RIVN (Rivian) Stock Analysis: Hold at $15 | $16 Target

Table of Contents

Executive Summary

This Rivian Automotive stock analysis covers RIVN's fundamentals, technicals, SEC filings, market sentiment, and insider activity as of March 2026. Here is the bottom line:

- HOLD — do not initiate a new position at $14.86. The risk/reward is roughly neutral at current levels. The probability-weighted 12-month target is $16 (+8%), insufficient to justify new capital when the downside in a bear scenario is -66%.

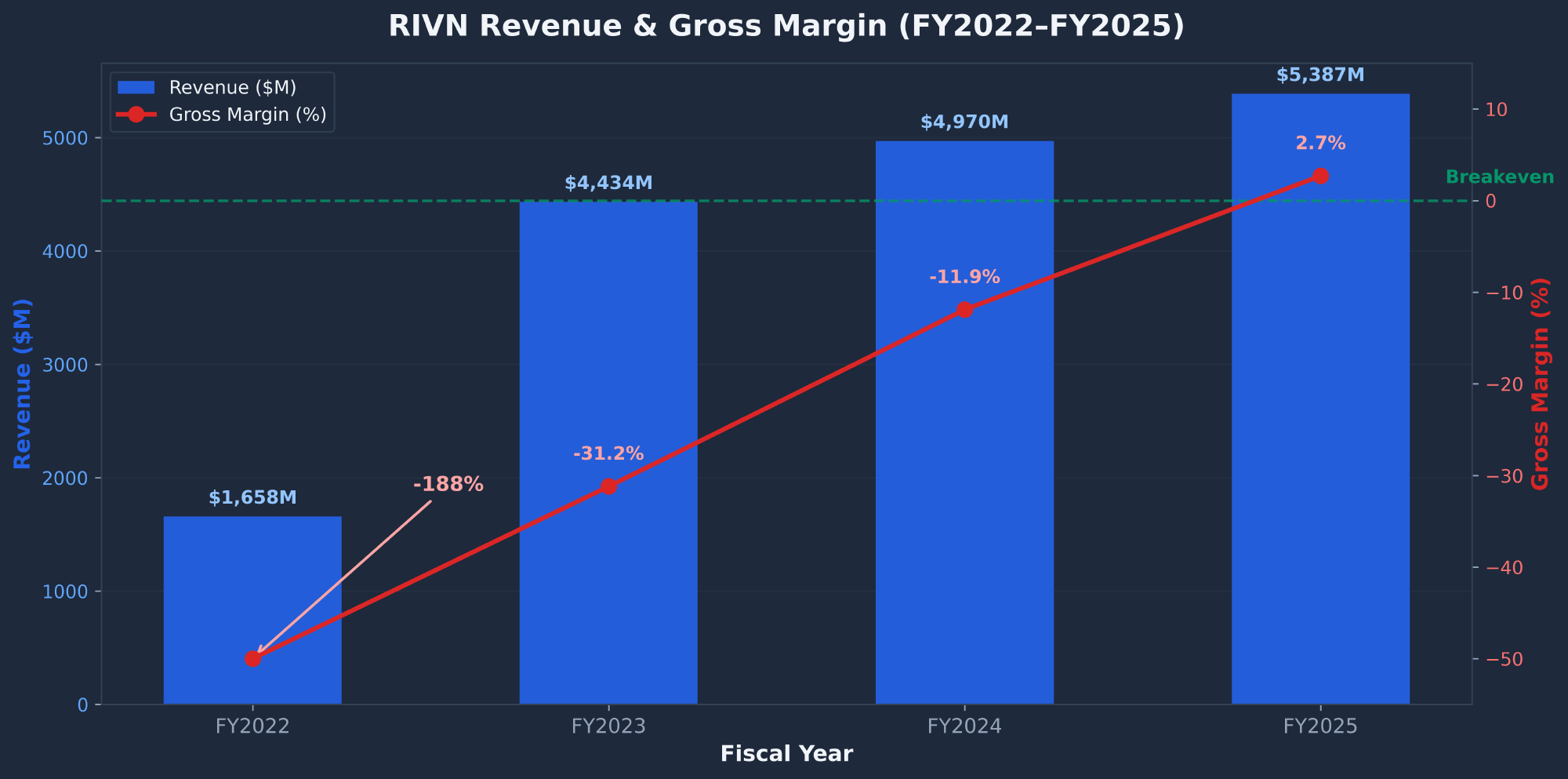

- FY2025 delivered a genuine milestone: Rivian's first-ever positive gross profit of $144M. But look closer — the VW JV contributed $576M in software gross profit. Automotive operations alone still lost $432M at -11.3% gross margin.

- The R2 launch is the single most important catalyst. The R2 Performance Edition ($58K) ships Q2 2026 from Rivian's Normal, IL factory. The mass-market R2 base model ($45K) has been delayed to late 2027. With 100K+ reservations, execution here determines whether RIVN doubles or halves.

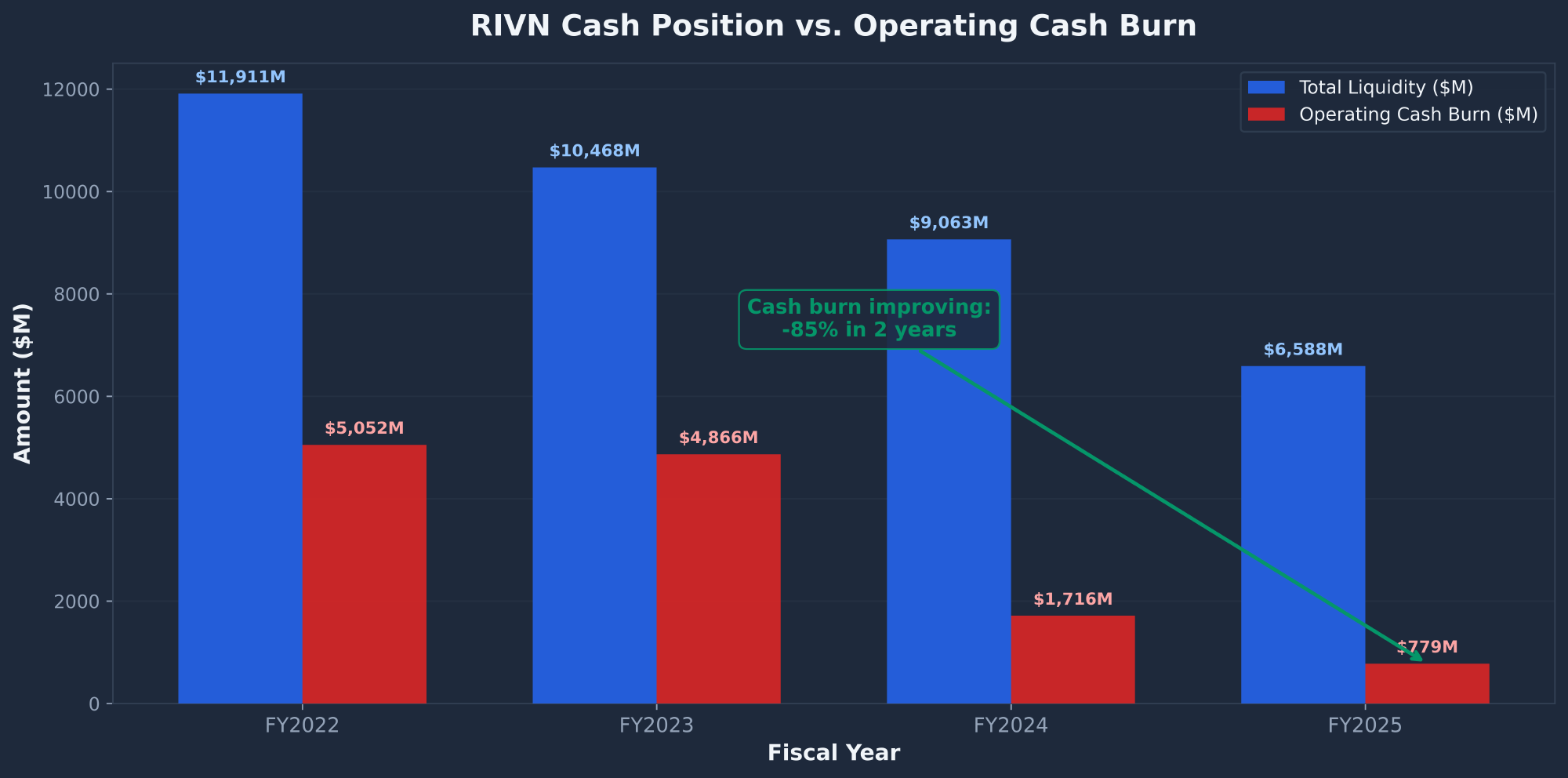

- Cash position is adequate but declining. $6.1B in liquidity plus $2.5B remaining from VW and a $6.6B DOE loan (undrawn) provide runway. But operating burn of $779M plus $1.7B capex means a capital raise within 12–18 months is likely.

- Insiders are not buying. No discretionary insider purchases since May 2022 despite an 81% decline from IPO. CEO's options are underwater at $15.22. Ford exited entirely. Only VW maintaining its 10%+ stake provides institutional conviction.

| Report | Signal | Key Finding |

|---|---|---|

| Fundamentals | NEUTRAL | First gross profit, but auto margins still negative. Revenue $5.39B, net loss $3.65B. |

| Technical | BEARISH | Below all MAs, death cross approaching, 34.5% correction from 52W high. MACD crossover is only bullish signal. |

| SEC Filings | BEARISH | $25B cumulative losses, $1.1B/yr SBC, 40% dilution since IPO, $233M litigation settlement, 10% coupon debt. |

| News & Events | NEUTRAL | 13/18 positive headlines but R2 sell-the-news reaction. Analyst consensus $17.83 (+20%). |

| Sentiment | NEUTRAL | Score 5.5/10. Reddit low. Media bullish framing but retail not engaged. "Next Tesla or next Fisker?" |

| Insider/Institutional | BEARISH | No discretionary buys since May 2022. Systematic selling via 10b5-1. Ford exited. VW holding is only positive. |

| VW Partnership | BULLISH | $5.8B commitment, $1.55B software revenue at 37% margin, $1B term loan available Oct 2026. |

| COMPOSITE | HOLD | 40% bearish, 55% neutral, 5% bullish. Risk/reward roughly neutral. Wait for R2 execution data. |

Investment Thesis

Rivian Automotive sits at an inflection point. The company has achieved its first-ever positive gross profit, secured a transformative $5.8B partnership with Volkswagen Group, and is weeks away from shipping the R2 — the vehicle that will determine whether Rivian becomes a viable mass-market EV manufacturer or remains a niche premium player burning cash at unsustainable rates.

The bull case is straightforward: the R2 Performance Edition ($58K) launches in Q2 2026 with 100K+ reservations, the VW JV generates $1.5B+ in high-margin software revenue, and Rivian follows the Tesla playbook from money-losing startup to profitable automaker. At 3.51x P/S versus Tesla's 13x, the valuation gap implies significant upside if execution delivers.

I assign a 45% probability to the base case ($16 target, +8%), 25% to the bull case ($29, +95%), and 30% to the bear case ($5, -66%). The probability-weighted target of $16 offers insufficient upside to justify initiating a position. Wait for either a break below $12 (better risk/reward) or two consecutive quarters of R2 deliveries above 10K units before committing capital.

Fundamental Analysis

Company Overview

Rivian Automotive, Inc. (NASDAQ: RIVN) is an American electric vehicle manufacturer headquartered in Irvine, California with 15,232 employees. Founded in 2009 by CEO RJ Scaringe (MIT PhD), Rivian went public in November 2021 at $78/share in one of the largest U.S. IPOs in history, briefly reaching a $150B+ market cap. The stock has since declined 81% from its IPO price and 92% from its all-time high of ~$180.

Rivian manufactures the R1T pickup truck, R1S SUV, and Electric Delivery Vans (EDVs) for Amazon at its Normal, Illinois factory. The R2 midsize SUV/crossover — designed for the mass market at ~$45K — launches in Q2 2026 with a Performance Edition at $58K. A second factory in Georgia (Stanton Springs North) targeting 400K vehicles/year is planned but significantly delayed, with construction expected to begin in 2026.

Income Statement

| Metric | FY2025 | FY2024 | FY2023 | FY2022 |

|---|---|---|---|---|

| Revenue ($M) | 5,387 | 4,970 | 4,434 | 1,658 |

| Gross Profit ($M) | 144 | (1,200) | (2,030) | (3,120) |

| Gross Margin | +2.7% | -11.9% | -31.2% | -188% |

| Net Income ($M) | (3,626) | (4,746) | (5,432) | (6,750) |

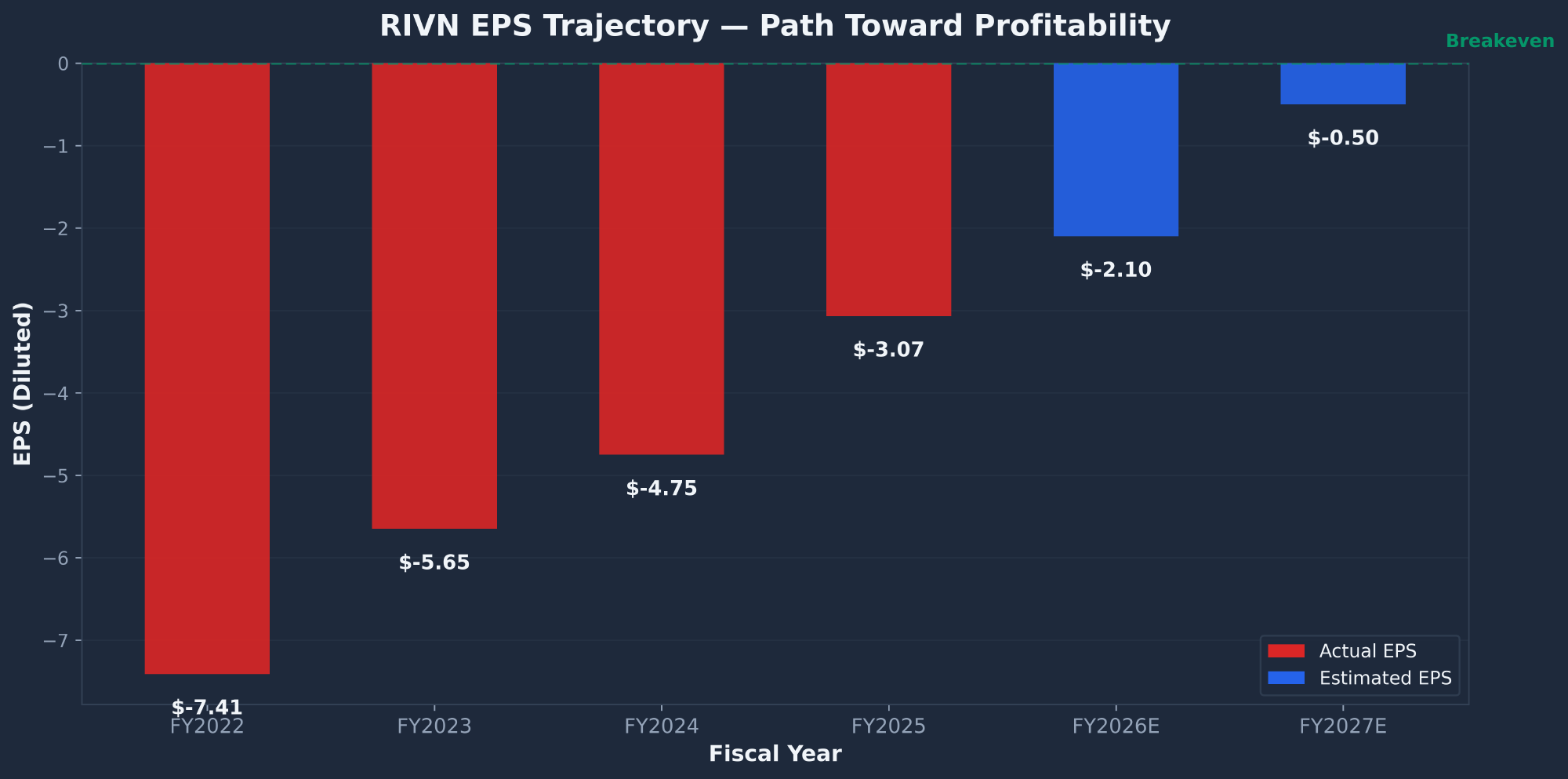

| EPS (Diluted) | ($3.07) | ($4.69) | ($5.74) | ($7.41) |

| Deliveries | 42,247 (-18%) | 51,579 | 50,122 | 20,332 |

| SBC ($M) | ~1,100 | 888 | 814 | 593 |

EPS Trajectory

Cash Position & Burn Rate

Peer Comparison

| Metric | RIVN ($14.86) | TSLA ($391) | LCID ($9.90) |

|---|---|---|---|

| Market Cap | ~$18.9B | ~$1.26T | ~$7.5B |

| Revenue (TTM) | $5.39B | ~$97B | ~$800M |

| P/S (TTM) | 3.51x | ~13x | ~9.4x |

| Gross Margin | +2.7% | ~18% | Deeply negative |

| Net Income | -$3.65B | +$7.1B | ~-$2.5B |

| Short Interest | 17.45% | ~3% | ~15% |

| Strategic Partner | VW ($5.8B JV) | N/A | Saudi PIF |

Technical Analysis

RIVN is at a “do or die” technical level. The stock sits just below the SMA 200 ($14.93) and the 61.8% Fibonacci retracement ($15.07) after a 34.5% correction from the $22.69 52-week high. The MA stack is fully bearish, a death cross is approaching in 6–8 weeks, and RSI never reached oversold during the entire decline — meaning no capitulation washout has occurred.

| Indicator | Value | Signal |

|---|---|---|

| SMA 50 | $16.11 | BEARISH (-7.8%) |

| SMA 200 | $14.93 | NEUTRAL (at level) |

| RSI (14) | 46.95 | NEUTRAL |

| MACD | -0.104 / Signal: -0.146 | BULLISH (crossover) |

| Beta | 1.72 | HIGH VOLATILITY |

| ATR (14) | $0.92 (6.2%) | ELEVATED |

SEC Filings Deep Dive

I analyzed 94 SEC filings spanning 5 annual reports, 13 quarterly reports, and 71 current reports. The filings paint a picture of a company making genuine operational progress while still bleeding cash at scale.

VW Joint Venture Economics

The Volkswagen partnership is Rivian's most strategically important asset. VW has committed $5.8B total, of which ~$3.3B has been received. The JV generated $1.55B in software & services revenue at approximately 37% gross margin ($576M gross profit) in FY2025 — this single revenue stream turned Rivian's consolidated gross margin positive. A $1B JV term loan becomes available in October 2026.

Debt Structure

| Instrument | Amount | Details |

|---|---|---|

| 4.625% Convertible Notes | $1,500M | Due Mar 2029 |

| 3.625% Convertible Notes | $1,725M | Due Oct 2030 |

| 10% Senior Secured Notes | ~$1,250M | Due Jan 2031. 10% coupon = high-yield pricing. |

| DOE ATVM Loan (undrawn) | ~$6,600M | For Georgia plant. Below-market rate. Not yet drawn. |

| VW JV Term Loan | $1,000M | Available Oct 2026. 10-year term. |

News & Catalysts

Analyst Ratings

| Firm | Rating | Target | Upside |

|---|---|---|---|

| Baird | Outperform | $25 | +68% |

| Deutsche Bank | Buy | $23 | +55% |

| TD Cowen | Buy | $20 | +35% |

| UBS | Neutral | $16 | +8% |

| Bank of America | Underperform | $14 | -6% |

| Morgan Stanley | Underweight | $12 | -19% |

| Bernstein | Underperform | $6.10 | -59% |

Consensus target: $17.83 (+20%). Wide dispersion: $6.10 to $25.00 reflects deep uncertainty about R2 execution and path to profitability.

Catalysts Calendar

| Timing | Event | Expected Impact |

|---|---|---|

| Q2 2026 | R2 Performance first deliveries | THE EVENT. Smooth ramp = +20-30%. Delays/quality issues = -25-35%. |

| May 2026 | Q1 2026 earnings | First test of 62K-67K delivery guidance credibility. |

| Oct 2026 | VW JV $1B term loan available | Eliminates near-term capital raise concerns. |

| 2026 | Georgia factory construction begins | 400K capacity target. Funded by $6.6B DOE loan. |

| H2 2026–H1 2027 | Potential capital raise | -15-25% if at depressed prices. |

| Late 2027 | R2 base model ($45K) launch | True mass-market catalyst. 100K+ reservations. |

Market Sentiment

Internet sentiment scores 5.5/10 — neutral-to-slightly-bullish. Reddit activity is low (approximately 1 WSB mention per day). The dedicated r/Rivian subreddit skews bullish with R2 dominating discussion and 85% of owners saying they would buy again. Financial media coverage is 13/18 positive headlines, heavily driven by Motley Fool's bullish framing (“Rivian Is About to Challenge Tesla Where It Hurts Most”).

Insider & Institutional Activity

The insider picture is concerning. CEO Scaringe's last discretionary purchase was May 2022 at $25.78 — he is down 42% on that position. His performance options have a $15.22 strike price, currently underwater. All recent insider activity is systematic selling via 10b5-1 plans. Ford Motor exited entirely in May 2022 at $26–$27/share, saving ~$179M versus holding to today.

The one bright spot: VW maintains its 10%+ ownership stake and has not reduced its position despite Rivian's decline. Institutional ownership is 45.34% (+2.28% net additions), showing institutional accumulation at these lower levels.

Risk Factors

| Risk | Probability | Impact |

|---|---|---|

| R2 ramp fails or significantly delays. New platform, new vehicle — execution risk is high. | 30% | -40 to -60% |

| Tesla accelerates sub-$50K competition. Model Y is already dominant in the segment R2 targets. | 60% | -10 to -20% |

| EV demand weakens under anti-EV policy. Tax credits expired, only 16% of Americans say they'd buy an EV. | 50% | -15 to -25% |

| Cash exhaustion forces dilutive raise. $2.5B annual total cash consumption at current rates. | 25% | -20 to -35% |

| Continued share dilution (SBC + convertibles). ~$1.1B/yr SBC, 40% dilution since IPO. | 80% | -5 to -10% annually |

| VW partnership deteriorates. Concentration risk: 29% of revenue from VW JV. | 15% | -30 to -50% |

Conclusion & Price Targets

Scenario Analysis

| Scenario | Prob. | FY27 Rev | Gross Margin | Target P/S | 12-Mo Target | Return |

|---|---|---|---|---|---|---|

| Bull | 25% | $11B | +14% | 3.5x | $29 | +95% |

| Base | 45% | $8.5B | +8% | 2.5x | $16 | +8% |

| Bear | 30% | $5.8B | +1% | 1.2x | $5 | -66% |

| Probability-Weighted Target | $16 | +8% | ||||

Bull Case ($29)

- R2 ramp succeeds: 10K+/quarter deliveries by Q4 2026

- VW JV software revenue grows to $2B+ with expanding margins

- Total revenue reaches $11B by FY2027 at 14% consolidated gross margin

- DOE loan funds Georgia factory at below-market rates

- Short squeeze: 17.45% short float, 4-5 days to cover

- Re-rates to 3.5x P/S as “platform company”

Bear Case ($5)

- R2 delays or demand disappoints from tariffs/macro headwinds

- $45K base model delayed to late 2027 — miss the mass-market window

- VW reduces JV commitment or renegotiates terms

- Forced capital raise at distressed prices (below $12)

- $1.1B annual SBC + convertible dilution erodes per-share value

- 10% secured notes signal high-yield credit risk perception

Action Plan

| If You... | Action | Rationale |

|---|---|---|

| Have no position | Do not initiate. Wait for price below $12 or two quarters of R2 deliveries above 10K. | +8% probability-weighted upside is insufficient risk compensation. Better entries will likely emerge. |

| Already own shares | Hold through R2 ramp. Hard stop at $10.00 (52W low). | R2 deliveries starting Q2 2026 will provide real data on the thesis. Selling now locks in losses before the catalyst. |

| Want to speculate | Consider selling cash-secured puts at the $10 or $12 strike. | Get paid to wait for a better entry. If assigned, your cost basis is below $12 with the premium collected. |

For more on options income strategies that work well with volatile EV stocks, see the wheel strategy guide or learn how to lower your stock basis using options. For a contrasting analysis of a profitable company, see the STX (Seagate) stock analysis.

Frequently Asked Questions

Is RIVN a good stock to buy?

RIVN is a Hold, not a Buy, at $14.86. The probability-weighted 12-month target of $16 (+8%) is insufficient to justify the risk of a -66% bear case. Rivian has achieved genuine milestones — first gross profit, the VW partnership, and R2 reservations — but automotive margins are still negative without VW software revenue, deliveries declined 18% YoY, and the $45K R2 base model has been delayed to late 2027. Wait for either a better entry price (below $12) or proof that R2 deliveries are ramping successfully (two quarters above 10K units) before buying.

What is the RIVN price target for 2026?

The analyst consensus RIVN price target is $17.83 (+20% upside), with a range of $6.10 (Bernstein) to $25.00 (Baird). My probability-weighted target is $16 based on three scenarios: bull case $29 (25% probability, R2 ramp succeeds), base case $16 (45%, moderate R2 execution), and bear case $5 (30%, R2 delays or demand weakness). The R2 Performance Edition first deliveries in Q2 2026 are the single most important catalyst that will determine which scenario plays out.

Should I buy or sell RIVN?

Neither — hold if you own it, avoid if you don't. The risk/reward at $14.86 is roughly 1:1. If you hold shares, maintain your position through the R2 ramp with a hard stop at $10.00. If you don't own shares, the most attractive strategy is selling cash-secured puts at the $10 or $12 strike to collect premium while waiting for a more favorable entry price. I would upgrade RIVN to a Buy if it drops below $12 or if automotive gross margins turn positive (excluding VW software) for a full quarter.

RIVN stock forecast for 2026 and beyond?

Rivian's near-term forecast depends almost entirely on R2 execution. If R2 deliveries ramp smoothly, 2026 delivery guidance of 62K–67K is achievable, revenue could reach $6.2B, and the stock could re-rate toward $20+. Longer-term, consensus revenue estimates project $8.5B (2027), $11.5B (2028), with first profitability around FY2029 at $0.86 EPS. The Georgia factory (400K annual capacity) and R2 base model ($45K, late 2027) are the major catalysts beyond 2026. In the bull case, Rivian reaches $10B+ revenue by 2028 at expanding margins, implying $24+/share at 3x P/S. In the bear case, R2 disappoints, cash runs low, and the stock revisits its $8–$10 historical floor.

Sources: SEC Filings (10-K, 10-Q, 8-K, DEF 14A), Finviz, Polygon.io, Google News, Reddit, Twitter/X. Report compiled March 16, 2026.