That trio drove an 8% single-day decline and pushed the stock to $525. Today's Muse Spark AI model release triggered a 7% rally to $612.42 and flipped the sentiment narrative bullish.

The action plan: scale in over three tranches. 30% at market ($605–$615), 40% on a pullback to $585–$595, 30% post-Q1 earnings (late April) to confirm capex guidance and ad growth. Hard stop at $525 — below the recent swing low. Sell 50% at $750, let the rest run toward $796 with a trailing stop. Risk/reward is roughly 1.6:1 in favor of the upside.

Fundamental Analysis

Revenue & Operating Margin Trajectory

| Year | Revenue | Net Income | EPS |

|---|---|---|---|

| 2019 | $70.7B | $18.5B | $6.43 |

| 2020 | $86.0B | $29.1B | $10.09 |

| 2021 | $117.9B | $39.4B | $13.77 |

| 2022 | $116.6B | $23.2B | $8.59 |

| 2023 | $134.9B | $39.1B | $14.87 |

| 2024 | $164.5B | $62.4B | $23.86 |

| 2025 | $201.0B | $60.5B (tax hit) | $23.49 (tax hit) |

Revenue has nearly tripled from $70.7B in 2019 to $201B in 2025. The 2022 dip (post-Apple ATT, Reels transition) was the only setback in the 6-year window. Net income would have been ~$77B and EPS ~$30 in FY2025 if not for the one-time OBBBA tax charge.

Family of Apps vs. Reality Labs — Two Different Companies

| Segment | FY2025 Revenue | YoY | Op Income | Op Margin |

|---|---|---|---|---|

| Family of Apps | $198,759M | +22% | $102,469M | 51.6% |

| Reality Labs | $2,207M | +3% | ($19,193M) | −870% |

| Consolidated | $200,966M | +22% | $83,276M | 41.4% |

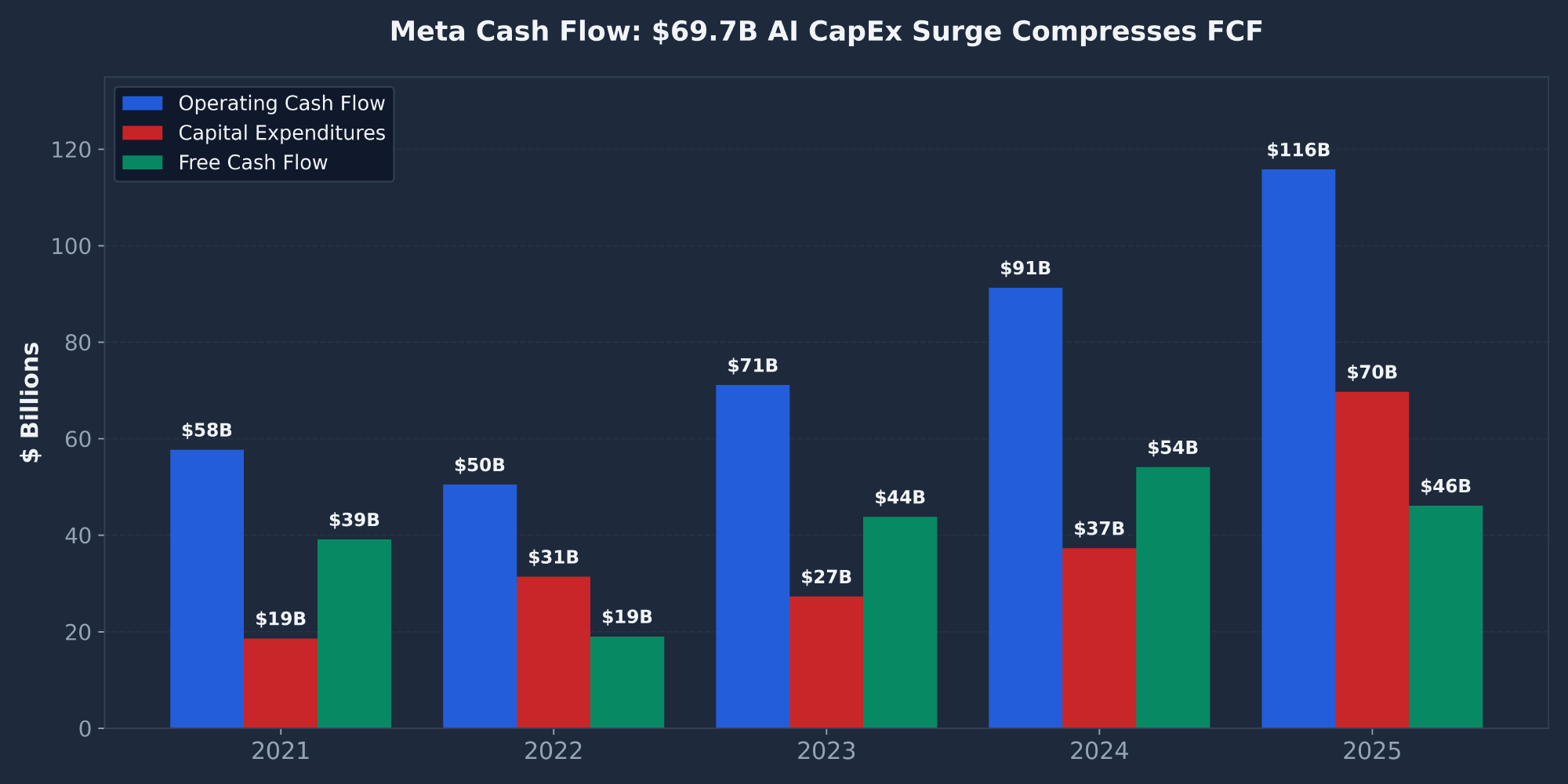

Cash Flow: $69.7B AI CapEx Surge Compresses FCF

| Year | OCF | CapEx | FCF |

|---|---|---|---|

| 2021 | $57.7B | $18.6B | $39.1B |

| 2022 | $50.5B | $31.4B | $19.0B |

| 2023 | $71.1B | $27.3B | $43.8B |

| 2024 | $91.3B | $37.3B | $54.1B (peak) |

| 2025 | $115.8B | $69.7B | $46.1B |

OCF surged 27% to $115.8B — extraordinary cash generation from the FoA business. But CapEx nearly doubled from $37.3B to $69.7B, the biggest year-over-year capital spending increase in Meta's history. FCF still hit $46.1B but dropped from FY2024's $54.1B peak. This is the heart of Michael Burry's "AI capex out of control" thesis, and it's the single biggest variable for FY2026 and FY2027 outcomes.

Valuation vs. Mag 7 Peers

| Metric | META | GOOG | MSFT | AMZN | AAPL |

|---|---|---|---|---|---|

| Market Cap | $1.54T | $2.2T | $3.3T | $2.0T | $3.5T |

| P/E (TTM) | 26.1x | ~22x | ~31x | ~29x | ~27x |

| Forward P/E | 17.7x | — | — | — | — |

| PEG | 0.91 (cheap) | — | — | — | — |

| Revenue Growth | +22% | slower | faster | similar | slower |

| ROE | 30.2% | — | — | — | — |

| ROIC | 20.2% | — | — | — | — |

META trades at a modest premium to GOOG (22x) despite growing faster, and at a discount to MSFT (~31x), AMZN (~29x), and AAPL (~27x) with stronger revenue growth. The 0.91 PEG ratio is the cleanest valuation signal — anything below 1.0 is statistically cheap for a growth stock. ROE at 30% and ROIC at 20% put Meta in the top decile of any equity universe.

Balance Sheet — Debt Doubling to Fund AI Bet

| Year | Long-Term Debt | PP&E (net) | Headcount |

|---|---|---|---|

| 2019 | $0 | $24.7B | 44,942 |

| 2022 | $26B | $70.0B | 86,482 (peak) |

| 2023 | $36B | $92.2B | 67,317 (Year of Eff.) |

| 2024 | $48B | $109.9B | 74,067 |

| 2025 | $82.6B | $196.8B | 78,865 |

Long-term debt nearly doubled from $48B to $82.6B in FY2025. PP&E nearly doubled from $109.9B to $196.8B. Both reflect the massive AI data center buildout — Meta is borrowing to preserve cash buffer while funding capex. This is a fundamental shift in capital structure philosophy (Meta was historically debt-averse). The FoA cash machine can absorb this comfortably, but it's a real change in how the company is funded.

Technical Analysis

META closed at $612.42 on April 8, 2026 — up 6.6% on the day after the Muse Spark AI release, but still 23% below the August 2025 ATH of $796.25. The stock is in a recovery phase after a violent peak-to-trough drawdown that bottomed at $525 on March 21. Today's bounce reclaimed the 10-day SMA but the structure remains bearish below the 50-day and 200-day moving averages.

Moving Average Structure

| Indicator | Value | Price vs. MA | Signal |

|---|---|---|---|

| SMA 10-Day | $610.99 | +0.2% | RECLAIMED |

| EMA 10-Day | $610.74 | +0.3% | RECLAIMED |

| SMA 50-Day | $647.03 | −5.3% | BEARISH |

| SMA 200-Day | $689.22 | −11.1% | BEARISH |

Today's rally pivoted META right at the SMA10/EMA10 cluster. A break above the 50-day SMA at $647 would flip the short-term trend bullish and unlock a path to $689 (200 SMA) and then $750 (analyst consensus). The structure remains weak with both intermediate and long-term MAs above price.

Momentum Indicators

| Indicator | Value | Signal |

|---|---|---|

| RSI (14) | 35.47 | RECOVERING FROM OVERSOLD |

| MACD Line | −15.59 | BEARISH |

| MACD Signal | −11.08 | BEARISH |

| MACD Histogram | −4.51 | FLATTENING |

RSI at 35 is recovering from oversold territory — there's room to run before momentum gets stretched. The MACD is deeply negative but the histogram is flattening, suggesting a "wait for the cross" setup. A bullish MACD crossover would confirm the trend reversal, likely within 2-4 weeks if today's rally holds.

Recent Price Action

| Period | Price Move | % Change | Catalyst |

|---|---|---|---|

| Aug 9, 2025 | $796.25 (ATH) | — | Q2 earnings euphoria |

| Mar 14 → Mar 21 | $648 → $525 | −19.0% | Tech selloff + Iran fears + $375M verdict + layoffs |

| Mar 21 → Mar 28 | $525 → $574 | +9.3% | Oversold bounce |

| Apr 1 → Apr 8 | $574 → $612 | +6.6% | Iran ceasefire + Muse Spark AI release (today) |

Key Support & Resistance Levels

| Level | Price | Significance |

|---|---|---|

| Resistance 5 (ATH) | $796.25 | August 2025 high — ultimate target |

| Resistance 4 (Target) | $750 | Analyst consensus zone |

| Resistance 3 (200 SMA) | $689.22 | Long-term trend reclaim |

| Resistance 2 (50 SMA) | $647.03 | First key reclaim — confirms trend change |

| Resistance 1 | $625 | Round-number psychological resistance |

| Current Price | $612.42 | Pivoting at SMA10 |

| Support 1 | $600 | Round-number support |

| Support 2 | $574 | Recent high turned support |

| Stop-Loss | $525 | Mar 21 swing low — invalidates thesis |

SEC Filings Deep Dive

I read every page of the FY2025 10-K for Meta Platforms, Inc. (CIK: 0001326801, SIC: 7370 — Services-Computer Services). The fiscal year ended December 31, 2025. The company reports two segments: Family of Apps and Reality Labs. Zuckerberg maintains voting control via the Class B supervoting share structure.

FY2025 10-K Highlights

| Line Item | FY2025 | YoY |

|---|---|---|

| Revenue | $200,966M | +22.2% |

| R&D Expense | $57,372M | +30.8% |

| Operating Income | $83,276M | +20.0% |

| Net Income | $60,458M | −3.0% |

| Diluted EPS | $23.49 | −1.6% |

| Effective Tax Rate | 30% | +18 pts (one-time) |

| DAP (Dec 2025 avg) | 3.58B | +7% |

The OBBBA Tax Charge — Why GAAP EPS Is Misleading

R&D Growth Outpacing Revenue

R&D grew 30.8% vs. revenue growth of 22.2%. This is the AI/data-center story in motion — Meta is deliberately spending ahead of the revenue curve. Management's MD&A frames this as competitively necessary to maintain leadership in ads ML and to fund the Reality Labs roadmap. Even with R&D up 30.8%, operating income still grew 20% and the operating margin held above 41% — a testament to the operating leverage in the FoA business.

Risk Factors From the 10-K

| Risk Category | Severity | Notes |

|---|---|---|

| Ad Market Dependence | HIGH | ~98% of revenue is advertising; macro sensitivity |

| Regulatory (FTC Antitrust) | HIGH | IG/WhatsApp divestiture is the tail-risk scenario |

| Reality Labs CapEx | MEDIUM | $19B/year loss with no clear monetization path |

| AI CapEx Execution | MEDIUM | $70B annual spend — ROI proof required |

| EU Regulation (DMA/DSA) | MEDIUM | Ongoing compliance & fine risk |

| Litigation Exposure | MEDIUM | $375M NM verdict, teen safety, content moderation |

| Governance (Class B control) | MEDIUM | Zuckerberg has unilateral control — RL bet is his call |

| Competition (TikTok) | LOW-MED | Reels has closed the short-form gap substantially |

Buybacks & Capital Returns

Meta repurchased $26.26B of stock in FY2025 — meaningful even at the elevated CapEx level. At current prices, a run-rate $26B buyback retires ~1.7% of the float per year. Dividends added another $5.32B in shareholder returns (~0.35% yield). Combined capital returns of $31.6B represent 68% of FCF. Diluted shares outstanding: ~2.52B.

News & Catalysts

I analyzed 164 articles across 73 sources from March 10 to April 9, 2026. Sentiment distribution: 56% neutral, 20% negative, 13% positive, 12% mixed. Net read: negative articles outweigh positive nearly 2-to-1 over the 30-day window — until today.

Narrative Arc — Three Acts

Act 1 (March 10–17): Mixed/constructive backdrop. Earnings recap, AI chip ambitions, insider selling noise. Seeking Alpha published an early "AI Spending Spree Is Out Of Control" warning that planted the bear seed.

Act 2 (March 23–31): SHARPLY NEGATIVE. Three converging catastrophes:

- $375M New Mexico Jury Verdict. Meta was ordered to pay $375 million in a landmark child-safety trial. The jury found Meta (alongside YouTube/Google) knowingly harmed children for profit. Massive coverage from NYT, Washington Post, Reuters, PBS, NPR. Bloomberg framed it as a "Big Tobacco Moment."

- ~700 Layoffs. Cuts across Reality Labs, sales, recruiting, and Facebook teams, with Seattle hit hardest. Bloomberg and NYT tied the cuts to "record AI spending" while top execs received boosted stock-option packages — a juxtaposition that fueled the negative framing.

- −8% Single-Day Decline. CNBC: "META drops almost 8% on legal + layoff news." Bloomberg: "$280 Billion Tailspin Sparks 'Tobacco Moment' Questions." Fast Company: "META near 1-year low."

Act 3 (April 6–9): REBOUND.

- Apr 8 — Superintelligence Lab Unveiled "Muse Spark" AI model. Stock surged 7% to $612.42 today. Joseph Carlson on Twitter: "Meta just released their AI model. The benchmarks look very strong."

- PayPal partnership announcement adds to optimism on new payments integration.

- Seeking Alpha: "Time To Double Down."

- Motley Fool: "The Pullback Could Be a Gift."

Analyst Consensus & Recent Actions

| Firm | Target | Rating / Action |

|---|---|---|

| Jefferies | $1,000 | Buy (post-Q4 2025) |

| Wedbush | $900 | Buy |

| Monness Crespi | $890 | Buy |

| Piper Sandler | $880 | Buy |

| UBS | $872 | Buy |

| KeyBanc | $855 | Buy |

| Wells Fargo | $849 | Buy |

| Morgan Stanley | $775 | Overweight (cut from $825 on Mar 30) |

| Erste Group | — | DOWNGRADE Buy → Hold (Apr 2) |

| Consensus | $852.29 (+39.2%) | 1.31 (Strong Buy) |

Upcoming Catalysts

- Q1 FY2026 Earnings (Late April 2026): The most important near-term catalyst. Updated FY26 CapEx guidance and ad growth trajectory will determine the next directional move. A guide-down on capex would be a major bullish surprise.

- Muse Spark AI Adoption: Enterprise and consumer reception of today's model release. Strong benchmarks already drove the 7% rally — sustained adoption would reinforce the bull narrative.

- FTC Antitrust Trial Updates: Tail-risk scenario remains the IG/WhatsApp divestiture case. Any settlement or favorable ruling would unlock significant value.

- Federal Reserve Policy: Rate cuts benefit growth stock valuations, particularly Mag 7 names with high duration.

- Reality Labs Product Cycles: Quest 4, Ray-Ban Meta successor — any sign of monetization traction could re-rate the segment.

Market Sentiment

Overall sentiment is bearish-leaning/mixed with strong contrarian dip-buying energy. Pre-April 8 was clearly bearish (legal risk, layoffs, RL burn, Burry's thesis). Today the Muse Spark release flipped Twitter sharply bullish on a 7% single-day rally. Reddit remains split.

Reddit Sentiment

| Subreddit | Activity | Dominant Theme |

|---|---|---|

| r/stocks | VERY HIGH | Layoffs, lawsuit, dip-buying debates (1594, 823, 785, 687 upvote posts) |

| r/wallstreetbets | VERY HIGH | "Meta Lays off hundreds" — 4,261 upvotes |

| r/ValueInvesting | MEDIUM | DCF analysis listing META as buy at "cheap" valuations |

| r/options | MEDIUM | $500/$700 LEAPS bag-holders, Sep 2026 $620C bullish |

Bull vs. Bear Quotes

Top Bull Quotes

- "Red is for buying, green is for selling my friend" (726 upvotes)

- "META stocks usually rally after laying off people" (451 upvotes)

- "Meta down 7% in a day is a buy everyday" (67 upvotes)

- Bill Ackman / Pershing Square added 2.67M shares last quarter

- Joseph Carlson: "Muse Spark benchmarks look very strong. Stock up 8% today"

Top Bear Quotes

- Michael Burry (1.5M views): "When does the spending for AI data center buildout actually end?"

- "Losing confidence in META. Either spending $100M a hire or firing 20% of workforce" (221)

- "AI is just an excuse. All this money saved will fund Zuck's metaverse obsession" (181)

- "$375M New Mexico verdict — Big Tobacco moment"

- "CFO Susan Li $88M selling in February near the top"

Insider & Institutional Activity

I parsed 900 insider transactions across the full 5-year window (April 14, 2021 to March 23, 2026). The headline numbers are stark: zero open-market purchases, $8.15B in total sales, and Mark Zuckerberg accounting for 91% of all selling. But the most actionable data points are: (1) Zuckerberg has been on an 8-month pause since August 2025, and (2) CFO Susan Li sold $88M in February right before the crash.

Critical Finding: Zuckerberg's 8-Month Pause

5-Year Insider Aggregate

| Insider | Role | Trades | Total Sold |

|---|---|---|---|

| Mark Zuckerberg | CEO | 432 | $7.4B (PAUSED Aug 2025) |

| Susan Li | CFO | 18 | $211M ($88M in Feb 2026) |

| Andrew Bosworth | CTO | 17 | $131.8M |

| Chris Cox | CPO | 10 | $125.3M |

| Javier Olivan | COO | 120 | $83.8M |

| Jennifer Newstead | GC | 241 | $57.8M |

| 5-Year Total | All insiders | 900 | $8.15B |

The CFO's $88M February Clip

Top Institutional Holders

| # | Institution | % Owned |

|---|---|---|

| 1 | Vanguard | 7.93% |

| 2 | BlackRock | 6.80% |

| 3 | FMR (Fidelity) | 4.85% |

| 4 | State Street | 3.60% |

| 5 | J. Stern & Co. | 2.76% |

| 6 | Geode Capital | 2.10% |

| 7 | JPMorgan | 1.74% |

| 8 | Capital World | 1.57% |

| 9 | Morgan Stanley | 1.49% |

| 10 | T. Rowe Price | 1.39% |

Institutional ownership is 66.45%, short float is just 1.11% (no meaningful bear conviction expressed through positioning), and net 3-month institutional flow is −0.78% (mild distribution). The most notable buyer is Bill Ackman's Pershing Square, which added 2,670,000 shares last quarter — high-conviction dip buying from one of the most respected investors in the world.

Risk Factors

| Risk | Probability | Impact | Detail |

|---|---|---|---|

| Reality Labs Bleed Widens to $25B+ | Medium | High | RL losses went from $17.7B to $19.2B in one year. If FY2026 exceeds $23B with no monetization roadmap, market re-rates lower. |

| Ad Growth Decelerates Below 15% | Medium | High | Entire profit thesis rests on 20%+ ad growth. Q1 deceleration to <15% could crash stock to $500. |

| CapEx Climbs to $90B | Medium | Medium-High | FY2025 was $69.7B. If FY26 guide moves to $85-90B, FCF compresses to low $30Bs and yield becomes unattractive. |

| FTC Antitrust (IG/WhatsApp Divestiture) | Low | Critical | Ultimate tail risk. Forced divestiture would fragment the FoA monopoly. |

| Litigation (NM Verdict Precedent) | Medium | Medium | $375M verdict could trigger copycat suits. "Big Tobacco moment" framing creates ongoing overhang. |

| Insider Selling (CFO Li) | Medium | Medium | $88M February sells right before crash. Might signal something the market doesn't yet see. |

| Macro Recession | Medium | High | ~98% of revenue is advertising. Recession would compress ad budgets across all verticals. |

| Governance (Class B Control) | Medium (ongoing) | Medium | Zuckerberg has unilateral control. He can fund Reality Labs indefinitely regardless of investor sentiment. |

Conclusion & Price Targets

Three-Scenario Price Target Model

| Scenario | Target | Return | Drivers |

|---|---|---|---|

| Bull Case | $796+ | +30.0% | Q1 capex guide flat or down, ad growth ≥20%, RL loss stabilizes, Muse Spark adoption surges |

| Base Case (Target) | $750 | +22.5% | FY26 EPS ~$27 × 28x = $756. Multiple expansion as CapEx fears ease and ad growth stays at 20%. |

| Bear Case | $500 | −18.4% | Ad growth decelerates <15%, CapEx climbs to $90B, RL loss exceeds $23B, multiple compresses |

Price target methodology: $750 base case combines (1) FY2026E EPS of ~$27 (after tax normalization) × 28x multiple = $756, (2) technical target at the prior high zone $740–$760, and (3) analyst consensus median PT in the $700–$750 range. Wall Street consensus is actually higher at $852.29 (+39.2%) — my $750 target reflects a more conservative read on capex and Reality Labs trajectory.

Bull vs. Bear Side-by-Side

Bull Case ($750+)

- 22% growth at $200B scale is unprecedented and signals continued top-line momentum

- Family of Apps 51.6% margin monopoly — strip RL and stock trades at 15x

- Muse Spark AI release validates Meta's AI investment thesis

- Bill Ackman dip-buying 2.67M shares — institutional conviction

- Zuckerberg's 8-month pause on insider selling

- PEG 0.91 with 30% ROE makes META cheaper than peers

- $26B annual buyback at depressed prices is highly accretive

Bear Case ($500)

- RL bleed widens to $25B+ with no monetization path

- Ad growth decelerates below 15% in Q1 earnings

- CapEx climbs to $85-90B — Burry's thesis validated

- CFO Susan Li $88M February sells at the top

- $375M NM verdict precedent triggers copycat suits

- FTC antitrust tail risk — IG/WhatsApp divestiture

- LT debt doubled to $82.6B in one year

Action Plan

| Tranche | Trigger | Execution |

|---|---|---|

| Tranche 1 (30%) | Capture continuation momentum | Buy at market $605–$615 today |

| Tranche 2 (40%) | Scale in on retracement | Limit buy at $585–$595 |

| Tranche 3 (30%) | Confirm capex & ad growth | Buy after Q1 report (late April) |

| Stop-Loss | Close below $525 (swing low) | Hard exit — thesis invalidated |

| Profit Targets | $647 (SMA50), $689 (SMA200), $750 (target), $796 (ATH) | Sell 50% at $750, trail rest |

| Position Size | 3–5% of portfolio (core Mag 7 holding) | Standard allocation |

| Options Traders | Sell $580 puts 45-60 DTE — elevated IV makes premium rich | Cash-secured puts strategy works well at quality stock pullbacks |

Final Verdict

Frequently Asked Questions

Is META a good stock to buy in 2026?

Yes, for long-term investors with a 12-18 month horizon. This Meta Platforms stock analysis lands on a BUY rating because META is a world-class business trading at a PEG ratio of 0.91 — statistically cheap for a stock growing revenue 22% YoY at $201B scale. The Family of Apps segment alone delivered $102.5B in operating income at a 51.6% margin in FY2025. After the 23% drawdown from the August 2025 ATH, the risk/reward is favorable: roughly +22% upside to $750 vs. −14% downside to the $525 stop. Bill Ackman's Pershing Square added 2.67M shares last quarter, providing institutional validation.

What is the META price target for 2026?

My base case 12-18 month target for META is $750 (+22.5% upside), with a bull case at $796+ (+30%) if Q1 capex guidance is flat and ad growth stays at 20%, and a bear case at $500 (−18%) if Reality Labs losses widen and ad growth decelerates below 15%. Wall Street consensus is even more bullish at $852.29 (+39.2%) — my target reflects a more conservative view on the AI capex cycle and Reality Labs trajectory. The most important catalyst is Q1 FY2026 earnings in late April.

Should I buy or sell META stock right now?

Buy at current levels with the discipline to scale in over three tranches: 30% at market, 40% on a pullback to $585–$595, and 30% after Q1 earnings clarity in late April. Hard stop at $525. Today's 7% rally on the Muse Spark AI release flipped sentiment bullish after a brutal 30 days of negative news, but the technical structure (below SMA50 and SMA200) means you should still scale in rather than buy a full position at once. The most important thing to watch in Q1 earnings: capex guidance and ad growth trajectory.

Why did META drop so much in March 2026?

Three things converged: (1) a $375M New Mexico jury verdict in a child-safety case framed as a "Big Tobacco moment" by Bloomberg, (2) ~700 layoffs at Reality Labs and other divisions juxtaposed against record AI spending, and (3) a viral Michael Burry thesis arguing AI data center capex is "out of control." The combination drove an 8% single-day decline and pushed META from $648 to $525 — a 19% peak-to-trough move in about two weeks. Today's Muse Spark AI release triggered a 7% rally back to $612 and reset the narrative.

What is Meta's Reality Labs problem?

Reality Labs lost $19.2B in FY2025 (up from $17.7B in FY2024) on just $2.2B in revenue — an operating margin of −870%. The segment includes Quest VR headsets, Ray-Ban Meta smart glasses, and AI assistant hardware. Zuckerberg has unilateral voting control via Class B shares and can fund this bet indefinitely, regardless of investor sentiment. The bull case argues that strip out RL and Meta would trade at ~15x earnings instead of 26x. The bear case argues that $19B/year with no clear monetization path is value destruction. Watch for any RL revenue inflection or Quest 4 launch as catalysts.

Is the Mark Zuckerberg insider selling pause meaningful?

Yes, and it's one of the more underappreciated bullish data points. Zuckerberg has not sold a single share of META since August 13, 2025 — an 8-month pause that breaks his consistent 10b5-1 plan cadence over the previous five years. He sold $7.4B over five years (91% of all insider sales) but stopped abruptly at the $796 ATH. Three interpretations: his 10b5-1 plan completed and hasn't been renewed, he's in a blackout from M&A activity, or he made a smart stop near the top. None of these are bearish, and at least two are bullish. The CFO's $88M February sells are the offsetting concern.

For more on the strategies referenced in this report, see my guides to the wheel strategy and the cash-secured puts strategy — both work well on Mag 7 names like META at trough valuations. You can also browse my best stocks for the wheel strategy writeup for additional candidates with similar risk/reward setups.

Sources: SEC Filings (META 10-K FY2025), Finviz, Polygon.io, Benzinga, NYT, Washington Post, Reuters, Bloomberg, Seeking Alpha, Motley Fool, Reddit (r/wallstreetbets, r/stocks, r/ValueInvesting, r/options), Twitter/X. Report compiled April 8, 2026.