SMMT (Summit) Stock Analysis: Hold at $16 | Binary FDA Bet

Table of Contents

Executive Summary

This Summit Therapeutics stock analysis covers SMMT's fundamentals, clinical pipeline, SEC filings, market sentiment, and insider activity as of March 2026. Here is the bottom line:

- SPECULATIVE HOLD — do not initiate a new position at $16.12. SMMT is a pre-revenue, clinical-stage biotech whose entire $12 billion market cap is a probability-weighted wager on a single FDA decision eight months from now. The risk/reward is roughly neutral at the current price.

- The central question is binary: Will the FDA approve ivonescimab without statistically significant overall survival (OS) data? The pre-specified OS analysis failed at p=0.057. FDA has stated stat-sig OS is necessary for approval in this setting.

- The PFS data is exceptional. A hazard ratio of 0.52 (p<0.00001) represents a 48% reduction in disease progression risk. But PFS does not always translate to OS, and FDA increasingly prioritizes survival endpoints.

- Insider buying is unprecedented in biotech history. CEO Robert Duggan has invested $784M of personal capital. 20 insider trades over 5 years — all purchases, zero sales by anyone, ever. The Akeso CEO is personally buying Summit stock.

- The short squeeze setup is extreme. 33.67% of the float is short with 13.56 days to cover. Only 103M shares are in the float (13.3% of 775M outstanding). FDA approval could trigger a violent squeeze.

| Report | Signal | Key Finding |

|---|---|---|

| Fundamentals | BEARISH | Zero revenue, $12B market cap, $323M annual cash burn, capital raise near-certain |

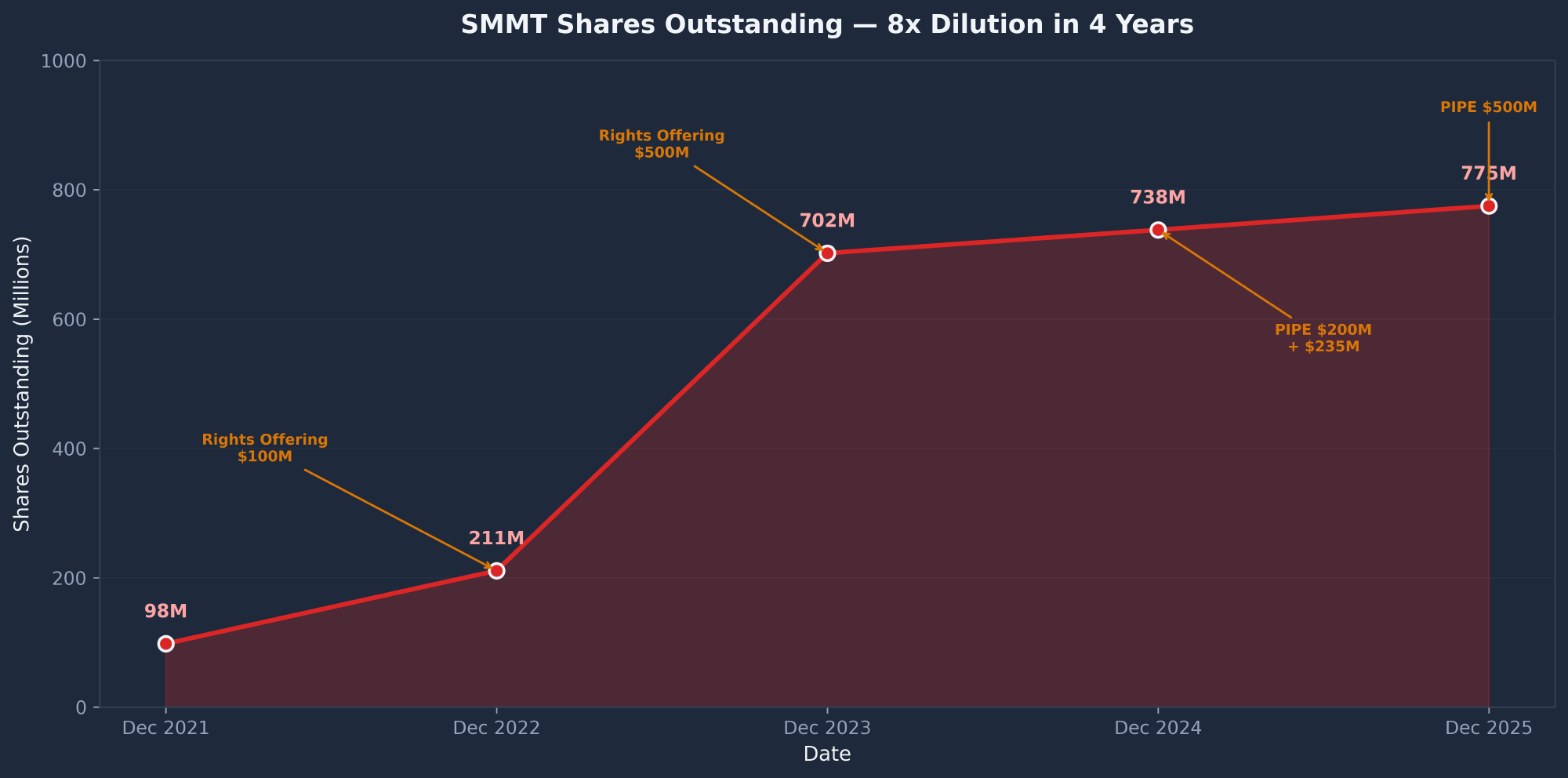

| SEC Filings | CRITICAL | OS missed stat-sig (p=0.057). $732M SBC blowout. 8x dilution in 4 years. $4.56B in Akeso milestones. |

| Technical | NEUTRAL | RSI 52.9, MACD bullish crossover, but 56% below ATH and 20% below SMA 200. Irrelevant for binary biotech. |

| News & Events | SPLIT | BLA accepted (bullish). Regional data concerns flagged by STAT News. Analyst consensus $31.71 (10 Buy / 3 Neutral / 2 Sell). |

| Sentiment | MODERATE BULL | Twitter 70/30 bullish but concentrated in biotech accounts. Reddit: negligible (246-member niche sub). |

| Insider/Institutional | EXTREMELY BULLISH | $630M+ insider buying, zero sales ever. 86.17% insider ownership. Analyst consensus $31.71 (97% upside). |

| COMPOSITE | SPECULATIVE HOLD | The expected value math is roughly neutral. Enormous upside and downside dispersion. Wait for clarity before committing capital. |

Investment Thesis

Summit Therapeutics is not a traditional stock. There are no earnings to model, no revenue to project, no multiples to compare. SMMT is a binary FDA bet. The entire $12 billion market cap is a probability-weighted wager on a single PDUFA regulatory decision eight months from now: will the FDA approve ivonescimab, a first-in-class bispecific antibody targeting both PD-1 and VEGF, for second-line EGFR-mutant non-small cell lung cancer (NSCLC)?

The drug is licensed from China's Akeso Inc. and represents a potential paradigm shift in immuno-oncology. Ivonescimab is the first drug to beat Merck's Keytruda (pembrolizumab) head-to-head in Phase 3 NSCLC on progression-free survival. If approved, it would target the same $25B+ market that Keytruda dominates — with Keytruda's patent cliff beginning in 2028.

I assign a 40% probability of approval (including short squeeze scenarios) and a 45% probability of rejection or delay. The expected value math produces a modestly positive number (+34% probability-weighted), but the dispersion is enormous. Remove the short squeeze scenario and the EV compresses to +9.4% — barely above a risk-free T-bill over the same period. This is why conviction is LOW.

The correct approach: if you have no position, wait for clarity — an AdCom announcement, updated OS data, or a dilutive capital raise that creates a cheaper entry. If you already hold shares, size to max 2–3% of portfolio and be prepared for a total loss scenario. The correct speculative instrument is long-dated call options (Jan 2027 expiry), not stock.

Fundamental Analysis

Company Overview

Summit Therapeutics Inc. (NASDAQ: SMMT) is a clinical-stage biopharmaceutical company headquartered in Miami, FL with approximately 265 employees. The company pivoted entirely from its original antibiotic focus (ridinilazole for C. diff, which failed) to oncology in late 2022 when it licensed ivonescimab from Akeso. Summit holds rights to the US, Canada, Europe, Japan, Latin America, Middle East, and Africa. Akeso retains China and other Asian markets.

The company is controlled by billionaire Robert Duggan, who owns 75.2% of all outstanding shares (555.7M shares) and has invested $784M of personal capital. Duggan previously turned a stake in Pharmacyclics (maker of Imbruvica) into a $3.5B payout when AbbVie acquired it in 2015.

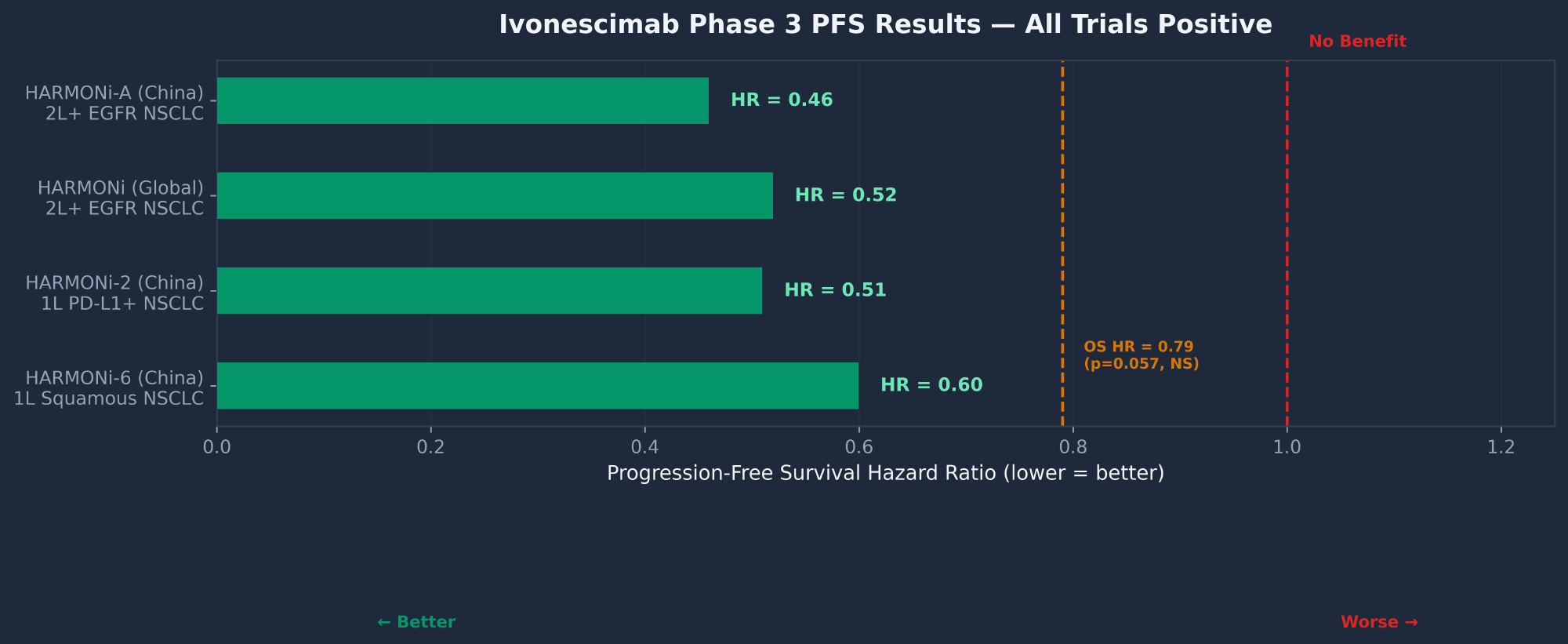

Pipeline — Ivonescimab Clinical Results

| Trial | Setting | PFS HR | OS HR | Status |

|---|---|---|---|---|

| HARMONi-A (China) | 2L+ EGFR NSCLC | 0.46 | 0.74 (stat-sig) | Approved China May 2024 |

| HARMONi (Global) | 2L+ EGFR NSCLC | 0.52 | 0.79 (p=0.057, NS) | BLA filed, PDUFA 11/14/26 |

| HARMONi-2 (China) | 1L PD-L1+ NSCLC mono | 0.51 | 0.777 (interim) | Approved China Apr 2025 |

| HARMONi-6 (China) | 1L Squamous NSCLC | 0.60 | Immature | Positive interim Oct 2025 |

| HARMONi-3 (Global) | 1L NSCLC vs. Keytruda+chemo | Enrolling | N/A | ~1,080 pts planned. Data 2027–2028 |

| HARMONi-7 (Global) | 1L high PD-L1 NSCLC mono | Site activation | N/A | ~780 pts planned |

The pipeline scorecard is 4/4 Phase 3 wins — every trial that has read out met its primary PFS endpoint. The critical issue is that the HARMONi global trial's OS analysis missed statistical significance at p=0.057. An ad hoc analysis with longer follow-up showed a nominal p=0.033, but this was not pre-specified and FDA historically discounts post-hoc analyses. North American patients showed HR=0.70 with median OS not reached vs. 14.0 months — the trend is improving but not conclusive.

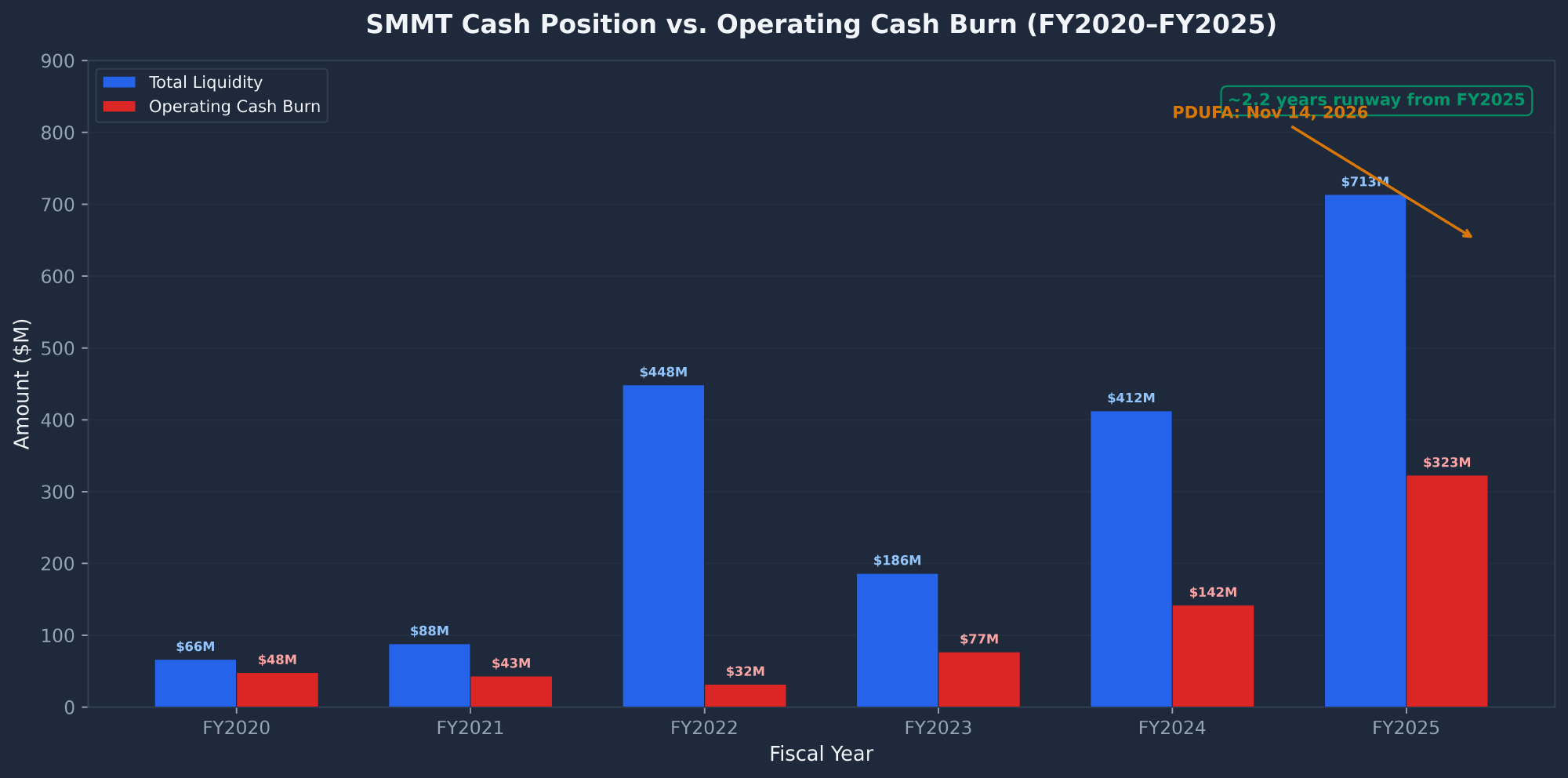

Cash Position & Burn Rate

| Metric ($M) | FY2025 | FY2024 | FY2023 | FY2022 |

|---|---|---|---|---|

| Revenue | $0 | $0 | $0 | $0.7 |

| R&D Expense | $537.7 | $150.8 | $59.5 | $52.0 |

| Net Loss | ($1,079.6) | ($221.3) | ($614.9) | ($78.8) |

| SBC (non-cash) | $732.4 | $51.0 | $14.1 | $11.9 |

| Cash Ops Burn | $322.9 | $142.1 | $76.8 | $31.8 |

| Total Liquidity | $713.4 | $412.3 | $186.2 | $448.4 |

Revenue Projections (Consensus)

| Year | Revenue Est. | EPS Est. | Notes |

|---|---|---|---|

| 2026 | $0 | Loss | PDUFA Nov 14, 2026. No revenue this year. |

| 2027 | $108M | Loss | First revenue if approved. Launch/ramp phase. |

| 2028 | $936M | Loss (narrowing) | Full first commercial year. Keytruda patent cliff begins. |

| 2029 | $2.7B | +$0.86 | Projected first profitable year. |

| 2030 | $4.7B | +$2.26 | Peak sales ramp. At 30x = ~$68/share implied. |

Technical Analysis

SMMT is at a critical inflection point — though for a binary biotech, technicals are secondary to the FDA decision. The stock has declined 56.3% from its $36.91 ATH (April 23, 2025) and is trading near its 52-week low of $13.83. The MACD just triggered a bullish crossover, but the bigger picture remains bearish with price 20% below the declining SMA 200.

| Indicator | Value | Signal |

|---|---|---|

| SMA 10 | $15.64 | BULLISH (+3.1%) |

| SMA 50 | $16.13 | NEUTRAL (at level) |

| SMA 200 | $20.11 | BEARISH (-19.9%) |

| RSI (14) | 52.9 | NEUTRAL |

| MACD | -0.017 / Signal: -0.094 | BULLISH (crossover) |

| Beta | -1.31 | INVERSE CORRELATION |

| ATR (14) | $0.83 (5.1%) | HIGH VOLATILITY |

Key Support & Resistance

| Level | Type | Significance |

|---|---|---|

| $13.83 | Support | 52-week low (Feb 21, 2026). Break below opens $11–$12. |

| $14.43–$14.60 | Support | Jan 2026 cluster low zone. High-volume reversal area. |

| $15.05 | Support | 61.8% Fibonacci retracement from $1.54 low to $36.91 ATH. Currently holding. |

| $17–$18 | Resistance | Heavy overhead supply from Nov 2024–Feb 2026. Unfilled gap at $16.64–$18.10. |

| $20.11 | Resistance | SMA 200 + psychological $20. Every rally since Sep 2025 stalled at $19–$21. |

| $36.91 | Resistance | All-time high. Massive same-day reversal (intraday range: $22.22–$36.91). |

SEC Filings Deep Dive

I analyzed 132 SEC filings spanning 6 annual reports, 15 quarterly reports, 102 current reports, and 8 proxy statements. The filings reveal the full scope of both the opportunity and the risk.

Company Transformation

Summit underwent a radical pivot from a failing antibiotic company to a single-asset oncology bet:

- FY2020–2021: Anti-infectives company focused on ridinilazole for C. diff. Going concern warnings. BARDA contract ($72.5M). 42 employees.

- FY2022 (pivot year): Ridinilazole abandoned (Sep 2022). Akeso license signed (Dec 2022). Discuva platform wound down. $8.5M intangible impairment.

- FY2023: Fully oncology-focused. Akeso deal closed. Going concern: substantial doubt explicitly stated.

- FY2024: Going concern resolved after $479M raised. FDA Fast Track granted. 159 employees.

- FY2025: BLA filed Q4 2025. FDA accepted Jan 29, 2026. PDUFA date: November 14, 2026. 265 employees.

Akeso License — The Economics

| Item | Amount |

|---|---|

| Upfront Payment | $500M ($475M cash + 10M shares) |

| Regulatory Milestones | Up to $1.05B |

| Commercial Milestones | Up to $3.505B |

| Total Potential Obligations | Up to $4.555B |

| Royalties on Net Sales | Low double-digit % |

| Patent Expiration | Core: Aug 2039. Additional: 2042. |

Dilution History

News & Catalysts

Coverage is heavy across financial media (86 articles analyzed), with sentiment split roughly 44% bullish / 35% bearish / 21% neutral. The narrative oscillates between “Keytruda killer” optimism and “OS miss = approval unlikely” skepticism.

Analyst Ratings

| Firm | Rating | Target | Upside |

|---|---|---|---|

| Goldman Sachs | Buy | $42 | +160% |

| Guggenheim | Buy | $40 | +148% |

| Citizens | Outperform | $40 | +148% |

| Citi | Buy | $35 | +117% |

| UBS | Buy | $30 | +86% |

| Barclays | Equal Weight | $18 | +12% |

| Leerink | Underperform | $12 | -26% |

Consensus price target: $31.71 (97% upside). Rating split: 10 Buy / 3 Neutral / 2 Sell.

Catalysts Calendar

| Timing | Event | Expected Impact |

|---|---|---|

| Q2–Q3 2026 | Anticipated capital raise (ATM or secondary) | 5–15% dilution. Short-term negative, but ensures survival through PDUFA. |

| Q2–Q3 2026 | Potential FDA Advisory Committee (AdCom) | ±30% on outcome. If NOT called: mildly bullish. |

| H2 2026 | Updated OS data (if provided during review) | If OS reaches stat-sig: game-changer. Approval probability jumps to 80%+. |

| Throughout 2026 | HARMONi-3 enrollment updates | Progress on the bigger 1L NSCLC trial supports the long-term thesis. |

| November 14, 2026 | PDUFA DATE — FDA decision on ivonescimab BLA | THE EVENT. Approval = $28–$42+. Rejection = $3–$5. CRL with data request = $8–$12. |

Market Sentiment

Internet sentiment is moderately bullish but thin. SMMT has not broken into mainstream retail consciousness. The dedicated r/SMMT subreddit has only 246 members. r/wallstreetbets shows approximately 3 posts total. The only substantive community discussion happened in r/biotech around the PD-1/VEGF dual mechanism of action — a technical thread with 110 comments from people who understand the science, not momentum traders.

Financial media coverage is heavily split: Motley Fool coverage spans both “Is Summit a Millionaire Maker?” and “Is Beaten-Down Summit a Bad-News Buy?” Benzinga provides event-driven coverage. STAT News flagged the regional data concern. The Lancet published HARMONi-6 data, providing clinical credibility.

Insider & Institutional Activity

This is the most one-sided insider buying profile I have ever seen in biotech. Twenty insider trades over 5 years. All 20 are purchases. Zero sales. By anyone. Ever.

Key Insider Purchases

| Insider | Role | Total Invested | Latest Purchase | Sales |

|---|---|---|---|---|

| Robert Duggan | CEO/Chairman | $784M | Oct 2025: 26.7K shares at $18.74 | ZERO |

| Mahkam Zanganeh | Co-CEO | $30M+ | Sep 2025: 338K shares at $17.69 | ZERO |

| Xia Yu | Director (Akeso CEO) | $10M+ | Oct 2025: 533K shares at $18.74 | ZERO |

| Manmeet Soni | COO | $5M | Oct 2023 at $1.68 | ZERO |

| Ankur Dhingra | CFO | ~$700K | Multiple purchases | ZERO |

The Akeso connection is particularly telling — the CEO of the company that licensed ivonescimab to Summit is personally buying Summit stock on the open market. Duggan's most recent purchases (Sep 2024 at $22.70 and Oct 2025 at $18.74) are both above the current price of $16.12, meaning he is underwater and still not selling.

Short Squeeze Setup

| Metric | Value | Significance |

|---|---|---|

| Short Float | 33.67% | One-third of all tradeable shares sold short. |

| Days to Cover | 13.56 | Nearly 3 weeks of average volume to cover. Extremely elevated. |

| Float | 102.98M | Only 13.3% of 775M shares. Insiders hold 86.17% and don't sell. |

| Institutional Ownership | 15.86% | Low but growing (+11.90% institutional transactions). Constrained by insider dominance. |

The squeeze math: ~34.7M shares short on a 103M float with 13.56 days to cover. Insiders own 86.17% and have never sold. Any positive catalyst — particularly FDA approval — could trigger a violent squeeze. The shorts are sophisticated institutional money betting against approval. This is a high-conviction standoff.

Risk Factors

| Risk | Probability | Impact |

|---|---|---|

| FDA rejects BLA (CRL) citing insufficient OS data | 35% | -75% |

| Dilutive capital raise before PDUFA. $299M ATM capacity remaining + $450M shelf. | 70%+ | 5–15% dilution |

| FDA requests more data (partial CRL). Delays 12–18 months. Additional dilution required. | 10% | -38% |

| AdCom called. Creates extreme volatility event before PDUFA. | 40% | ±30% |

| Securities fraud litigation. Pomerantz and Portnoy investigations active. | 30% | 5–10% drag |

| Competitive threat from BNT327 (BioNTech) or LM-299 (Merck). Same mechanism class. | 25% | 10–20% multiple compression |

| Akeso sole-source manufacturing dependency. Supply disruption would be catastrophic. | Low | Severe |

| Duggan concentration risk. 75.2% ownership by one individual. No institutional counterweight. | Ongoing | Governance concern |

Conclusion & Price Targets

Probability-Weighted Scenario Analysis

| Scenario | Probability | Target | Return | Rationale |

|---|---|---|---|---|

| FDA Approval | 40% | $32 | +98% | PFS data exceptional. Unmet need real. But OS missed stat-sig. |

| Approval + Short Squeeze | 15% | $42 | +160% | 33.67% short float, 13.56 days to cover. Goldman $42 target. |

| FDA Rejection (CRL) | 35% | $4 | -75% | Collapses to near cash value. Cash/share ~$0.92 but Akeso license retains some value. |

| FDA Requests More Data | 10% | $10 | -38% | Not dead but delayed 12–18 months. Dilution required. |

| Expected Value (Probability-Weighted) | $21.53 | +34% | Remove squeeze scenario and EV drops to +9.4% — near-neutral. | |

Bull Case ($28–$42)

- PFS HR=0.52 is exceptional. FDA may apply regulatory flexibility given unmet need.

- $784M CEO conviction + zero insider sales = unprecedented skin in the game.

- Short squeeze potential: 33.67% of float short, 13.56 days to cover.

- HARMONi-3 targets the $25B+ 1L NSCLC market. Even a rejection of 2L+ BLA doesn't kill the story.

- Merck M&A optionality: Keytruda patent cliff 2028 creates acquirer urgency.

Bear Case ($3–$5)

- OS missed stat-sig (p=0.057). FDA explicitly stated stat-sig OS is necessary.

- $12B market cap on zero revenue. Pre-revenue biotech with $323M annual burn.

- 8x dilution in 4 years. Further dilution near-certain before PDUFA.

- $732M SBC blowout enriched insiders regardless of FDA outcome.

- China data extrapolation risk: weaker efficacy in non-Chinese patients flagged by STAT News.

Action Plan

| If You... | Action | Rationale |

|---|---|---|

| Have no position | Do not initiate. Wait for AdCom or updated OS data. | Risk/reward roughly neutral at $16.12. Better entries may emerge on a capital raise dip or $14 support retest. |

| Already own shares | Hold. Max 2–3% of portfolio. Hard stop at $13.50. | You've accepted the binary risk. Selling now locks in a loss and potentially misses 100%+ move. |

| Want to speculate | Use Jan 2027 call options ($15 or $20 strike). | Options define max loss upfront. The correct instrument for a binary bet with a specific expiration. |

If you're interested in options strategies for managing binary biotech risk, check out the wheel strategy guide for a more conservative income approach, or learn about cash-secured puts as a way to get paid to wait for a better entry price on speculative names like SMMT. For a contrasting analysis of a profitable, revenue-generating company, see the STX (Seagate) stock analysis.

Frequently Asked Questions

Is SMMT a good stock to buy?

SMMT is not a traditional stock — it is a binary option on FDA approval with a specific expiration date (November 14, 2026). The entire $12 billion market cap is a probability-weighted wager on whether the FDA will approve ivonescimab without statistically significant overall survival data. I rate it a Speculative Hold with low conviction. If you have no position, wait for clarity from an AdCom announcement or updated OS data before committing capital. If you want to speculate, long-dated call options (Jan 2027 expiry) are the appropriate instrument, not stock.

What is the SMMT price target for 2026?

The price target for SMMT is entirely dependent on the FDA decision. The analyst consensus target is $31.71 (97% upside), with Goldman Sachs at $42 (highest) and Leerink at $12 (lowest). My probability-weighted expected value is $21.53 (+34%), but the dispersion is enormous: approval scenarios point to $28–$42, rejection scenarios point to $3–$5, and a partial CRL would land around $8–$12. The PDUFA date is November 14, 2026.

Should I buy or sell SMMT?

Neither. The risk/reward at $16.12 is roughly neutral when you strip out the most optimistic short squeeze tail. If you already own shares, hold with a maximum 2–3% portfolio allocation and a hard stop at $13.50. If you don't own shares, wait for a better setup — either a dilutive capital raise creating a cheaper entry, an AdCom announcement clarifying FDA's thinking, or updated OS data that shifts the approval probability. The correct speculative vehicle is options, not stock.

SMMT stock forecast for 2026 and beyond?

The near-term forecast is binary: approval at the November 14 PDUFA would likely send SMMT to $28–$42, while rejection would crater it to $3–$5. Beyond the PDUFA, if approved, consensus revenue estimates project $108M (2027), $936M (2028), $2.7B (2029), and $4.7B (2030). First profitability is projected for 2029 at $0.86 EPS. The longer-term bull case rests on HARMONi-3 (1L NSCLC vs. Keytruda) data expected in 2027–2028, which targets an even larger market. Even if the 2L+ BLA is rejected, the HARMONi-3 and HARMONi-7 trials keep the broader ivonescimab story alive.

Sources: SEC Filings, Finviz, Polygon.io, Google News, Reddit, Twitter/X. Report compiled March 16, 2026.