TOST (Toast) Stock Analysis: Buy at $28 | $38 Target

Table of Contents

Executive Summary

This TOST stock analysis covers Toast, Inc.'s fundamentals, technicals, SEC filings, market sentiment, and insider activity as of March 2026. I publish stock research reports like this one on this website to share my personal investment analysis. Here is the bottom line:

- BUY at $27.60 with a 12-month target of $36–$40 (+30% to +45% upside). Toast is a generational compounder at a cyclical low — the dominant restaurant operating system trading at a PEG of 0.66 with a pristine balance sheet, $2B cash, zero debt, and a $928M tax shield.

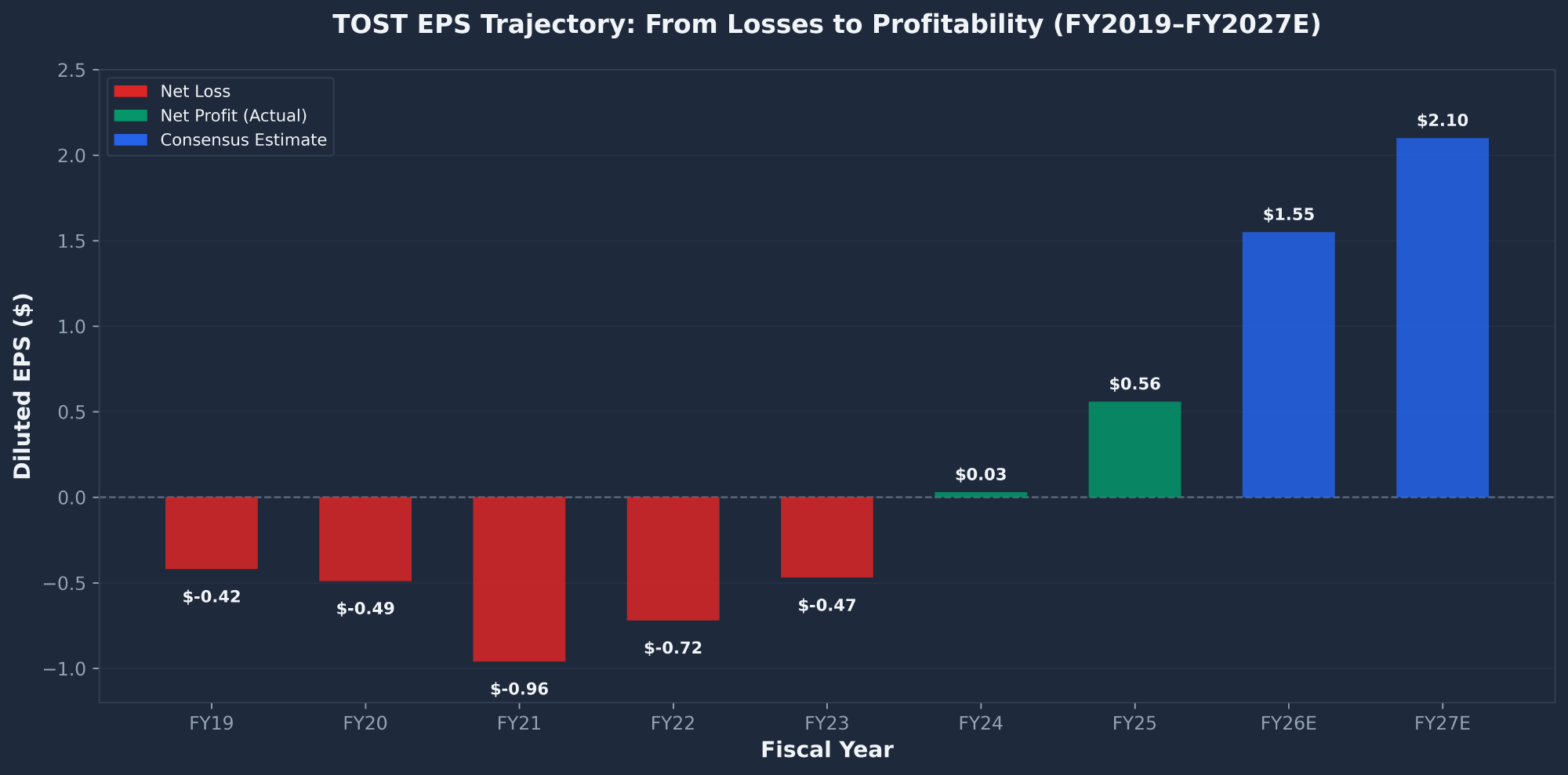

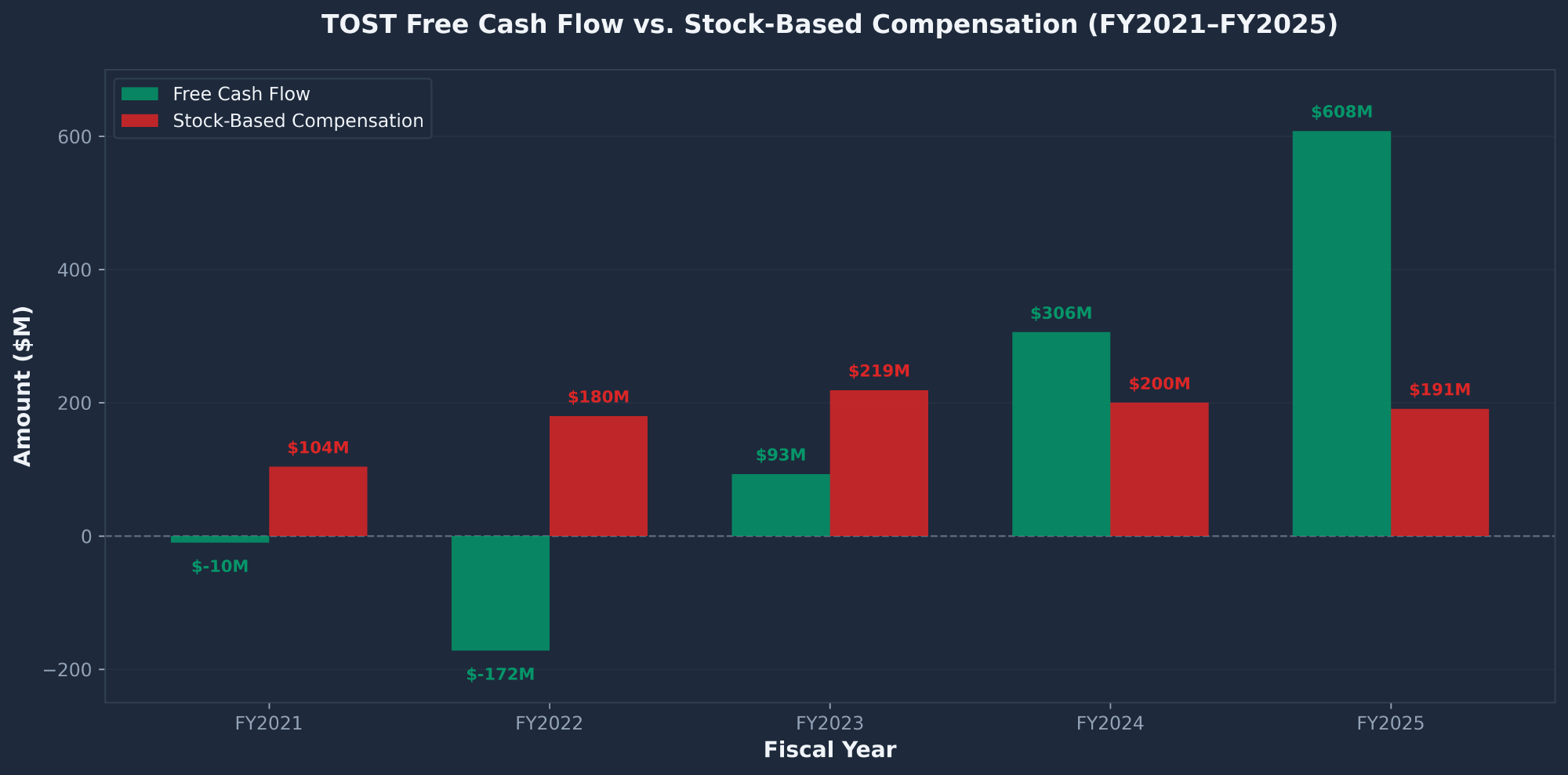

- The profitability inflection is real and accelerating. After $1.2B in cumulative losses from IPO through FY2023, Toast generated $342M in net income and $608M in free cash flow in FY2025. EPS is projected to nearly triple from $0.56 (FY25) to $1.55 (FY26E).

- Massive underpenetrated TAM. With 164K locations out of 860K+ US restaurants, Toast has only ~20% market penetration. The vast majority of restaurants remain on legacy systems. International expansion into the UK, Ireland, and Canada adds further runway.

- Smart money is loading up aggressively. ValueAct Capital doubled its position, Cathie Wood/ARK added to Next Generation Internet ETF, Jennison Associates increased +74%, Marshall Wace +108%, and Norges Bank (Norway's sovereign wealth fund) initiated a new position.

- Technicals demand patience. TOST is in a confirmed bearish trend — below all moving averages with RSI at 43. The relief rally from $24.35 to $30.51 failed at the 50 SMA. Scale in, don't go all-in.

| Report | Signal | Key Finding | Weight |

|---|---|---|---|

| Fundamentals | STRONG BUY | PEG 0.66, Fwd P/E 17.85x, $2B cash, zero debt, $608M FCF, 24% revenue growth | 25% |

| SEC Filings | BULLISH | Revenue 9.3x since FY2019. SBC declining (3.9% of revenue). $928M NOL shield. NRR disclosure dropped — watch. | 20% |

| Technical | BEARISH | Below all MAs, RSI 43, descending channel. MACD crossover improving but unconfirmed. No bottom confirmed. | 15% |

| News & Events | BULLISH | Uber partnership, Applebee's enterprise win, Cathie Wood buying. Consensus target $40.46 (46% upside). | 15% |

| Insider/Institutional | NEUTRAL | 200 trades, zero purchases in 5 years. But systematic 10b5-1 plans. CEO/President retain Class B (10x) control. Institutions aggressively adding. | 15% |

| Sentiment | CAUTIOUSLY BULLISH | Media overwhelmingly positive. Low Reddit activity (not a meme stock). "Too integrated to disrupt" narrative dominant. | 10% |

| COMPOSITE | MODERATELY BULLISH | 4 bullish, 1 bearish, 1 neutral across 6 reports. Weighted composite favors the long side with elevated risk from technicals. | 100% |

Investment Thesis

Toast is a cloud-based, all-in-one digital technology platform built for the restaurant industry. The company provides an integrated suite of SaaS products, financial technology solutions, and hardware that enables restaurants to manage operations, process payments, drive guest engagement, and access capital. Founded in 2012 and headquartered in Boston, Toast went public in September 2021 at $40/share.

The investment thesis is straightforward: Toast is the dominant modern restaurant operating system with only ~20% US market penetration, trading at a PEG of 0.66 after a 44% drawdown from highs. The fundamentals have never been stronger — FY2025 delivered $6.15B in revenue (+24% YoY), $342M in net income (from cumulative losses of $1.2B just two years prior), and $608M in free cash flow. The balance sheet is pristine: $2B cash, zero debt, and a $928M NOL tax shield that means Toast pays essentially zero taxes for the next 3–4 years.

The 44% drawdown from the $49.66 ATH creates the entry opportunity. The sell-off was driven by a broader SaaS sector panic (triggered by the Anthropic Claude Cowork launch), a Q4 EPS miss ($0.16 vs $0.24 expected), and macro tariff fears — not a deterioration in Toast's business. Revenue still beat expectations, locations grew 22%, and management guided $775–$795M adjusted EBITDA for 2026. The risk/reward setup favors a recovery toward $36–$40 over the next 12 months as the market re-prices the profitability trajectory.

Fundamental Analysis

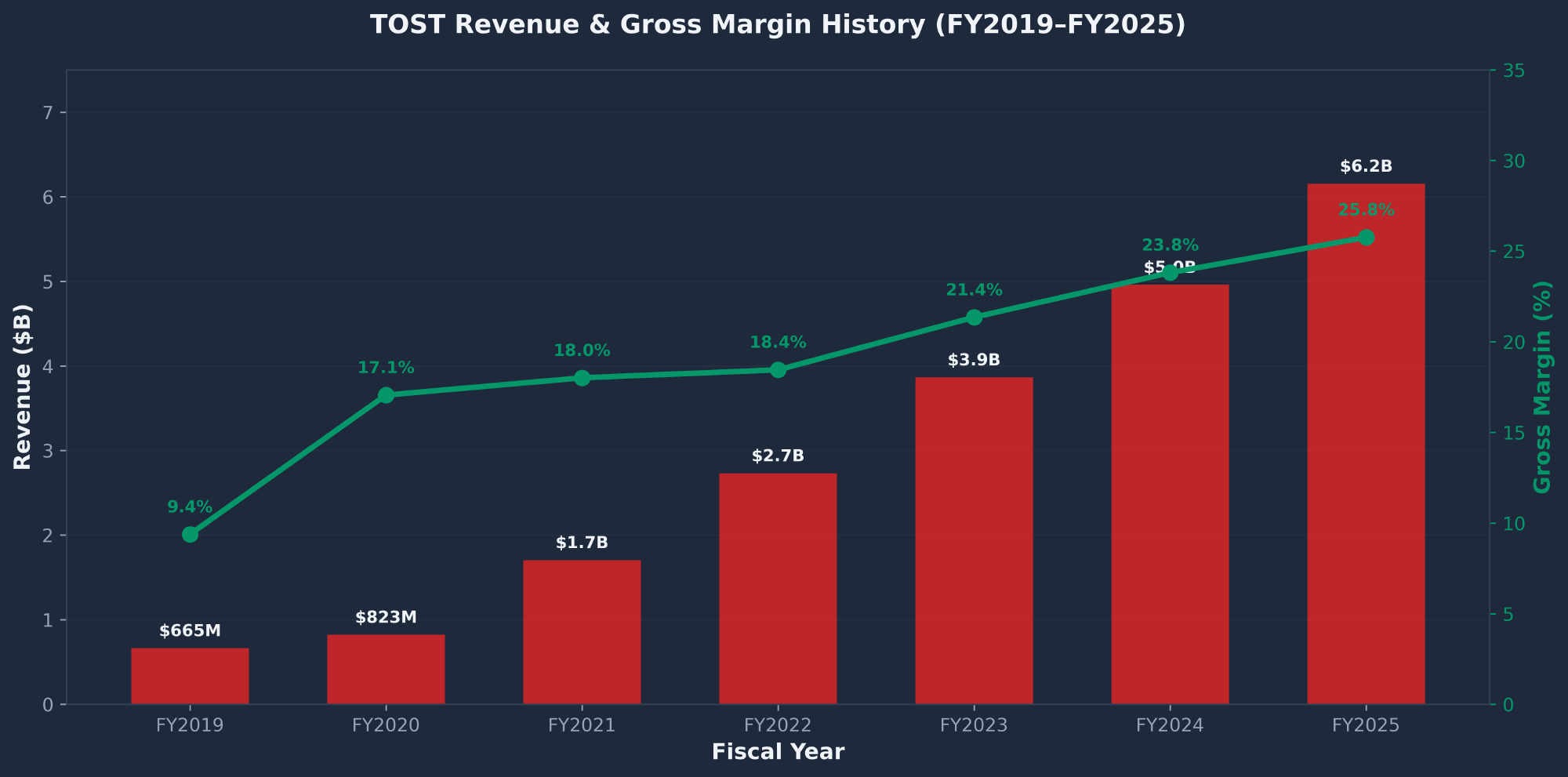

Toast's TOST stock analysis starts with the financials, and the story is one of dramatic transformation. Revenue has grown 9.3x from $665M (FY2019) to $6.15B (FY2025) — a 49.5% five-year CAGR. More importantly, the company crossed the profitability Rubicon in FY2024 and accelerated into FY2025 with a $588M swing in net income over two years (from -$246M to +$342M).

Income Statement Overview

| Metric | FY2022 | FY2023 | FY2024 | FY2025 | FY2026E |

|---|---|---|---|---|---|

| Revenue | $2.73B | $3.87B | $4.96B | $6.15B | ~$7.40B |

| Gross Margin | 18.5% | 21.4% | 23.8% | 25.8% | ~28% |

| Net Income | ($275M) | ($246M) | $19M | $342M | ~$900M |

| GAAP EPS | ($0.72) | ($0.47) | $0.03 | $0.56 | ~$1.55 |

| Adj. EBITDA | ($115M) | $61M | $373M | $633M | $775–$795M |

| FCF | ($172M) | $93M | $306M | $608M | ~$750M |

| Locations | ~79K | ~106K | ~134K | ~164K | ~195K |

| ARR | $901M | $1.22B | $1.63B | $2.05B | $2.3B (Guided) |

Valuation Comparison

| Company | Price | Rev Growth | Fwd P/E | EV/Rev | Edge |

|---|---|---|---|---|---|

| Toast (TOST) | $27.60 | +24% | 17.8x | 2.3x | Fastest grower, lowest Fwd P/E, best balance sheet |

| Block (XYZ) | $59.79 | +12% | ~14x | 1.8x | Broader POS/fintech but lower growth, not restaurant-specific |

| Lightspeed (LSPD) | $8.86 | +20% | ~35x | 1.5x | Higher P/E for lower growth, less focused |

| PAR Technology (PAR) | $14.77 | +15% | N/A (loss) | 2.8x | Enterprise restaurant tech, still unprofitable, much smaller |

Balance Sheet & Cash Flow

The balance sheet is the strongest in Toast's peer group: $2.0B in cash, zero debt, and a $928M federal NOL carryforward ($843M with indefinite life). The $750M buyback authorization signals management confidence. CapEx is just $53M (0.86% of revenue), highlighting the asset-light software model. FCF nearly doubled YoY from $306M to $608M, and SBC has declined from $219M to $191M — the dilution headwind is shrinking in both relative and absolute terms.

Technical Analysis

TOST is in a confirmed bearish trend across all timeframes. The stock has declined 44% from its $49.66 ATH (July 2025) to $27.60, sitting below every major moving average with a fully bearish MA stack.

| Indicator | Value | Signal |

|---|---|---|

| SMA 10 | $28.92 (-4.6%) | BEARISH |

| SMA 50 | $30.62 (-9.9%) | BEARISH |

| SMA 200 | $37.83 (-27.0%) | BEARISH |

| RSI (14) | 42.93 | NEUTRAL-BEARISH |

| MACD | -0.41 (above signal) | IMPROVING |

| Beta | 1.92 | HIGH RISK |

Key Support & Resistance Levels

| Level | Price | Significance |

|---|---|---|

| Support — 52W Low | $24.35 | Hit Feb 24, sharp bounce. Confluence with 61.8% Fib of the full 2022–2025 rally ($25.77). Critical floor. |

| Support — Swing Low | $27.00–$27.60 | Current price zone. Bounced from this area 3x in 6 weeks. |

| Resistance — 10 SMA | $28.92 | Immediate overhead. Price rejected from this area on Mar 9–11. |

| Resistance — 50 SMA / Fib | $30.30–$30.62 | Confluence of 50 SMA and 23.6% Fib. Mar 5–6 rally stalled here exactly. Must clear to confirm reversal. |

| Resistance — 38.2% Fib | $34.00–$34.90 | Major confluence zone. Prior support that broke down. |

| Resistance — 200 SMA | $37.83 | 27% above current price. Reclaim unlikely near-term without major catalyst. |

The most constructive element is the MACD bullish crossover (Mar 3) with positive histogram. However, the histogram is contracting from +0.66 to +0.19, and the MACD line remains below zero. The relief rally from $24.35 to $30.51 (+25%) failed precisely at the 50 SMA / 23.6% Fibonacci confluence — a technically significant rejection that confirms $30–$31 as strong resistance.

SEC Filings Deep Dive

I analyzed 60 SEC filings spanning Toast's IPO (September 2021) through FY2025 (filed February 2026): 5 10-Ks, 13 10-Qs, 35 8-Ks, 4 DEF 14As, 1 S-1, and 2 S-1/As.

Management Credibility Scorecard

Toast has systematically delivered or exceeded every major promise from its S-1. This earns a management credibility rating of A.

| S-1 Promise (2021) | Actual Delivery | Verdict |

|---|---|---|

| ~48K locations (6% of TAM) | ~164K locations by FY2025 (~20% market share) | Exceeded |

| ARR ~$494M | ARR $2,047M (4x IPO level) | Exceeded |

| GPV $38B annualized | GPV $195.1B in FY2025 (5.1x) | Exceeded |

| Path to profitability (ongoing losses expected) | GAAP profitable FY2024 ($19M NI); FY2025 $342M NI | Delivered |

| Expand beyond core US SMB | Entered UK, Ireland, Canada; enterprise wins (Applebee's, Topgolf) | On Track |

Revenue Mix Evolution

Toast generates revenue from three streams: Subscription services (SaaS) at 15% of revenue, Financial technology solutions (payments/fintech) at 82%, and Hardware & professional services at 3%. Fintech dominates on a dollar basis but subscription is the high-margin growth engine, growing 33% YoY in FY2025 vs. fintech at 24%.

Hidden Gems & Red Flags

Other notable findings: the $928M federal NOL carryforward ($843M with indefinite life) means Toast pays essentially zero cash taxes for years — FY2025 income tax expense was only $4M on $346M pre-tax income. The hardware segment remains underwater (-$220M gross profit in FY2025), intentionally subsidizing account acquisition. Total OpEx as a percentage of revenue dropped from 44% in FY2020 to 21% in FY2025 — remarkable operating leverage.

News & Catalysts

Toast's news flow is overwhelmingly bullish. Across 70+ articles analyzed (50 from Massive CLI, 20 from Google News), the sentiment breakdown is approximately 49 positive, 13 neutral, 4 mixed, and 4 negative. Analyst consensus stands at 17 Buy / 7 Hold with a $40.46 consensus target (46% upside).

Key Headlines

| Date | Headline | Signal |

|---|---|---|

| Feb 19 | Q4 2025 Earnings: EPS miss ($0.16 vs $0.24 est.) but revenue beat ($1.63B, +22%). 8,000 net new locations in Q4. ARR guided $2.3B for 2026. | Mixed |

| Feb 25 | ValueAct Capital Doubled Stake — Activist hedge fund doubled TOST position despite SaaS sell-off. Cites 6x EV/ARR, 700K+ legacy locations. | Bullish |

| Mar 8 | Toast + Uber Global Partnership — Preferred delivery integration via Uber Direct. 2026 ad tools planned. Expands GPV and fintech revenue. | Bullish |

| Feb 22 | Cathie Wood/ARK Bought — Added TOST to Ark Next Generation Internet ETF alongside AMZN and SHOP. | Bullish |

| Ongoing | AI Product Suite Launch — Toast IQ & Sous Chef AI tools for restaurant optimization. SoundHound voice AI integration. "Deeply entrenched ecosystem." | Bullish |

Analyst Ratings

| Firm | Rating | Target | Upside |

|---|---|---|---|

| Citigroup | Buy | $51 | +84.8% |

| Wells Fargo | Overweight | $47 | +70.3% |

| JP Morgan | Overweight | $43 | +55.8% |

| BNP Paribas | Outperform | $40 | +44.9% |

| DA Davidson | Neutral | $36 | +30.4% |

Upcoming Catalysts

| Catalyst | Timing | Impact |

|---|---|---|

| Q1 2026 Earnings | May 2026 | Critical. Must beat on EPS to restore profitability narrative after Q4 miss. An EPS beat could trigger a 15–20% re-rating. |

| Uber Partnership Revenue | H1 2026 | Ad tools and delivery integration revenue should begin materializing. Could drive upside to GPV. |

| AI Monetization (Toast IQ) | Throughout 2026 | AI-powered tools create premium subscription tier opportunities. Could accelerate ARPU expansion. |

| Buyback Execution | Ongoing | $750M authorization at current prices could retire ~27M shares (4.6% of float). Provides price floor and EPS accretion. |

Market Sentiment

The overall sentiment for TOST stock is cautiously bullish. Media coverage is overwhelmingly positive: nearly every analyst and financial publication frames TOST as a buy-the-dip opportunity after its ~45% drawdown from highs. The strongest institutional signal is ValueAct Capital doubling its position. The core tension: 26% ARR growth and massive TAM vs. a ~50x trailing P/E and a Q4 EPS miss that rattled confidence.

Community Sentiment

| Platform | Activity | Tone |

|---|---|---|

| r/ValueInvesting | LOW | Watchlist candidate. ValueAct doubling is the most-discussed signal. Skepticism on PE but interest in TAM story. |

| r/stocks | LOW | Appears in megathreads and "growth stocks to buy" roundups. No standalone DD posts. Consensus: solid company, waiting for better entry. |

| r/wallstreetbets | MINIMAL | Not a meme stock. Almost zero standalone TOST posts. This is actually a positive — institutional investors drive the price, not retail hype. |

Bull vs. Bear Community Arguments

Bull Case

- Massive TAM — only ~20% penetrated (164K of 860K+ US restaurants)

- Record net additions: 30K locations in FY2025

- ARR $2B+ growing 26%, subscription margins at 65%

- PEG of 0.66 — cheapest it's been since $14 in 2023

- AI moat deepening (Toast IQ, Sous Chef, SoundHound)

- ValueAct, Cathie Wood, Norges Bank all buying

- Enterprise wins validate upmarket push (Applebee's, Topgolf)

Bear Case

- Trailing P/E ~50x vs. industry 17.5x

- Q4 2025 EPS miss (-33%): $0.16 vs $0.24 expected

- Down 44% from peak with 1.92 beta (amplified drawdowns)

- Restaurant macro/recession risk (first to suffer)

- SBC still inflating earnings vs. true cash profitability

- Competition from Fiserv/Clover, Square, Shopify POS

- NRR disclosure dropped (possible compression)

Insider & Institutional Activity

TOST's insider trading profile is a study in nuance. On the surface, 200 trades with zero purchases over 5 years looks deeply bearish. But the dual-class share structure changes the calculus entirely.

Dual-Class Share Structure

Toast has a dual-class share structure where Class B shares carry 10x voting power compared to Class A shares. Insiders sell Class A shares while retaining their Class B supermajority:

| Insider | Title | Class A | Class B (10x Votes) | Total Sold |

|---|---|---|---|---|

| Narang Aman | CEO | 340K | 18.9M | $27.8M |

| Fredette Stephen | President | 2.9M | 25.7M | $37.3M |

| Yuan David | Director | Liquidated ALL 3 Tidemark fund positions | $27.6M | |

Institutional Flows

On the institutional side, the signal is strongly bullish:

| Institution | Ownership | Change | Signal |

|---|---|---|---|

| Capital International | 7.72% | — | Largest holder — steady |

| Vanguard Group | 7.60% | — | Index/passive — steady |

| Jennison Associates | — | +74.4% | Strong conviction buy |

| Marshall Wace | — | +108.3% | Doubled position — very aggressive |

| Norges Bank | — | New Position | Norway sovereign wealth fund — long-term signal |

| ValueAct Capital | — | Doubled | Activist fund, deep fundamental research |

Risk Factors

| Risk | Probability | Impact | Detail |

|---|---|---|---|

| Technicals Are Awful | High | High | Below all MAs. RSI never reached oversold during 44% decline — suggests distribution, not capitulation. Could retest $24.35 or break lower to $22–$23. |

| Restaurant Recession Risk | Medium | High | Restaurants are first to suffer in a consumer downturn. January job openings at lowest since 2020. Beta of 1.92 amplifies market declines nearly 2x. |

| Q4 EPS Miss Pattern | Medium | Medium | Q4 GAAP EPS of $0.16 vs $0.24 expected (-33% miss). International expansion driving costs. NRR disclosure dropped. If Q1 2026 also misses, profitability narrative takes a hit. |

| Yuan's Discretionary Exit | Low | Medium | Director David Yuan liquidated $27.6M — NOT under a 10b5-1 plan. Discretionary full exit by a board member with inside knowledge. Could be fund lifecycle or private concerns. |

| Competition | Medium | Medium | Fiserv (Clover), Block (Square), Shopify POS, and Lightspeed competing for restaurant share. Oct 2025 unintentional pricing glitch highlighted pricing discipline concerns. |

| Fintech Margin Ceiling | High | Low | Fintech (82% of revenue) has only 23% gross margin — interchange and network fees eat most of the take rate. Overall margin expansion depends on growing subscription faster than fintech. |

Conclusion & Price Targets

Earnings Model: Three Scenarios

| Scenario | Assumptions | FY26 EPS | Multiple | Target | Return |

|---|---|---|---|---|---|

| Bear | Recession, growth slows to 15%, margins compress. Multiple contracts. | $1.20 | 15x | $18 | -35% |

| Base | Consensus 20% revenue growth, EPS to $1.55. Multiple re-rates to 23–26x as profitability proves out. | $1.55 | 23–26x | $36–$40 | +30% to +45% |

| Bull | Accelerating growth (25%+ rev), EPS beats, international traction, AI monetization. Multiple re-rates to 30x+. | $1.75 | 30x | $52.50 | +90% |

Bull Case ($52.50)

- EPS beats to $1.75+

- International locations ramping faster than expected

- AI products (Toast IQ) creating premium subscription tier

- Multiple re-rates to 30x as profitability narrative solidifies

- Uber partnership drives upside to GPV and fintech revenue

Bear Case ($18)

- Recession drives restaurant closures and delayed tech adoption

- EPS misses continue through FY2026

- Multiple compresses to 15x as growth narrative breaks

- Competition from Fiserv/Square captures incremental share

- NRR compression confirms weakening unit economics

Suggested Entry Plan

| Action | Price | Detail |

|---|---|---|

| Buy 1/3 | $27–$28 | Initial position at current levels. Price has bounced from this zone 3x in 6 weeks. |

| Buy 1/3 | $24.50–$26 | Add on retest of 52W low zone. $24.35 is the line in the sand (61.8% Fib confluence). |

| Buy 1/3 | Above $30.62 | Final add on reclaim of 50-day SMA with volume. Confirms the downtrend is breaking. |

| Stop Loss | Below $23.50 | Exit full position. Break below $24.35 on volume signals structural breakdown to $22–$19 range. |

If you're interested in learning how to use options strategies like cash-secured puts to enter positions at better prices, or how the wheel strategy can generate income on stocks like TOST, check out those guides. You can also explore the best stocks for the wheel strategy or learn about lowering your stock basis using options.

Frequently Asked Questions

Is TOST a good stock to buy?

Based on my TOST stock analysis, I rate Toast as a BUY at $27.60 with a 12-month target of $36–$40. The stock trades at a PEG ratio of 0.66, which is the cheapest it's been since early 2023. With $2B in cash, zero debt, $608M in free cash flow, and 24% revenue growth, the fundamentals have never been stronger. The 44% drawdown from highs was driven by macro fears and a Q4 EPS miss, not a business deterioration. However, the bearish technicals and 1.92 beta demand a scaled entry approach — don't go all-in at once.

What is the TOST price target for 2026?

My base case target for TOST is $36–$40 over the next 12 months, assuming consensus revenue growth of ~20% and EPS expansion to ~$1.55 on a 23–26x forward multiple. The analyst consensus target is $40.46 (17 Buy, 7 Hold). In a bull scenario with accelerating growth and AI monetization, the stock could reach $52.50 (+90%). In a bear scenario with recession-driven deceleration, the downside target is $18 (-35%).

Should I buy or sell TOST?

I recommend buying TOST using a scaled entry approach: buy 1/3 at $27–$28 (current levels), add 1/3 on a retest of $24.50–$26 (near 52W low), and deploy the final 1/3 on a reclaim of the 50-day SMA above $30.62. Set a hard stop below $23.50. The risk/reward at current levels is asymmetric: $18 bear case (-35%) vs. $40 base case (+45%) vs. $52.50 bull case (+90%). If you already own TOST, this is not the time to sell — the fundamentals don't justify the current price decline.

TOST stock forecast for 2026 and beyond?

Toast is positioned for multi-year compounding. Revenue is projected to grow from $6.15B (FY2025) to ~$7.4B (FY2026) and ~$8.7B (FY2027). EPS should scale from $0.56 to ~$1.55 (FY2026E) to ~$2.10 (FY2027E) as operating leverage kicks in. With only ~20% US market penetration, an expanding international footprint, AI-powered products (Toast IQ, Sous Chef), and a fortress balance sheet, Toast has the runway for sustained 20%+ growth for several more years. The key catalyst is Q1 2026 earnings (May 2026) — an EPS beat would likely trigger a meaningful re-rating.

Sources: SEC Filings (10-K, 10-Q, 8-K, DEF 14A, S-1), Finviz, Polygon.io, Google News, Reddit, Motley Fool, Seeking Alpha, Yahoo Finance, Investing.com. Report compiled March 15, 2026.